This Top Stock Looks Too Cheap to Ignore

Key Points

Oscar Health has made major inroads in the health insurance market with its tech-forward plans.

The company was unprofitable last year, but it is well on its way to fixing these issues in 2026.

With its long-term growth trajectory, Oscar Health still looks undervalued right now.

- 10 stocks we like better than Oscar Health ›

The conventional wisdom holds that a stock that trades up more than 50% in less than six months is overvalued. But sometimes the best stocks are recent winners that Wall Street is only beginning to uncover, with fundamental business improvements that remain undervalued relative to their long-term growth trajectories.

This is an apt description for healthcare disruptor Oscar Health (NYSE: OSCR). Oscar Health is a health insurer stealing market share with its technology-focused offering and is beginning to show a profit inflection. Here's why shares -- up 53% so far this year -- are still too cheap to ignore.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Market share gains and rapid growth

When considering basic health insurance, one might argue that it is a commodity. All the insurer is doing is providing blanket coverage across various health providers in the local area, subject to stringent regulations such as Medicare and the Affordable Care Act (ACA) marketplace.

Where Oscar Health has made inroads, from a standing start a decade ago, is through a better customer experience across everything outside traditional health services. It has built a cloud-based software solution from the ground up, complimentary telehealth for all users, and transparent pricing compared to the competition. It may take years for Oscar to catch up to legacy competitors like UnitedHealth in terms of doctor and care coverage across the United States, but it is already light-years ahead in the rest of the customer experience.

This is why Oscar Health's total number of members paying for insurance has grown rapidly in recent years, hitting 3.2 million at the end of Q1 2026. Right now, the company focuses only on the ACA marketplace, making this growth even more impressive. In Q1 2021, Oscar had just over 500,000 paying insurance members.

The path to operating leverage is clear

What kept Oscar Health's stock in the gutter last year was rising healthcare utilization among its members, which exceeded analyst projections. This was an issue for all health insurers in 2025, leading to a decline in profitability. In 2025, Oscar Health had a $400 million operating loss due to these rising costs.

At the same time, the United States government debated last year whether to eliminate extended tax subsidies for ACA marketplace payors, which increased the pool of citizens who could afford individual health insurance, a boost for Oscar Health. As the government let these subsidies expire amid a tough year for Oscar, the stock began to fall.

It turns out that Oscar Health's nimble management had already prepared health insurance plan pricing for subsidy experimentation while also being conservative in projecting healthcare utilization among members to ensure 2025 did not repeat in 2026.

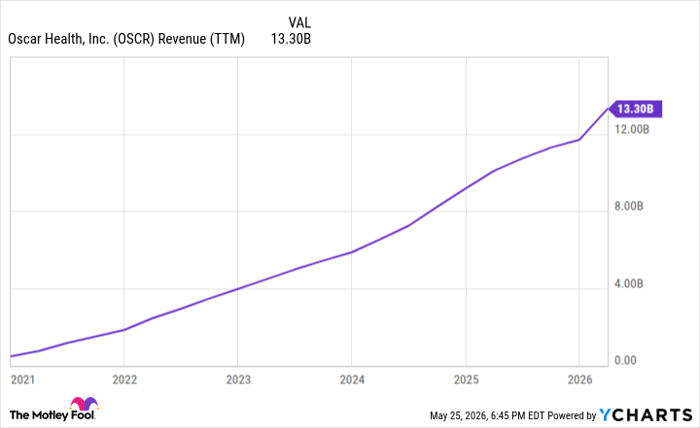

Q1 2026 results proved the strategy's intelligence. Oscar Health generated $700 million in operating income in the first quarter, gaining market share while also achieving operating leverage. It expects typical seasonality in health insurance to lower its 2026 annual operating earnings to $250 million-$450 million, but that would still be a record high for the business. If the company can keep adding new members, it will gain greater nationwide scale, enabling stronger earnings growth in the years ahead.

Data by YCharts.

Why Oscar Health stock is too cheap to ignore

After jumping up 53% this year, Oscar Health trades at a market cap of $6.63 billion. This is still cheap compared to what the business can earn in a few years. At the high end of its 2026 guidance, the company expects revenue of $19 billion and operating income of $450 million, resulting in a profit margin of just 2.3%.

More scale in the years ahead should enable greater expansion of profit margins. Remember that $30 billion in premium revenue and just a 3% profit margin is $900 million in annual operating income, or less than 10x its current market cap. Given the size of the healthcare industry in the United States, premium revenue could grow well beyond $30 billion over the long term.

This makes Oscar Health stock still cheap despite its 50% year-to-date gain.

Should you buy stock in Oscar Health right now?

Before you buy stock in Oscar Health, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Oscar Health wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $472,852!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,317,207!*

Now, it’s worth noting Stock Advisor’s total average return is 984% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 28, 2026.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool recommends UnitedHealth Group. The Motley Fool has a disclosure policy.

Recommended Articles