Marvell’s Data Centre Revenue Grew 42% and Its Custom AI Chips Are Landing at Hyperscalers — Is MRVL a Buy at $195?

TradingKey - Marvell Q1 FY2027: $1.41B revenue +18% YoY, Data Centre +42% to $678M. Custom ASIC wins at hyperscalers. MRVL at $195, Fib cluster below $198 resistance. RSI 65. Target $202.73.

Marvell Technology (NASDAQ: MRVL) released its Q1 fiscal 2027 earnings on May 3, surpassing all major forecasts: $1.41 billion in revenue, representing an 18% year-over-year increase; $678 million in Data Centre revenue, up 42% compared to the previous year; and a non-GAAP gross margin reaching 52.8%. The business landed fresh custom ASIC design wins with large cloud service providers, and its Ethernet switches and optical DSPs continue to gain traction in upcoming generation AI clusters.

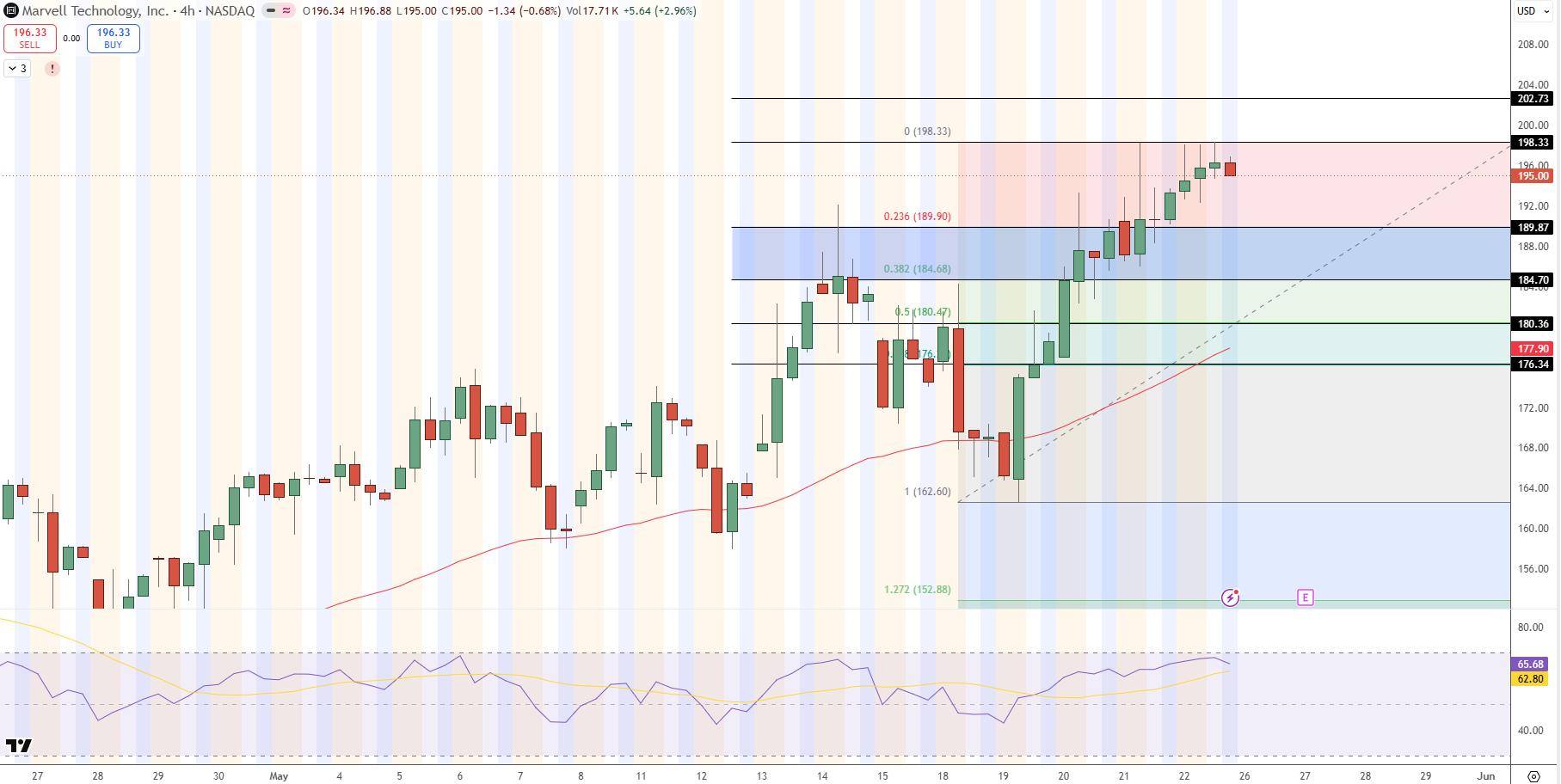

At 195 per share, MRVL is challenging the 0% Fibonacci extension at $198.33 on the 4-hour timeframe chart. The RSI sits at 65.68, while the green candles with volume confirm that buyers are in control. The $196 to $198 resistance level remains the critical barrier to overcome.

Marvell Q1 FY2027 earnings review: Data Centre grows 42% and new custom ASIC wins

The Q1 FY2027 quarter validated what Marvell has touted as its core strategy over the past two years. Data Centre revenue of $678 million surged 42% on an annual basis, and today comprises some 48% of total revenue. This represents the company's fastest-growing category, one that is both highly profitable and has the longest-term contracts.

CEO Matt Murphy emphasized in the earnings report that Marvell's Ethernet switches and optical DSPs are increasingly widely adopted among the large cloud providers that are building 100,000-GPU-plus AI clusters. At such massive scales of GPUs, the networking layer, which is composed of Ethernet switches, optical transceivers, and cabling, is of just as much importance as the GPU themselves. Marvell is part of this very layer.

More importantly, Marvell has announced new custom ASIC design wins in the quarter. A custom ASIC refers to a bespoke silicon chip designed for a specific cloud provider workload (for example an inference accelerator, a custom networking chip, a controller for specialized storage, or other hardware that fits the architecture of a single large cloud services business). These are not commodity chips sold to the open market, but are bespoke designs that guarantee multi-year revenue streams from the customer at structurally-higher margin levels than standard networking ASICs. The new designs announced in Q1 FY2027 will not come online until production ramps over the 12 to 24 months, meaning the $678 million in Data Centre revenue does not represent where the segment will be by Q4 FY2027.

How is Marvell different from Nvidia, Cisco, and Broadcom within the AI infrastructure stack?

When we think about spending on AI infrastructure, it can be segmented into three different categories:

- Compute (Nvidia GPUs, Google TPUs, AMD MI-series, etc.)

- Networking fabric (Ethernet switches, optical transceivers and cabling that connect the compute nodes)

- Custom silicon (bespoke chips that do specific tasks more efficiently than standard compute hardware).

Marvell mainly participates in category two and three. That means its primary competition in category two are companies like Cisco, whereas its chief competition in category three are companies like Broadcom.

A relatively little talked about Marvell opportunity is its optical DSP business. At the gigawatt scale of an entire AI cluster, data center racks and multiple data center buildings are connected by optical cables that run at the speed of light. In short, the internal interconnects between the racks must be fiber optical, and the optical signals between the racks must be high-speed, high-volume DSPs. Marvell sells these PAM4 DSPs and optical interconnect products.

The reason the optical DSP market is so important to Marvell is that it's growing faster than the market for GPUs. For every GPU that is added to a cluster, a disproportionate number of extra DSP chips and fiber cables are needed to make the cluster faster. That means Marvell is benefiting from a tailwind driven by GPU growth that outpaces its own GPU growth.

MRVL technical analysis: Fib cluster at $198 with RSI 65 and the rising trendline

On the 4H chart, MRVL is at $195 per share, having risen from the $157 low in May. Higher lows have been formed since, as the stock has retook 0.236 Fibonacci at $189.90 and 0.382 Fibonacci at $184.68 on bullish engulfing candles on volume-heavy days.

MRVL Price Chart - Source: Tradingview

Sellers are at $196 to $198, a price level in front of the 0% Fibonacci extension at $198.33. The RSI is at 65.68, sitting in healthy bullish terrain without showing overbought territory, and there is a small positive divergence on the most recent low. Should price drop before it breaks out of the zone, the support cluster at $189.87 to $184.70 needs to be held.

MRVL Technical Trade Setup

- Entry: Long above $196.33, 0% Fibonacci cleared

- Target: $202.73, trendline extension level

- Support: $189.87, $184.70, fib cluster support

- Stop loss: Daily close below $189.87, trendline broken

What did Marvell Tech Q1 FY2027 results show?

Marvell reported Q1 FY2027 Revenue at $1.41 B, +18% YoY.

Data Centre: +42% YoY to $678 M (Ethernet switches, optical DSPs, custom ASICs for hyperscaler AI). Non-GAAP Gross Margin: +460 BPS to 52.8%. New custom ASIC design wins with major cloud providers ramping to revenue over 12-24 months. Next earnings Q2 FY2027 in late Aug is the next hard catalyst.

What does Marvell Tech actually make in AI?

Marvell makes 3 categories of AI infrastructure products:

- High-speed Ethernet switches optimized for AI GPU clusters, as scale increases, network fabric bottlenecks performance

- Optical DSPs/PAM4 interconnects transmitting high data rates that copper cannot reach within/between large AI data center facilities

- Custom ASICs designed for specific hyperscaler needs, inference accelerators, specialized networking, storage controllers, creating long-term supply partnerships with higher margin profiles than standardized silicon

Narrowly similar to Marvell in both custom ASICs and high-speed Ethernet switching capability: Broadcom.

Is MRVL stock buyable today at $195 in May 2026?

The technical picture is favorable for buyers. The stock price has climbed along a rising support line starting from May’s $162 lows, forming higher lows and holding a 65.68 RSI. Buying pressure remains strong when volume confirms price advances. Key resistance area: $196-$198. Price breaks above $196.33 to target $202.73. Major support zone: $189.87 to $184.70.

Fundamentals: Data Centre growth at +42% with new custom ASIC design wins growing over the next 12-24 months; growing adoption of optical DSPs. This provides solid forward visibility to support price. Risk: slower AI spending by major cloud vendors; increased competition from Broadcom for custom silicon business.

The bottom line

Data centre growth was up 42%, custom ASIC design wins are picking up, and optical DSP technology is finding its place in the AI networking infrastructure. These elements give Marvell a long-term revenue growth trajectory that puts it apart from both Nvidia and Cisco. Marvell’s announced custom ASIC design wins represent incremental revenue that will be reflected in 12 to 24 months, meaning its current $678 million Data Centre quarterly number falls well short of the expected growth for the division by the end of FY2027.

MRVL has $195 shares currently approaching the $198.33 Fibonacci resistance area with 65 on the relative strength index and no change to an established upward trend. If price clears the $196.33 threshold, target price $202.73. Late August’s Q2 FY2027 earnings report serves as next catalyst. Broadcom’s outlook for hyperscaler custom silicon represents most pertinent proxy for Marvell’s order flow over the near term.

Recommended Articles