SoftBank Rises About 40% in Three Days, How Much Further Can Arm Valuation Rerating and OpenAI IPO Expectations Push Stock Price?

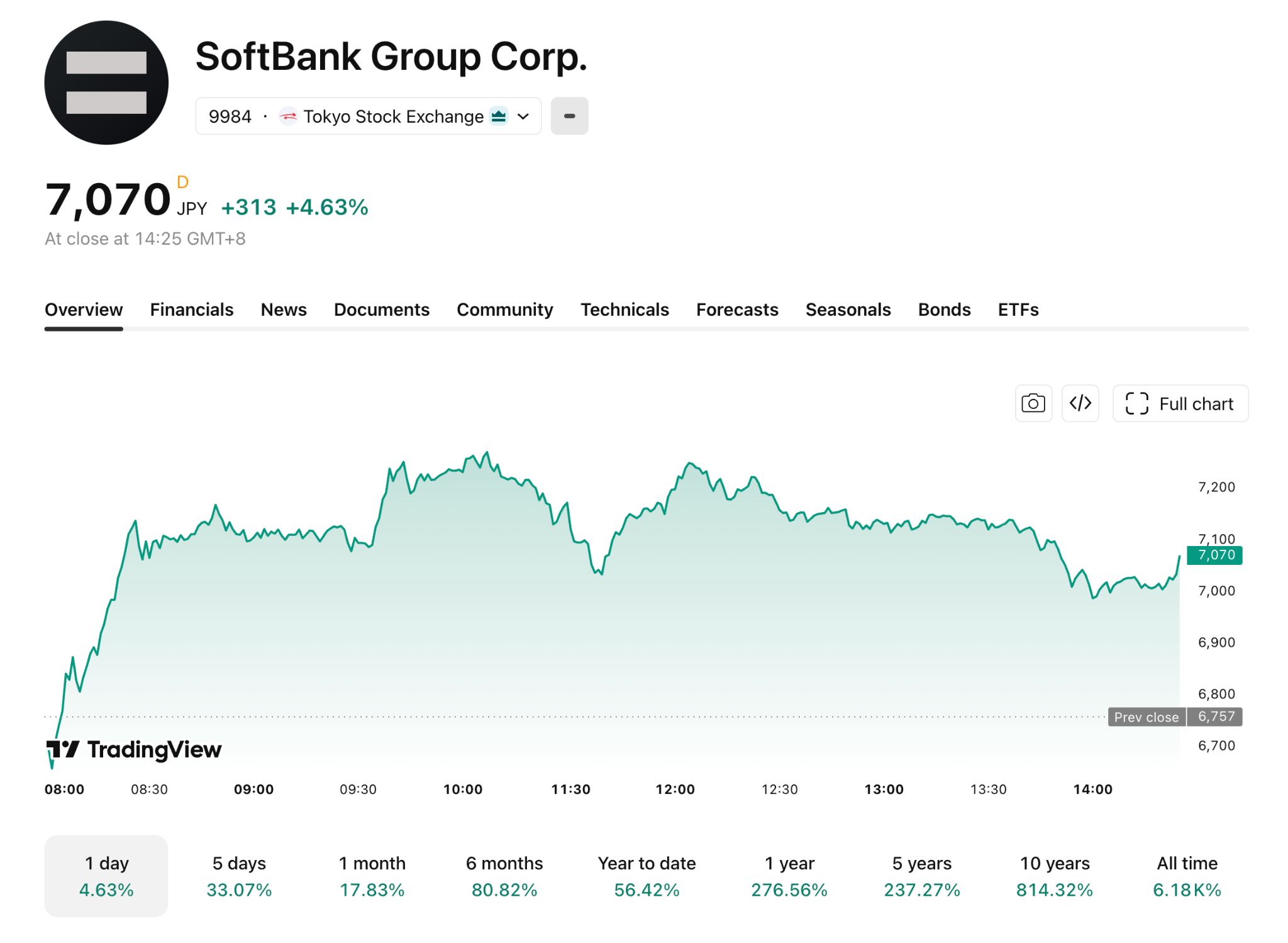

TradingKey - During the Asian trading session on May 25, SoftBank Group closed up 4.63% at 7,070 yen, extending last week's strong momentum. The stock surged 19.84% and 11.9% last Thursday and Friday, respectively, for a cumulative three-day gain of approximately 40%.

This rally is primarily driven by three factors: Nvidia's earnings report ( NVDA) boosting Arm ( ARM) share price, mounting expectations for an OpenAI IPO, and SoftBank's own earnings beating estimates. The market's primary focus now is how much more upside remains for this rally driven by Arm and OpenAI.

[SoftBank stock price trend, Source: TradingView]

ARM and OpenAI, two core assets, account for nearly 70% of the valuation.

According to Morningstar estimates, based on the day's closing price, SoftBank's approximately 90% stake in Arm accounts for about 40% of its total assets, while its roughly 13% stake in OpenAI accounts for approximately 26%, with the two combined representing nearly two-thirds of the total.

Arm's recent rally was bolstered by Nvidia's earnings results. Nvidia reported quarterly revenue of $81.615 billion on May 20, up 85% year-over-year, and stated that revenue from its Arm-based Vera CPUs is expected to reach $20 billion this year. Driven by this, Arm's stock has surged more than 30% since Nvidia released its earnings on May 20.

According to media reports, SoftBank's cumulative investment in OpenAI totals approximately $64.6 billion, with unrealized paper profits of about $45 billion. OpenAI could go public as early as this autumn, with its valuation potentially surpassing $1 trillion.

Furthermore, the full-year net profit for fiscal year 2025, announced on May 13, reached 5 trillion yen, a more than fourfold increase year-over-year, far exceeding market expectations.

SoftBank Valuation Analysis: Room for NAV Discount Narrowing Remains the Core Disagreement

As a holding company, SoftBank Group’s market capitalization has long traded below the sum of its net asset value (NAV), a phenomenon known as the "holding company discount." SoftBank’s average discount rate over the past five years was approximately 50%, reaching 55%–60% at the start of 2025.

As the AI sector heats up and assets like OpenAI mature, the discount has narrowed significantly. Morgan Stanley noted that the discount rate has fallen from over 50% to approximately 35%, recently compressing further to about 17%. UBS estimates SoftBank’s net asset value at approximately 42.5 trillion yen, suggesting that a 20% discount is reasonable under an AI-led narrative.

Compared to other investment holding companies, Berkshire Hathaway typically trades at a 5%–10% discount due to its diversified cash flows and extremely low debt, while Prosus maintains a long-term discount of 40%–50% due to asset concentration and governance issues. SoftBank’s 17% discount lies between the two, reflecting high asset quality alongside risks from debt and concentration.

The current core market debate centers on whether there is room for the discount to continue narrowing. Optimists argue that as key catalysts like the OpenAI IPO materialize, the discount is expected to compress further, thereby supporting an upward trend in the stock price.

Conservative views warn that approximately 16 trillion yen in interest-bearing debt at the SoftBank parent level and over-concentration in AI holdings could cause the discount to widen again. Notably, a $40 billion unsecured bridge loan is set to mature in March 2027.

Whether the discount can narrow further depends on three variables: OpenAI’s IPO valuation and liquidity, debt refinancing conditions, and the sustainability of Arm’s share price. While market expectations for OpenAI are already well-priced, significant uncertainty remains regarding debt refinancing. Even if OpenAI lists successfully, the discount rate is unlikely to break below 15% if refinancing costs rise sharply.

ARM: Valuation Divergence and Concentration Risk

[Source: TradingKey]

Wall Street is significantly divided over Arm's prospects. According to TradingKey data, the average price target from the 40 analysts covering Arm is currently $228.81, implying a 25.35% downside from the current share price.

The bullish representative, Bernstein, has set a price target of $300, calling Arm "at the center of the CPU renaissance"; the bearish representative, Goldman Sachs ( GS ), maintains a "Sell" rating with a price target of $125, believing the valuation excessively reflects optimistic expectations.

The core disagreement lies in whether Arm can secure more CPU design orders beyond Nvidia. Can the decline in smartphone royalties be fully offset by growth in the data center segment? Initial signs of the answer will emerge as early as Arm's next quarterly earnings report.

SoftBank has placed a concentrated bet of over $64.6 billion on OpenAI, on the premise that OpenAI maintains its leadership. While OpenAI currently remains in the top tier, competition is intensifying: Google's Gemini is catching up in the multimodal field, and new entrants like xAI are also investing heavily. If OpenAI's advantage is eroded by competition, its trillion-dollar valuation will face a reassessment.

Concentrated bets on a single company are not a flaw in themselves; Berkshire Hathaway has long employed a similar strategy. SoftBank's specific risk lies in the rigid repayment pressure on its liability side, while OpenAI cannot be easily liquidated before going public. This maturity mismatch is the fundamental reason why the concentration risk is magnified.

Market Outlook: Can OpenAI’s Valuation Break $1 Trillion?

In the short term, Arm and OpenAI may still drive SoftBank higher, but the current share price has already priced in substantial optimism. Against the backdrop of approximately 16 trillion yen in interest-bearing debt, it is difficult for the discount rate to fall to Berkshire's level of 5%–10%. To narrow further to below 15%, conditions such as an OpenAI IPO valuation exceeding $1 trillion, manageable refinancing costs, and Arm royalty growth exceeding 10% quarter-on-quarter must be met.

Investors should monitor four key signals: if OpenAI's valuation guidance is below $800 billion, the discount rate may widen to over 20%; if SoftBank's refinancing spread is below 200 basis points, the discount rate could compress toward 12%–15%; Arm royalty growth below 5% quarter-on-quarter is bearish; and initiating buybacks when the discount rate exceeds 25% would be a bottom signal.

Recommended Articles