Palantir Stock Is Down 35% From Its All-Time High. Should You Buy the Dip?

Key Points

Palantir's revenue growth continues to accelerate.

The company's profit margin has reached impressive levels.

The stock is still pricey.

- 10 stocks we like better than Palantir Technologies ›

For a while, Palantir Technologies (NASDAQ: PLTR) was one of the best-performing artificial intelligence (AI) stocks to own, and its shares regularly set record highs. However, the market's enthusiasm for it has waned in the past half-year or so. Palantir stock peaked in October, and since then, it has fallen by around 35%. That's a significant course correction, and unlike most other AI stocks, it has been trading sideways and slightly downward since April began.

Is Palantir a buy now on the dip? Or is there something else going on?

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Palantir's growth has been nothing short of incredible

Since October, Palantir has delivered a couple of earnings reports. Both were excellent, and Q1's was its strongest ever. In that quarter, revenue grew 85% year over year to $1.63 billion, with strength in both its commercial and government segments.

The U.S. continued to lead the way in terms of demand. Palantir has become synonymous with the generative AI build-out, and its AIP product lineup is to thank for that.

Another positive aspect of Palantir is its profit margin. Unlike many tech companies that operate under a philosophy of growth at all costs, Palantir posted an impressive 53% net income margin during Q1. Few companies ever reach a profit margin this high, so it's all the more impressive that Palantir could notch it when it's in the middle of a major growth cycle. But therein lies a problem.

Because Palantir's profit margin has already been optimized, it's not likely to benefit from the combination of a rising profit margin and top-line growth. Instead, the only way for Palantir to justify its incredibly high valuation is by growing its revenue.

That's exactly why the stock is well off its all-time high.

The reality is that Palantir is crushing it from a business standpoint, but the stock got overhyped and pushed to a valuation that was nearly impossible to live up to. Even after the sell-off, Palantir's stock is still incredibly pricey.

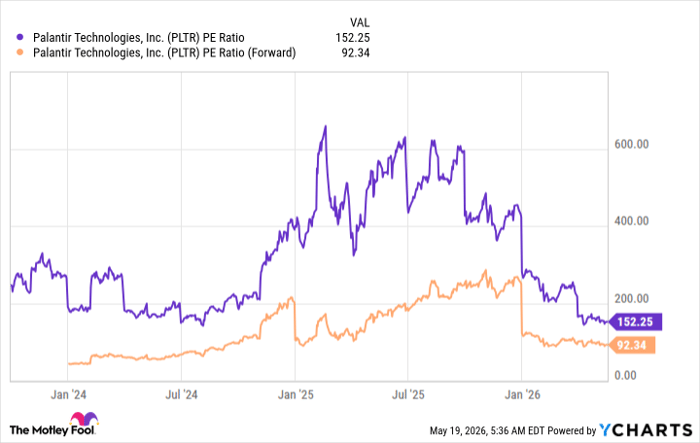

PLTR PE Ratio data by YCharts

At 152 times earnings and 92 times expected forward earnings, Palantir is far more expensive than many of its peers. It will have to double, if not triple, its earnings after 2026 to become a more reasonably valued stock, and that assumes that its share price holds steady for some time.

If you think that it can deliver that type of bottom-line growth, then Palantir could be a solid stock pick for the longer term. If you're like me and skeptical about its ability to achieve that pace, it may be smart to stay patient with this stock and wait for a better deal to come along.

Should you buy stock in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $481,589!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,345,714!*

Now, it’s worth noting Stock Advisor’s total average return is 993% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 22, 2026.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool has a disclosure policy.

Recommended Articles