Nvidia Q3 Earnings Explode: $57B Smashes Wall Street, After-Hours Rally of 6% Slaps Down the "AI Bubble" Narrative!

- Gold Prices Under Pressure After Hitting $4,600, UBS: Safe-Haven Logic Unchanged But Only Delayed.

- US-Iran Rift Persists, Will Gold Rise or Fall Next?

- Gold rallies on hopes for US-Iran talks and falling US Treasury yields

- Gold Price Forecast: XAU/USD opens lower around $4,450 on fears of widening Iran conflicts

- USD/JPY Hits 160.00 Mark, Will Japanese Government Intervene? Will the Currency’s Rally Be Contained?

- Seesaw Effect Continues. US Pre-Market Three Major Index Futures Weaken, Oil Prices Rise, Bitcoin Drops Below 68,000 Mark

Short-term Volatility, Long-term Optimism

At the latest GTC conference, Jensen Huang revealed that for the five quarters ending in 2026, the order backlog for Blackwell + Rubin has reached $500 billion, with projected delivery of 20 million chips over the coming quarters. These two figures significantly exceeded market expectations. When superimposed with the smooth mass production of Blackwell, Nvidia’s future revenue and EPS have been further revised upward. Currently, Nvidia’s forward PE sits around 28-30x. The recent stock correction—dropping about 15% from late October highs of $212 to mid-November lows of $181—reflects market uncertainty regarding the "sustainability of growth post-FY2027," rather than FY2026-FY2027 itself.

Prior to GTC, a series of collaborations landed by OpenAI further fueled market enthusiasm for AI: Nvidia (10GW), AMD (~6GW), Broadcom (10GW), and Oracle (4.5GW), totaling 30GW of demand. Calculated at an investment of $45-50 billion per GW, this corresponds to an AI infrastructure spend of $1.4–1.5 trillion. These orders are essentially locked in for delivery between 2026 and 2028, providing Nvidia with extremely high visibility in the near term.

It is worth noting that the current high growth of the AI industry chain does partially rely on a "closed-loop supply chain": the upstream (Nvidia) is highly profitable, while downstream model vendors (like OpenAI) may be facing annualized losses of $15–20 billion. This extreme bifurcation in profit distribution is an objective reality of the current phase, and it has triggered reasonable external concerns regarding "compute overcapacity" or a "bubble," leading to recent pullbacks in related stocks.

However, in the long run, this cycle of "upstream makes money first, then feeds downstream R&D, then accelerates application landing" is the standard path for all major infrastructure cycles (such as the Internet and Mobile Internet). Downstream model demand is rapidly shifting from "experimentation" to "scale monetization," providing strong support for upstream compute spending. OpenAI’s revenue was only $3.7 billion in 2024 but is projected to grow 440% YoY to $20 billion in 2025; Anthropic is also expected to surge 1000% from just $1 billion in 2024 to roughly $100 billion this year. Although they remain deep in the red, the sustained high growth in enterprise users, API calls, and payment penetration indicates that real demand is realizing rapidly. The key variable now lies in whether the downstream sector can significantly improve monetization efficiency in 2026–2027 (Enterprise AI, paid inference, incremental advertising, etc.). As long as this step is realized, profits will gradually migrate downstream, and overcapacity risks will be digested by real demand; conversely, we may see a temporary supply-demand mismatch.

Therefore, the market's current 28-30x forward PE has effectively paid a premium for the high growth of FY2026–2027 but has given limited credit to sustainability post-FY2027. This reflects caution but also leaves a margin of safety. As long as Nvidia continues to deliver on Blackwell/Rubin in the coming quarters—as it has in the past—and gradually provides clear visibility for FY2028, there is still room for valuation expansion. The current pullback is essentially "pricing in the uncertainty after FY2027" in advance; it is a typical fluctuation within a high-prosperity sector, not a trend reversal.

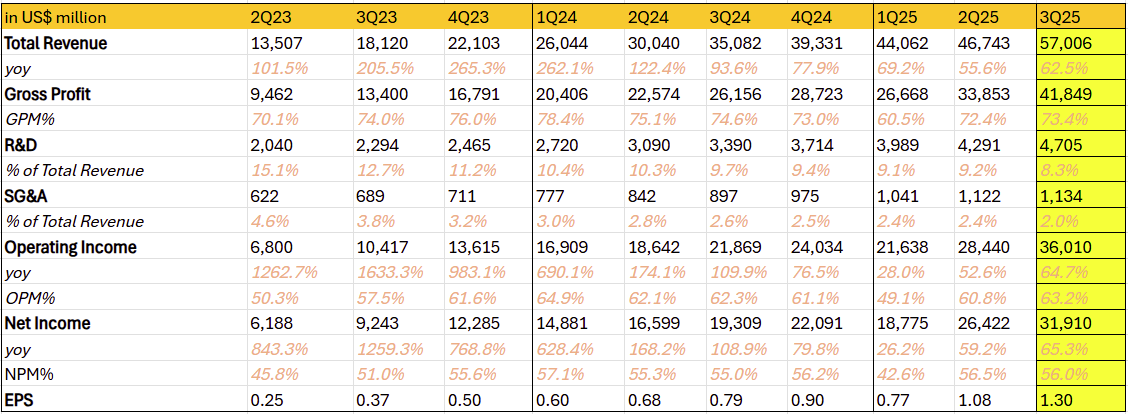

Key Financial Data Overview

Nvidia’s earnings report this quarter didn't just crush Wall Street’s most optimistic expectations with overwhelming performance; it provided the global tech industry with a definitive answer regarding the sustainability of AI infrastructure construction. On top of such a massive base, the stock surged over 6% after hours, driving a collective rally in AI-related stocks and effectively dispelling the anxiety of the "AI Bubble" theory.

Revenue: Nvidia continues to benefit from robust AI demand growth, particularly the explosive expansion of the Data Center business. Q3 revenue hit $57 billion, up 62.5% YoY, smashing market expectations of $55.1 billion.

Gross Margin: GAAP gross margin was 73.4%, up 0.9% QoQ but down 1.4% YoY. The sequential improvement was driven by product mix optimization and scale effects, proving that the negative impact of the China-specific H20 chip has faded. However, the year-over-year decline reflects rising production costs—specifically the sharp price increases in DRAM and NAND. These memory components make up a higher proportion of new generation high-performance chips like Blackwell, potentially leading to pricing pressure or supply chain fluctuations.

Operating Income: Performance was stellar with GAAP operating income at $36 billion (up 27% QoQ, 65% YoY). This was driven by strong revenue pull and relatively stable gross margins, highlighting Nvidia’s efficient operating leverage.

Net Income: Net income also hit a record high. GAAP net income was $31.9 billion (up 21% QoQ, 65% YoY); EPS was $1.30 (up 20% QoQ, 67% YoY). The company returned $37 billion to shareholders via buybacks and dividends this quarter and year-to-date, with $62.2 billion remaining in authorization, providing strong support for the stock price.

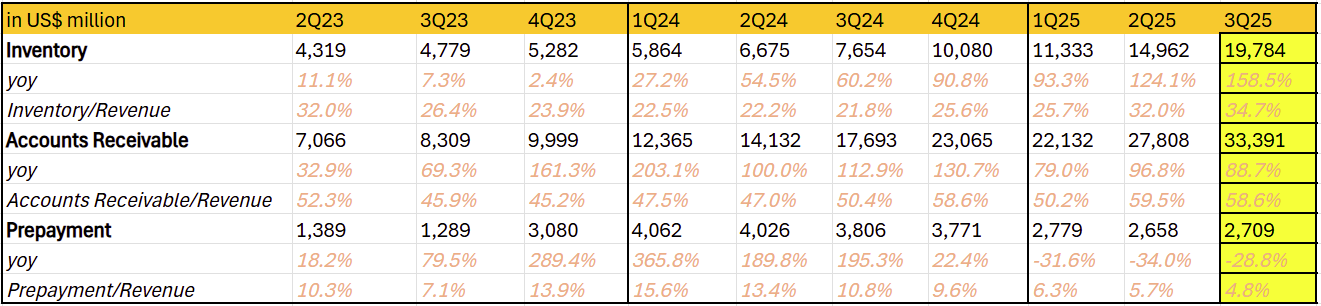

Cash Flow & Inventory: While inventory seemingly spiked 158.5% YoY to $19.8 billion, operating cash flow remained massive at $23.8 billion (+35% YoY), with free cash flow hitting a record $22.1 billion. The inventory buildup does not indicate weak demand; rather, it signals Nvidia’s strategic move to lock in capacity and supply ahead of surging Blackwell demand. Although accounts receivable jumped 88.7% YoY to $33.4 billion, the Days Sales Outstanding (DSO) remains healthy at 45 days. Inventory conversion and prepayment releases provided a buffer, ensuring cash flow was not dragged down.

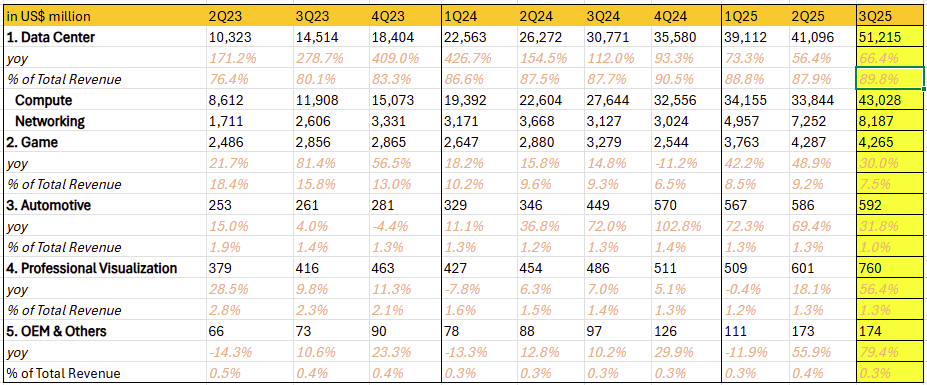

Data Center Business Breakdown

The Data Center business now accounts for roughly 90% of Nvidia’s total revenue, making it the absolute core determining the company's valuation anchor. Revenue for this segment reached $51.2 billion (+66% YoY), a historic high, driven primarily by the ramp-up of the GB series products.

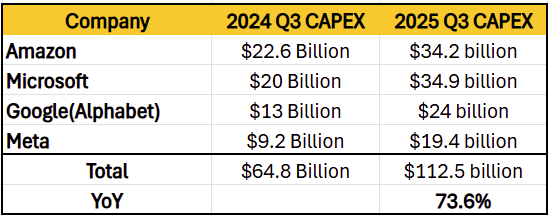

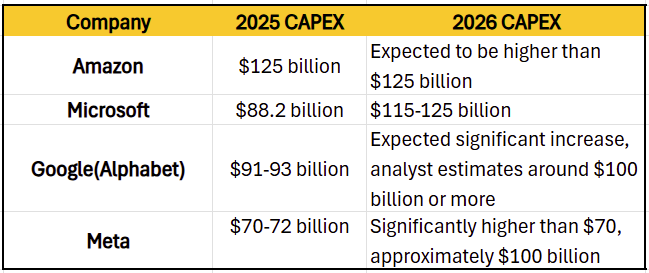

Compute Revenue: $43 billion (+56% YoY, +27% QoQ). The accelerated mass production of the B300 contributed the most significant incremental growth this quarter. Large cloud service providers (Hyperscalers) remain the biggest buyers of AI chips. This quarter, Google, Meta, Microsoft, and Amazon saw their capital expenditures (CapEx) surge nearly 74% YoY to roughly $112.5 billion, providing the strongest guarantee for Nvidia’s compute growth.

Networking Revenue: $8.2 billion (+162% YoY, +13% QoQ). The growth rate here is nearly three times that of the compute business, now making up roughly 16% of Data Center revenue. As AI models explode in size, the system bottleneck is shifting from "compute" to "interconnect." Training a model with trillions of parameters requires tens of thousands of GPUs working in unison like a single supercomputer; in this scenario, inter-GPU communication latency becomes the decisive constraint. Leveraging InfiniBand (from the Mellanox acquisition), the Spectrum-X Ethernet platform, and the NVLink + Copper full-rack solutions of the Blackwell era, Nvidia has built a formidable moat. This may become Nvidia's strongest and most durable "second growth curve" in the coming years.

Other Segment Performance

Gaming: Revenue reached $4.3 billion (+30% YoY), driven by hot sales of the RTX 50 series and the rise of the AI PC trend. Although its share of total revenue has dropped to 7.5%, compared to AMD’s Q3 Gaming revenue of $1.3 billion, Nvidia retains a dominant lead in the graphics card market.

Automotive: Revenue reached $592 million (+32% YoY, +1% QoQ). The sequential slowdown reflects cyclical adjustments in the auto industry, but the YoY growth benefits from the DRIVE AGX Hyperion 10 platform and the partnership with Uber.

Professional Visualization: Revenue reached $760 million (+26% QoQ, +56% YoY). Growth was driven by NVIDIA DGX Spark (the world's smallest AI supercomputer) shipments assisting professional AI workstation applications. While only 1.3% of revenue, it is highly efficient, benefiting from the penetration of the Omniverse digital twin platform in design/simulation, showcasing Nvidia’s expansion from hardware into the AI ecosystem.

Future Outlook

Nvidia forecasts next quarter's revenue to reach $65 billion (excluding assumptions for China AI GPU revenue), a QoQ increase of $9 billion, beating the market expectation of $61.6 billion. Gross margins are projected at 74.8%, a 1.4% sequential improvement, also beating the expected 74.4%, driven by the continued production ramp of the GB series.

Short-term: Nvidia’s earnings certainty is extremely high. Revenue is largely derived from the CapEx budgets of "Hyperscalers" (Microsoft, Meta, Google, Amazon), whose spending intent and cadence remain strong and predictable. Based on the latest earnings and management guidance from these giants, the strategic consensus that "the risk of under-investing and missing the AI era far outweighs the risk of over-investing and lower short-term returns" firmly dominates. Consequently, Big Tech has not cut 2026 AI infrastructure budgets but has widely and significantly raised CapEx plans. This trend provides extreme visibility and a high floor for Nvidia’s shipments over the next 4-6 quarters. Nvidia management reiterated in the earnings call: Total revenue for the second half of FY2025 through FY2026 will reach at least $500 billion. This guidance further reinforces market confidence in the high visibility of the next two fiscal years.

Long-term: Compared to the highly certain FY2025-2026, the market is more focused on the sustainability of growth in 2027 and beyond. Hence, Nvidia hasn't been awarded a higher valuation due to concerns over AI chip market share dilution and the long-term sustainability of Big Tech CapEx. Nvidia needs to continue validating its thesis through quarterly results—just as it has for the past two years—to gradually push the market to upgrade its long-range revenue and EPS expectations.

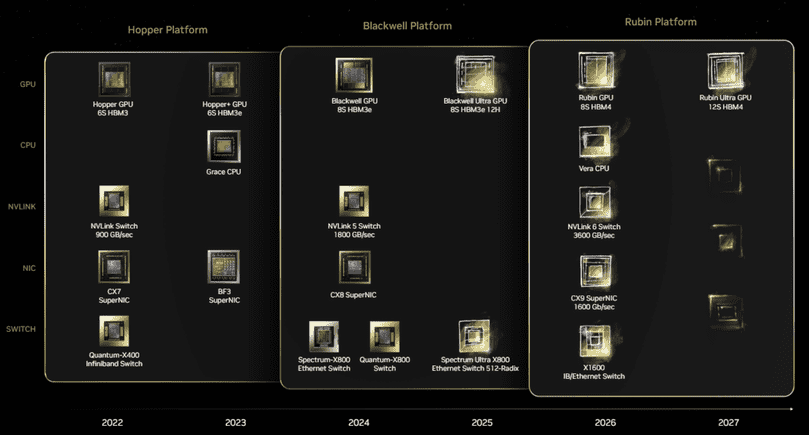

The Bull Case: Nvidia’s product roadmap is crystal clear: Rubin and CPX architecture (TSMC 3nm) launching in H2 2026, followed by Rubin Ultra in 2027, showing a steady rhythm of technical iteration. The China market risk has been fully "cleared," meaning any future movement there is pure upside. Furthermore, Sovereign AI has become strategic infrastructure for nations globally; Nvidia emphasized multiple times on the call that this sector is already contributing billions in orders and growing fast. Additionally, if OpenAI’s commercialization path becomes clearer, it will trigger another wave of upside surprises. These structural opportunities have not yet been fully priced in; as they materialize, valuation is expected to steadily move upward.

Potential Risks

Short-term Noise: Recent reports of liquidation or share reduction by entities like SoftBank and Bridgewater have, to some extent, shaken market confidence.

Customer Concentration: The vast majority of revenue comes from the top four cloud vendors. A significant spending cut by any one of them would cause a severe shock.

Technology Iteration Risk: If the next-generation Rubin architecture fails to deliver on schedule or suffers from major hardware defects, it would inflict substantial damage on the stock price.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.