Software Stocks Are Continuing to Rally, Should Investors Buy Oracle or Microsoft Now?

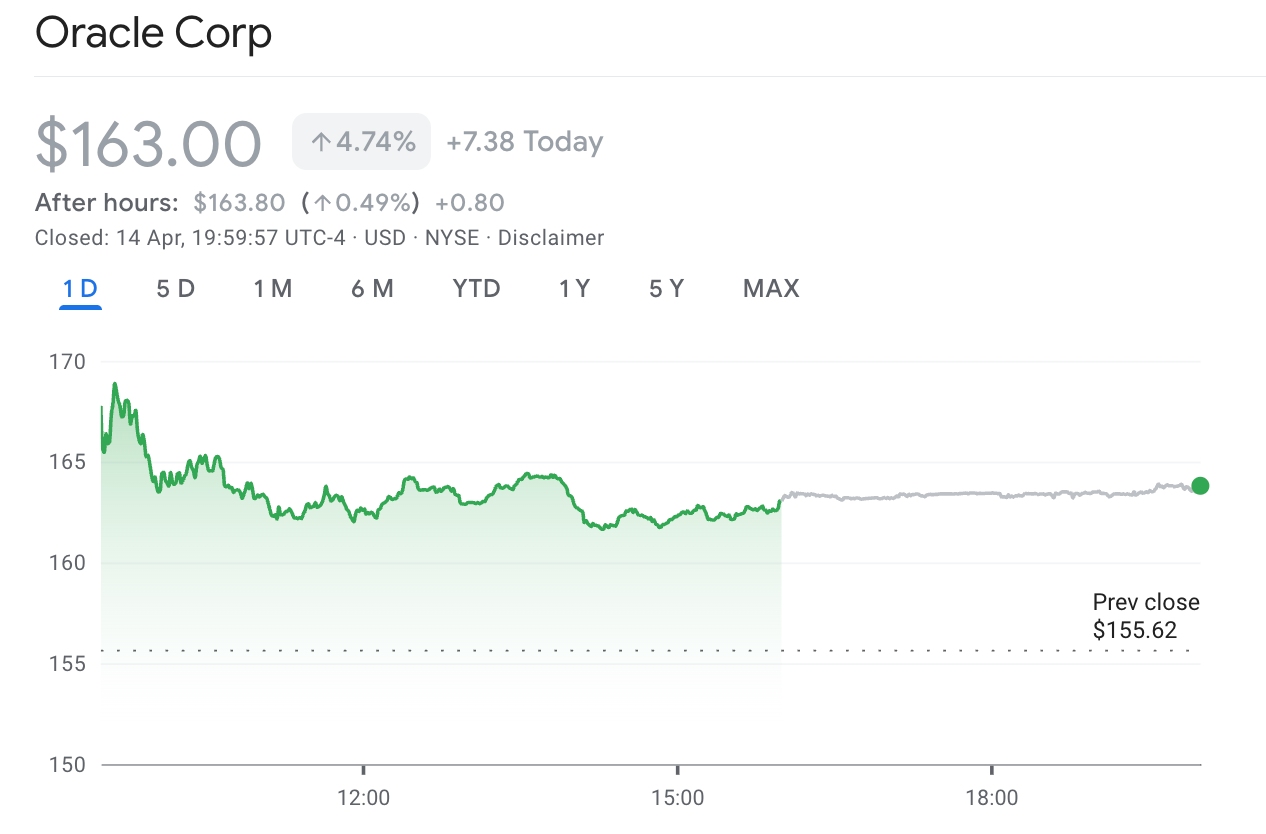

TradingKey - Following April 13, Oracle (ORCL.US) After its stock price surged 12.7% in a single day and its market capitalization increased by $50.4 billion, the stock continued its rally on April 14, rising another 4.74% to reach $163, as trading volume expanded to $9.783 billion.

[Oracle's stock price trend on April 14, Source: Google Finance]

The IGV software ETF rose sharply for two consecutive days, with a 5.4% jump on April 13 marking its largest single-day gain in a year; heavyweight stocks such as Microsoft, Palantir, and Salesforce also strengthened in tandem.

Previously, the rapid development of generative AI and AI agents had been shaking the foundations of traditional software business models. In early 2026, Anthropic released tools such as the enterprise-grade AI task assistant Cowork and Claude Code. These tools were promoted as potential AI alternatives to some SaaS products, triggering deep market concerns that the software industry would be disrupted by AI.

As a result, the software sector experienced a sustained and aggressive sell-off, with Oracle's year-to-date decline at one point exceeding 20%. Microsoft (MSFT) Its year-to-date decline also exceeded 20%.

Now that software stocks have rebounded across the board, which of these two giants, both deeply tied to OpenAI, should investors choose to achieve higher returns?

Oracle: A "Growth Stock" with High Growth and High Risk

Oracle's investment thesis is highly concentrated. As of the third quarter of fiscal 2026, total revenue reached $17.2 billion, up 22% year-over-year, while cloud infrastructure revenue surged 84% to $4.9 billion.

Remaining Performance Obligations (RPO) reached $553 billion, a year-over-year increase of over 300%, signifying that revenue for the coming years is effectively locked in.

However, Oracle's continuous cash outlays have rendered its cash flow extremely fragile. For the first three quarters of fiscal 2026, Oracle's free cash flow stood at -$43.8 billion, a stark contrast to the positive $26.2 billion recorded in fiscal 2025.

Capital expenditures for fiscal 2026 are projected to reach $50 billion; although the revenue target for fiscal 2027 is $90 billion, the capital expenditure forecast has yet to be disclosed.

Barclays previously predicted that Oracle could exhaust its cash by November 2026 and warned that its credit rating might be downgraded to BBB-, nearing junk status, as its debt-to-equity ratio has soared to 500%, far exceeding Amazon's 50% and Microsoft's 30%.

Oracle management has been responding proactively. During the Q3 earnings call, Clay Magouyrk, CEO of Oracle Cloud Infrastructure, revealed that \"over 90%\" of the company's planned 10-plus gigawatts of power and data center capacity over the next three years is \"entirely funded by partners.\" Furthermore, over $29 billion in new contracts were signed through \"bring your own hardware\" and prepayment models to \"continue expansion without consuming any of Oracle's negative free cash flow.\" The CFO also reiterated that an investment-grade rating will be maintained, with debt issuance for the year strictly capped at the previously announced $50 billion.

[Oracle Analyst Ratings, Source: TradingKey]

From an analyst perspective, Wall Street's average 12-month price target for Oracle is approximately $246, implying an upside of about 50%.

Microsoft: A "Cash Cow" with a Robust Ecosystem

Compared to Oracle's "all-in" strategy, Microsoft offers a starkly different path.

At the fundamental level, Microsoft has demonstrated stronger resilience. In the second quarter of fiscal year 2026 (the fourth quarter of 2025), Microsoft reported revenue of $81.3 billion, up 17% year-over-year, and net income of $30.9 billion, up 23% year-over-year. Azure cloud revenue grew 39% year-over-year, and Microsoft Cloud's quarterly revenue exceeded $50 billion for the first time.

Total commercial remaining performance obligations (RPO) reached $625 billion, with approximately 45% derived from OpenAI contracts, reflecting the strong pull-through effect of AI demand. In terms of profitability, Microsoft's operating margin is approximately 46.7%, far exceeding Oracle's 31.9%. Microsoft's free cash flow margin is a positive 25.3%, while Oracle's is -21.6%.

[Microsoft Analyst Ratings, Source: TradingKey]

Wall Street maintains a consistently high target price for Microsoft, with an average target price of $586, implying nearly 50% upside from current levels. Previously, Jefferies maintained a Street-high target of $675, and Morgan Stanley maintained its high target of $650.

Ahead of Microsoft's earnings release on April 29, Bernstein analysts noted: "Industry giants like Microsoft have not been left behind by the times; instead, they are actively embracing AI technology—the company has already invested billions of dollars in OpenAI. Furthermore, no AI model, no matter how advanced its coding technology, can replace Microsoft's infrastructure software and cloud services."

From a fundamental perspective, Microsoft may have the upper hand. For investors who prioritize stable fundamentals and a solid moat, Microsoft may be the superior investment target, as its performance indicates relatively stable growth potential. Conversely, Oracle may be more suitable for investors with a higher risk appetite who value its future development potential; however, it is important to note that while its stock price offers greater elasticity, there are significant risks, such as a prolonged lack of cash flow.

In terms of valuation ranges, following a deep correction, Oracle has fallen into the valuation range typical of normal growth stocks. Investors should pay close attention to whether its performance reveals a deceleration in growth or if its future room for expansion continues to broaden.

Recommended Articles