Big Short Burry’s Precise Strike, Trump Personally Saves the Day, Can Palantir’s Stock Price Hold Steady?

TradingKey - Currently, Palantir ( PLTR) is currently embroiled in a whirlwind of controversy between bulls and bears. On one side, renowned short-seller Michael Burry has triggered market volatility with a high-profile bearish stance; on the other, former U.S. President Donald Trump has personally voiced his support, causing the debate over the company's valuation and future competitiveness to escalate.

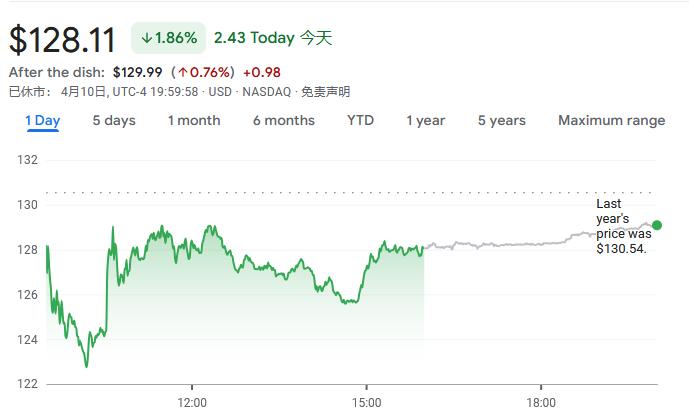

On April 9, Burry posted on X, claiming that Anthropic would erode Palantir's market share in the enterprise AI sector, while also revealing a large short position in the stock—though the post was quickly deleted. Impacted by the news, Palantir's stock price came under pressure, closing at $130.49 that day with a 7.3% decline.

Amid the bearish sentiment, Trump posted on Truth Social on the 10th to offer his support: "Palantir Technologies has been proven to possess top-tier combat capabilities and technical equipment; if you don't believe it, just ask our enemies."

Lifted by Trump's remarks, Palantir's stock rose as much as 5% intraday but ultimately closed down 1.8%, failing to reverse its downward trend for the week.

Following Trump's statement, Burry immediately clarified his position through a blog post, stating explicitly that he would not close his positions and would firmly maintain his bearish stance. He revealed that he had begun shorting Palantir as early as the fall of 2025 and has rolled over his positions multiple times, currently holding a significant number of long-term put options.

In his blog, Burry detailed: "I currently hold two types of put options: one set of contracts expiring on June 17, 2027, with a strike price of $50, and another set expiring on December 19, 2026, with a strike price of $100. I will not sell a single one today."

To date, Palantir's stock price has fallen by a cumulative 28% this year, a 38% decline from its 52-week high of $207.11 reached in November 2025.

Burry Says Palantir Valuation Still Too High Despite Being Cut in Half

Michael Burry, famous for accurately predicting the 2008 subprime mortgage crisis and whose story was adapted into the movie "The Big Short," has stirred the market's sensitive nerves with his recent bearish remarks on Palantir.

In fact, long before Burry spoke out, many investors and analysts had already questioned Palantir's high valuation, and the rapid expansion of AI startup Anthropic in the enterprise AI tool space is seen as a direct challenge to Palantir's business model.

Analysts point out that Palantir is now caught in a core contradiction; while its deep ties with the U.S. government provide stable revenue and a political "safety net," its high valuation makes it hypersensitive to any competitive threats.

During Trump’s second term, Palantir has secured a string of large government contracts, and its business expansion momentum has been swift; however, the recent sharp pullback in its share price sends a clear signal—the market still harbors deep doubts about whether the company can defend its existing share in the commercial AI segment.

This is precisely Burry’s short logic: as native AI companies like Anthropic accelerate their push into the enterprise market, Palantir’s competitive moat may be gradually eroded.

Burry explicitly stated that Palantir has shown weakness since its stock price hit a peak last year, and the current share price remains "severely overvalued," with its fundamental value less than half of its current market cap. He also admitted that a short-term rebound cannot be ruled out, but he will continue to hold put options and will definitely not "close out his positions."

Besides shorting Palantir, Burry has also intensified his short position on Nvidia by purchasing more put options with a $115 strike price expiring in January 2027, further signaling his concerns over a valuation bubble in the AI industry.

Why Trump Backs Palantir?

Trump's public endorsement of Palantir is no coincidence; the AI tech firm has long established a deep alignment of interests with the current U.S. administration.

Founded in the early 2000s by Peter Thiel, Alex Karp, and two others, Palantir has possessed a distinct "official background" since its inception—In-Q-Tel, the venture capital arm of the CIA, was an early investor.

From a business partnership perspective, Palantir's ties with various U.S. agencies have permeated core sectors; its proprietary Maven AI system has been fully integrated by the Pentagon, playing a critical role in real-time data analysis and decision support during military operations against Iran.

Concurrently, the company has secured several new contracts totaling over $1 billion with the Department of Homeland Security and Immigration and Customs Enforcement (ICE), directly participating in the Trump administration's controversial immigration enforcement actions.

Furthermore, several former Palantir employees have transitioned into government roles, and the company has retained a veteran lobbying team with close ties to the White House. Notably, CEO Alex Karp, a long-time Democratic supporter, donated $1 million to the Trump-aligned Maga Inc. super PAC in 2024; subsequently, he was not only invited to dine with Trump at the White House but also accompanied him on a state visit to Saudi Arabia, signaling a clear shift in political stance.

Palantir's formidable reputation is well-established globally; the firm provided critical data support in the operation to track down Osama bin Laden and, following the outbreak of the Russia-Ukraine conflict, has provided the Ukrainian military with technical support such as intelligence fusion analysis and AI-driven decision assistance.

In recent Middle Eastern conflicts, both the U.S. and Israeli militaries have fully deployed Palantir's Maven system. The U.S. version also integrates Anthropic’s Claude large language model, providing combat-proven validation of AI's capacity to enhance operational efficiency.

Currently, the Maven system has been deployed across all U.S. joint combatant commands, assisting the military in critical operational phases such as target identification and weapon pairing through digital battlefield situational awareness maps.

Market sentiment suggests that, through its deep entrenchment with U.S. military and intelligence agencies, Palantir is poised to be a direct beneficiary of Middle Eastern conflicts. This serves as the primary driver for the company’s continued acquisition of massive government contracts and deepened collaboration with the Pentagon during Trump's second term.

Wedbush Backs Palantir

Palantir's share price has indeed been under considerable pressure recently; however, the prominent Wall Street firm Wedbush believes that Anthropic's rise has not delivered a material blow to Palantir’s business.

Wedbush noted in its latest report that Palantir's core business growth drivers remain strong, with U.S. commercial revenue soaring 137% year-over-year and government business achieving 66% growth. As both segments advance in tandem, they exhibit a trend of accelerated expansion. Based on this judgment, Wedbush maintained its 'Outperform' rating on Palantir with a price target of $230, explicitly stating that reports of Anthropic 'cannibalizing Palantir's market' are merely amplified market rumors that do not align with the facts.

Industry analysis also indicates that Palantir's true competitive advantage lies in its deep 'moat' built around data, specifically the AIP platform's capacity for deep data integration within enterprise-level scenarios. This capability has not been supplanted by Anthropic's model technology; on the contrary, it has been further strengthened throughout the process of AI implementation.

Is Palantir Still a Buy?

Palantir's investment value requires a balance between its high-growth performance and elevated valuation risks. From a performance standpoint, the company is in a phase of explosive growth.

Full-year 2025 revenue reached $4.475 billion, up 56.18% year-over-year, with fourth-quarter revenue setting a record with 70% year-over-year growth. The company achieved a dual-engine drive of growth and profitability, with a 2025 operating margin of 57% and a simultaneous surge in free cash flow.

However, behind the stellar performance lies widespread market concern regarding its high valuation. Its current P/E ratio remains elevated; even based on 2026 projections, its price-to-free cash flow multiple reaches 94x, far exceeding the software industry average.

This high valuation is built on market expectations for sustained high growth. Should the company’s growth experience a marginal slowdown, the pressure for a valuation correction will increase significantly.

Furthermore, the risk of intensifying market competition cannot be overlooked. Although Palantir currently avoids direct competition with the likes of OpenAI through its differentiated focus on enterprise data integration and AI decision-making, continuous investment by tech giants such as Google and Amazon in cloud computing and data analytics may pose a threat to its market share.

Meanwhile, the company's deep ties to the government, while creating a high barrier to entry, also leave it susceptible to shifts in the political and legal landscape. Regulatory pressures related to data privacy and surveillance also remain a constant factor.

Analysts noted that for investors with a high risk tolerance who are optimistic about the long-term prospects of the AI decision-making sector, the company's growth potential may support further valuation digestion.

Recommended Articles