Nvidia's Jensen Huang Foresees $1 Trillion in Combined Sales for Blackwell and Vera Rubin Through 2027 -- but This Is Only Half the Story

Key Points

AI is Wall Street's hottest investment trend, with Nvidia's graphics processing units (GPUs) leading the charge.

Nvidia's CEO, Jensen Huang, expects the company's two newest GPUs to generate a baseline of $1 trillion in sales through 2027.

However, increasing internal competition, coupled with Taiwan Semiconductor expanding its production capacity, is a possible recipe for Nvidia's sales and margins to diverge.

- 10 stocks we like better than Nvidia ›

Arguably, no game-changing innovation has captured the attention and capital of investors quite like the evolution of artificial intelligence (AI). Empowering software and systems with the tools to make split-second decisions sans human oversight is a multitrillion-dollar addressable opportunity.

Among the laundry list of public companies benefiting from the artificial intelligence revolution is graphics processing unit (GPU) kingpin, Nvidia (NASDAQ: NVDA). Nvidia has added approximately $4 trillion in market value since the start of 2023 on the heels of its GPU dominance in AI-accelerated data centers.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

But it's not looking in the rearview mirror that has Wall Street and investors excited. It's recent commentary from CEO Jensen Huang that's raising eyebrows. The only problem is that Huang's trillion-dollar forecast may not tell the full story.

The "t" word has entered the picture

At Nvidia's annual GPU Technology Conference (GTC) in mid-March, the company's billionaire boss outlined a sales forecast for its two most-advanced GPUs, Blackwell and Vera Rubin (the latter of which debuts later this year), containing the "t" word... trillion. Said Huang,

I'm here to tell you that right now, where I stand -- a few short months after GTC DC, one year after last GTC -- right where I stand, I see through 2027, at least $1 trillion.

Baseline combined sales of $1 trillion for Blackwell and Vera Rubin would be jaw-dropping. It would solidify Nvidia's AI hardware as the undisputed top choice by businesses in enterprise data centers.

Furthermore, this $1 trillion estimate demonstrates the often-overlooked importance of the CUDA software platform. This is the toolkit developers use to maximize the compute capabilities of their Nvidia GPUs, including the building and training of large language models.

But while this $1 trillion Blackwell-Rubin sales forecast likely has investors seeing dollar signs, it may only be telling half the story.

Internal competition may weigh on Nvidia's gross margin

Inevitably, Nvidia is going to face increased GPU competition. However, its biggest competitive risk might come from within.

Many of the company's largest customers by net sales are currently developing GPUs and solutions to use in their data centers. Even though these internally developed chips are several rungs of the ladder below Nvidia's hardware, they do have the advantage of being notably cheaper and more readily available.

Compounding this increase in internal competition is the reality that world-leading chip fabricator, Taiwan Semiconductor Manufacturing, is steadily expanding its monthly chip-on-wafer-on-substrate (CoWoS) capacity.

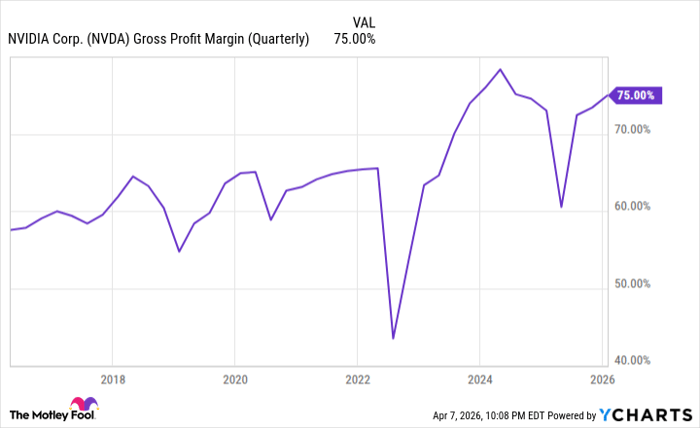

NVDA Gross Profit Margin (Quarterly) data by YCharts.

One of Nvidia's foundational catalysts has been persist GPU scarcity. While its GPUs maintaining compute superiority has helped with its pricing power and gross margin, GPU demand handily outstripping supply has been even more important.

With Taiwan Semi rapidly expanding its monthly CoWoS wafer capacity, and Nvidia's customers intent on deploying internally developed chips in their data centers, the GPU scarcity that's fueled Nvidia's pricing power will likely wane over time.

Taiwan Semi's ability to handle more GPU output can help facilitate Huang's prognostication of $1 trillion in combined sales for Blackwell and Vera Rubin through 2027. But at the same time, Nvidia's gross margin may erode as GPU scarcity fades. In other words, Huang's trillion-dollar forecast is only half the story.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $536,003!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,116,248!*

Now, it’s worth noting Stock Advisor’s total average return is 946% — a market-crushing outperformance compared to 190% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of April 10, 2026.

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Recommended Articles