Vertiv Is Quietly Powering Every AI Data Center in America, and the Stock Could Double

Key Points

The technology specialist for data centers reported strong revenue and earnings growth last year.

Vertiv is well-positioned thanks to accelerating AI infrastructure investments by hyperscalers.

Its stock remains attractively valued relative to many growth stocks in the AI arena.

- 10 stocks we like better than Vertiv ›

It's been a challenge navigating the technology sector so far in 2026. While megacap artificial intelligence (AI) stocks were once considered near locks for market-beating gains, recent selling pressure has investors thinking twice.

While hyperscalers in particular continue to face scrutiny, growth can still be found elsewhere. Take Vertiv Holdings (NYSE: VRT) as a prime example: Shares have skyrocketed 62% so far this year -- absolutely dominating the "Magnificent Seven," S&P 500, and Nasdaq-100.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Let's dig into the catalysts fueling Vertiv right now and explore why the stock's rally could be just getting started.

Image source: The Motley Fool.

Vertiv had a monster 2025, and...

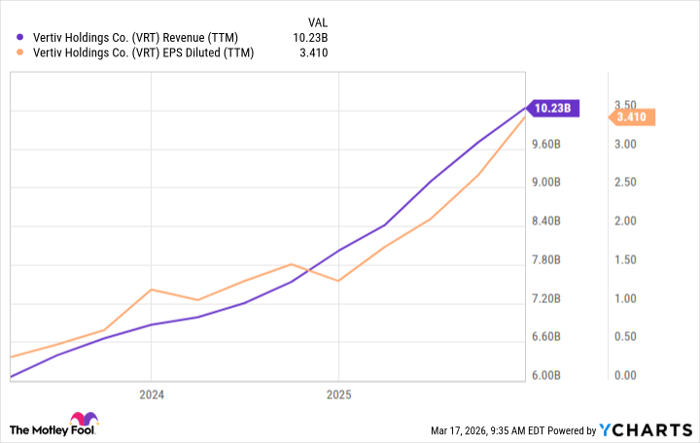

Vertiv specializes in power and cooling solutions for data centers. Over the last few years, the company's revenue has supercharged thanks to rising investment in AI infrastructure. Even better, however, is Vertiv's profitability. Per the trends below, the company has been able to command strong unit economics across its thriving data center empire -- expanding earnings growth in tandem with soaring revenue.

VRT Revenue (TTM) data by YCharts

The subtle theme from the figures above is that Vertiv's revenue and earnings-per-share (EPS) growth are getting steeper. In other words, the company's financial profile is accelerating. But don't just take my word for it.

Consider that during the company's fourth-quarter earnings report, management guided for 2026 revenue between $13.3 and $13.7 billion, EPS in the range of $5.97 to $6.07, and free cash flow up to $2.3 billion. At the midpoints, this represents annual revenue and earnings growth of roughly 28% and 43%, respectively.

...this year will be even better

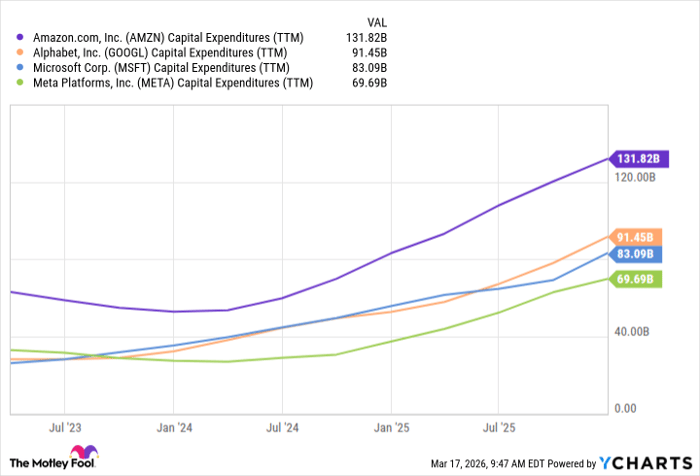

The big question smart investors are asking is: What factors are driving such enormous growth for Vertiv? The answer is simple: In 2026, AI hyperscalers Microsoft, Amazon, Alphabet, and Meta Platforms are forecasting to spend up to $700 billion in capital expenditures (capex).

AMZN Capital Expenditures (TTM) data by YCharts

These behemoths have been major purchasers of Nvidia's industry-leading graphics processing units (GPUs) throughout the AI revolution. These trends do not appear to be slowing down in the slightest, as Nvidia CEO Jensen Huang just revealed that he thinks the company's AI chip backlog could reach $1 trillion by 2027.

These are important details to understand because Vertiv has a strategic partnership with Nvidia. As big tech continues to allocate hundreds of billions of dollars of capital toward chip procurement and data center build-outs, Vertiv should capture some of this spend, given its role in the AI infrastructure value chain.

Against this backdrop, I think it's highly likely that Vertiv is positioned to continue riding AI-driven secular tailwinds throughout 2026 and beyond.

Will Vertiv stock double in 2026?

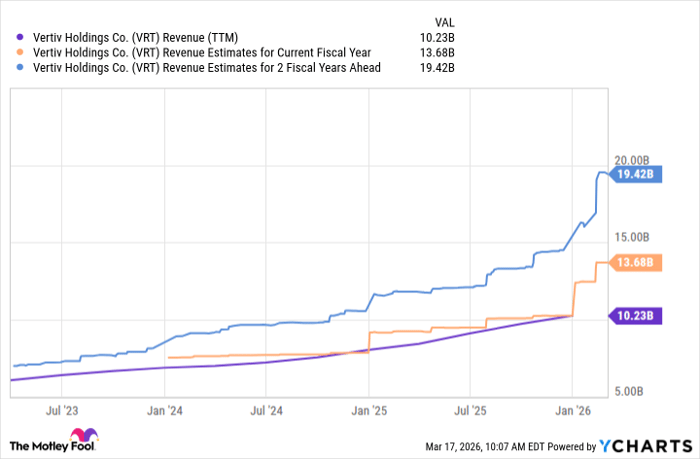

Given the company's 2026 guidance, ongoing AI infrastructure supercycle, and ties to Nvidia, Vertiv should continue delivering robust growth across the top and bottom lines.

VRT Revenue (TTM) data by YCharts

With that said, since shares have already torched the market this year, it's natural to think Vertiv stock has gotten ahead of itself and is benefiting from unsustainable momentum. Savvy investors understand that looking at percentage gains in isolation doesn't help much when it comes to assessing a company's underlying valuation profile, though.

Vertiv currently trades at a price-to-sales (P/S) ratio of 10. Should Vertiv achieve the forecasts above -- which seems doable considering the company already has a $15 billion backlog -- a modest P/S rerating in the range of 12 to 14 could double Vertiv stock.

This valuation profile is still well below many hypergrowth AI stocks. To me, this suggests that Vertiv remains undervalued and could be positioned for meaningful valuation expansion throughout the AI infrastructure era.

Given the company's multi-year runway and ability to directly benefit from ongoing infrastructure investment from hyperscalers, I find Vertiv's growth narrative quite compelling. For these reasons, I see the stock as a no-brainer buy right now and think its rally is just beginning. By year-end, I think Vertiv stock could easily become a multibagger.

Should you buy stock in Vertiv right now?

Before you buy stock in Vertiv, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Vertiv wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $494,747!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,094,668!*

Now, it’s worth noting Stock Advisor’s total average return is 911% — a market-crushing outperformance compared to 186% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 20, 2026.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Vertiv. The Motley Fool has a disclosure policy.

Recommended Articles