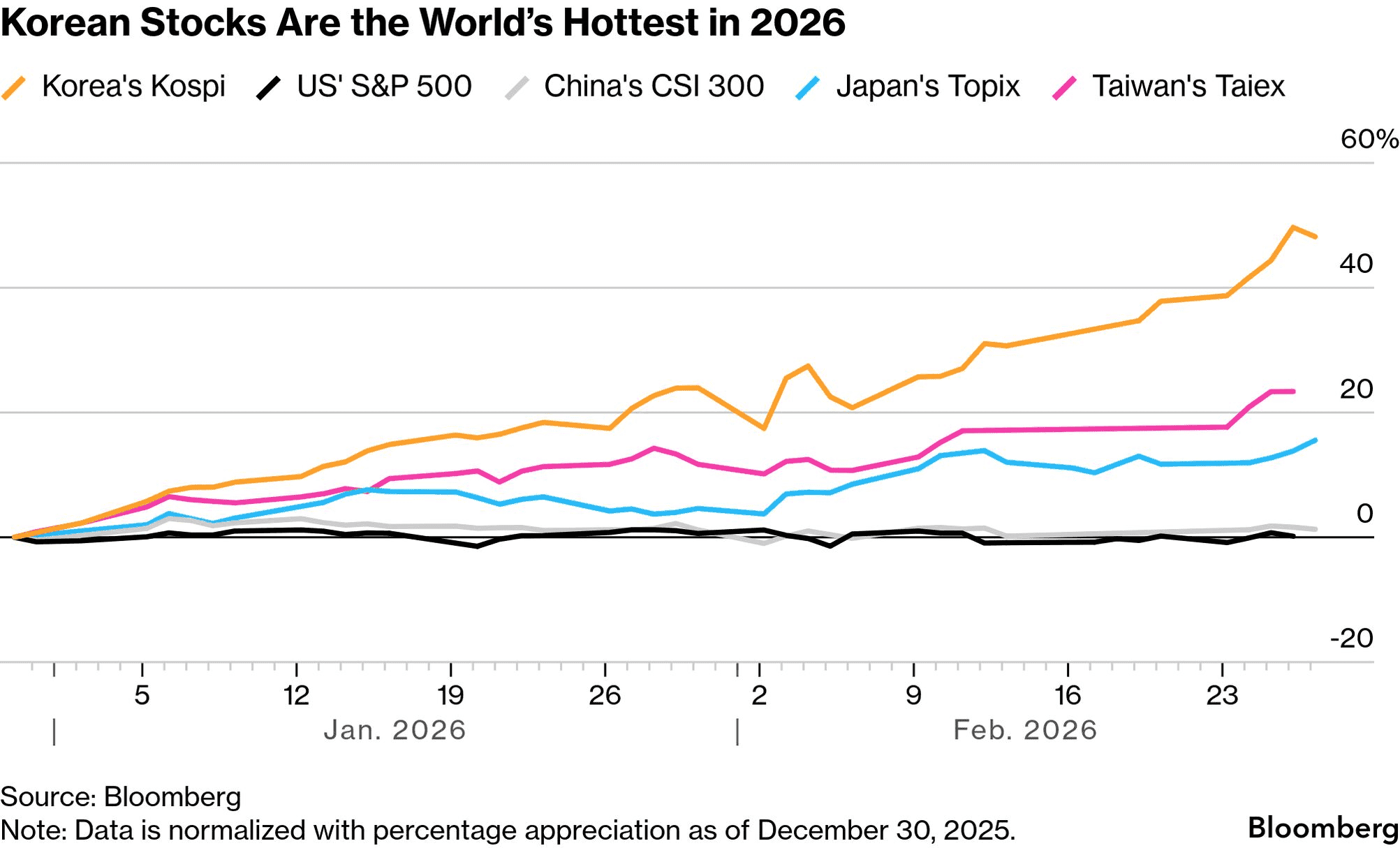

Korean Stocks Up 47% YTD: How to Join the Rally

TradingKey - Since the start of 2026, South Korea’s KOSPI Index has been on a tear — rising more than 47% so far this year and lifting the market’s capitalization to ninth place globally. That performance makes it one of the brightest stars among major equity benchmarks.

Source: Bloomberg

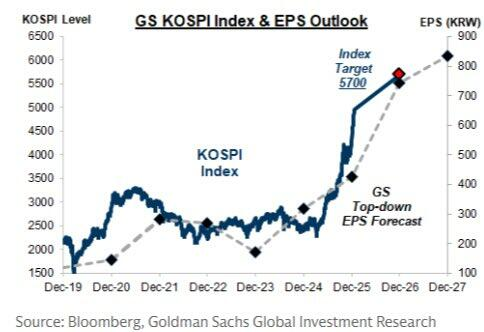

Goldman Sachs (GS) noted in a report earlier this month that, in U.S.‑dollar terms, the MSCI Korea Index is leading gains across Asia‑Pacific. Despite the strong run, the bank advised against taking profits and instead raised its 12‑month KOSPI target to 6,400.

Samsung and SK Hynix Drive the KOSPI Rally

This surge has been powered by a memory‑chip supercycle centered on Samsung and SK Hynix . The two giants carry heavy weights in the KOSPI and have soared on exploding demand for AI storage and HBM (high‑bandwidth memory). Together, they’ve contributed an outsized share of the index’s advance. Local media put it bluntly: “Without Samsung and Hynix, there would be no KOSPI at 6,000.”

At the same time, analysts have systematically upgraded earnings forecasts for both companies, prompting a broader repricing of large‑cap valuations across Korea’s equity market.

Source: GS

Foreign and Domestic Money Flow Back In

According to The Korea Times, foreign investors are flooding back, shifting their stance from long‑term underweight to active overweight on Korea. For years, global funds avoided Korean assets, held back by a sluggish memory cycle, governance discounts, and the country’s “emerging‑market” label.

That changed in 2025–2026. As continued monetary ease and reform expectations rose, foreign investors turned into steady net buyers. Their share of total KOSPI market capitalization climbed to roughly ₩1,327 trillion in 2025, ending years of withdrawals.

So far in 2026, passive index trackers, active managers, and hedge funds have all expanded Korean exposure, placing the country squarely in the “AI + reform” theme basket.

Domestic capital is also returning. With rates seen peaking and real estate cooling, local funds have begun shifting from property and deposits into equities. Retail investors are joining through mutual funds, pensions, and direct stock purchases, while insurance firms and retirement systems are boosting equity allocations for the long run.

Governance Discount Finds a Real Response

To understand why this rally feels different from past cyclical rebounds, look to the long‑debated issue of Korea’s “governance discount” and the Lee Jae‑myung administration’s changing tone.

For decades, the Korean market was tagged as “cheap — but cheap for a reason.” Investor skepticism stemmed from ownership structures favoring controlling shareholders, leaving minorities weak on dividends, buybacks, capital allocation, and disclosure. Put simply, markets weren’t convinced profits would ultimately flow back to all shareholders. That uncertainty demanded valuation compensation — the essence of the governance discount.

Since Lee Jae‑myung took office, his government has explicitly prioritized improving corporate governance and increasing market appeal. For institutional investors, this policy shift has transformed Korea’s image from a “structurally discounted” market into one undergoing valuation repair through reform.

As expectations shifted, investors recalibrated the discount downward. Hence, while the memory‑earnings cycle turned up, the KOSPI’s valuation multiple also lifted, breaking the pattern of “strong earnings, static P/Es” that defined previous recoveries.

Macro Tailwind and Regional Reallocation

Beyond governance optimism, macro conditions are boosting Korea’s momentum. The country’s economy sits at the intersection of AI and global manufacturing. As a major base for semiconductors, display panels, EV batteries, and autos, Korea is capturing part of the production migrating from single‑supply chains to more diversified geographies.

The Bank of Korea recently raised its growth outlook and signaled it would keep policy settings steady for at least six months, preserving abundant liquidity for equities — though soaring Seoul property prices still complicate decisions. Economists such as Deutsche Bank strategist Juliana Lee remain more optimistic on Korea’s prospects than the consensus view.

In this blend of policy support and industrial depth, investors now see Korea as a comprehensive allocation target backed by a durable macro base.

Investing in Korea via ETFs

Recent foreign‑broker reports suggest that most analysts don’t see the rally as finished. Instead, they describe it as the first half of a longer rerating phase.

J.P. Morgan Chase & Co. (JPM) has raised its KOSPI target to around 7,500 points — still leaving double‑digit upside potential. Nomura Holdings Inc. (NMR) argues that as capital rotates from a “pure U.S. AI trade” to a “global AI supply‑chain allocation,” Korea stands out as a prime beneficiary. Deutsche Bank, meanwhile, emphasizes the country’s “valuation‑repair story,” noting that current price‑to‑earnings ratios remain reasonable relative to earnings potential. If governance reform materially lifts shareholder returns, it expects long‑term allocations from pensions and sovereign funds to rise further.

Here are the ETFs you can invest in Korea.

The Franklin FTSE Korea ETF (FLKR) allocates roughly 47% to information technology, 19% to industrials, and 12% to financials. Its top holdings, Samsung and Hynix, dominate the portfolio with weights of 21.6% and 20.0%, respectively. FLKR carries an annual expense ratio of 0.09% and yields 2.87%. The fund gained 26.6% over the past month and 127.3% over the past year.

The iShares MSCI Korea ETF (EWY) shows a similar pattern, with 50% in information technology, 18% in industrials, and 11% in financials. Samsung and Hynix account for 28.4% and 19.0% of the fund’s weight. EWY has an annual expense ratio of 0.59% and a dividend yield of 1.53%. It climbed 26.3% in the past month and 133.4% over the past year.

Meanwhile, the First Trust Asia Pacific ex‑Japan AlphaDEX Fund (FPA) keeps about 53.6% of assets in Korea, while the iShares Asia 50 ETF (AIA) allocates roughly 25.9% to Korean equities.

Recommended Articles