Why Tesla Stock Could Double as Optimus Reaches Human-Level Proficiency This Year

Key Points

Tesla is transitioning its manufacturing plant in Fremont, California, to a factory focused on producing the Optimus robot.

Tesla could turn Optimus into a high-margin services business similar to what it's done with its self-driving software platform.

Wall Street is forecasting Tesla's earnings to double over the next couple of years.

- These 10 stocks could mint the next wave of millionaires ›

Throughout the artificial intelligence (AI) revolution, Tesla (NASDAQ: TSLA) stock has experienced a number of pronounced peaks and valleys. Whether it's Elon Musk's foray into politics, an electric vehicle (EV) business in decline, or ongoing delays with the company's long-awaited robotaxi service, it's never boring over at Tesla.

Nevertheless, the stock has been resilient, and recent price action suggests investors are generally optimistic. One of the biggest catalysts fueling Tesla's enthusiasm is the company's humanoid robot, Optimus.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Let's dig into how Tesla plans to scale the Optimus business and assess how robotics could become the key to a compounding earnings profile in the long run.

Image source: Tesla.

Tesla is trading cars for robots

At the end of January, Tesla reported earnings for the fourth quarter and full year 2025. Musk notified investors that the company plans to pivot some of its manufacturing capacity in Fremont, California, to wind down production of the Model S and X vehicles.

As production comes to an end for these EV models, Tesla will transition part of Fremont into a space focused on Optimus in lieu of the Model S and X.

Understanding the high-margin robotics model

You might not think that robotics offers robust profit margins, given that these devices require substantial capital outlays for research and development (R&D) and capital expenditures (capex).

One way Tesla has built a profitable business is by integrating high-margin services into its core hardware products. Take the EV business. Broadly speaking, buying a car is a one-time purchase -- or at the very least, a nonrecurring purchase.

Tesla's vehicle business is supplemented by a services platform featuring the company's autonomous driving technology. In other words, if you want access to Tesla's Full Self-Driving (FSD) software, you need to sign up for a subscription. Wrapping a high-margin, recurring-revenue software service around the capital-intensive EV business has helped Tesla generate healthy gross margins and free cash flow.

Tesla will likely employ a similar playbook with Optimus. In addition to the one-time hardware sale of the robot itself, customers will pay a subscription fee alongside that allows Optimus to function, learn new tasks, and improve dexterity over time.

The financial potential of Tesla Optimus

Humanoid robots have the potential to add trillions of dollars of economic value by delivering unprecedented levels of efficiency to the labor force. But Tesla is far from the only company exploring humanoids.

Moreover, Musk indicated that initial production of Optimus Gen 3 is likely to begin only at the end of this year. This is all to say that Optimus won't materially impact Tesla's financial profile for several years.

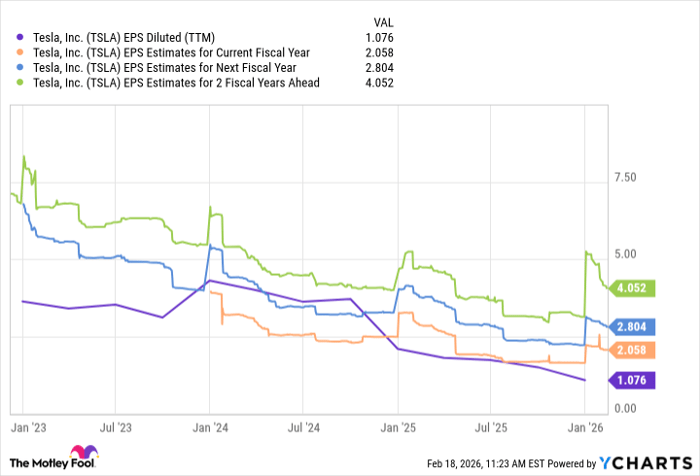

TSLA EPS Diluted (TTM) data by YCharts

Here is where things get interesting: Wall Street forecasts Tesla's earnings to return to growth this year. By 2028, the company's earnings per share are expected to double. That may not seem like much, but the gap between Tesla's trailing-12-month EPS and its 2028 expected earnings implies significant growth ahead.

This profitability will not be driven solely by more EV sales. Rather, it appears that Wall Street anticipates Tesla successfully executing on its AI vision and beginning to scale Optimus in a material way over the next couple of years.

Should Tesla meet or exceed these expectations, the stock could be in a position to double as earnings growth compounds thanks to the company's dominance in the physical AI realm.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $492,341!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $50,381!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $424,262!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

See the 3 stocks »

*Stock Advisor returns as of February 24, 2026.

Adam Spatacco has positions in Tesla. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

Recommended Articles