Palantir Q3 2025 Earnings: Blowout Performance Can’t Hide an AI Bubble, Four Growing Risks Behind a Nearly 1,000x Valuation

TradingKey – After the close of trading on November 4, “AI application King” Palantir Technologies (PLTR) reported its third-quarter earnings for fiscal year 2025. Despite a blowout quarter, surging top-line growth, and a flood of commercial orders, the stock plunged in after-hours trading.

Adding fuel to the fire, famed “Big Short” hedge fund manager Michael Burry disclosed a $1 billion short bet against Palantir—a move that raises a critical question: what’s the disconnect between Palantir’s performance and its share price action?

Let’s break down the numbers and look under the hood.

Q3 2025 Overview

Palantir reported Q3 revenue of $1.18 billion, up 63% year-over-year and 18% sequentially, once again crossing the billion-dollar mark in quarterly revenue. Results blew past consensus estimates of $1.09 billion, marking the 21 consecutive quarter of beating market expectations.

Even more notably, net profit soared—from $140 million in the same quarter last year to $480 million, representing more than a 2x YoY jump and 46% QoQ growth.

Segment Breakdown:

1. Commercial Business:

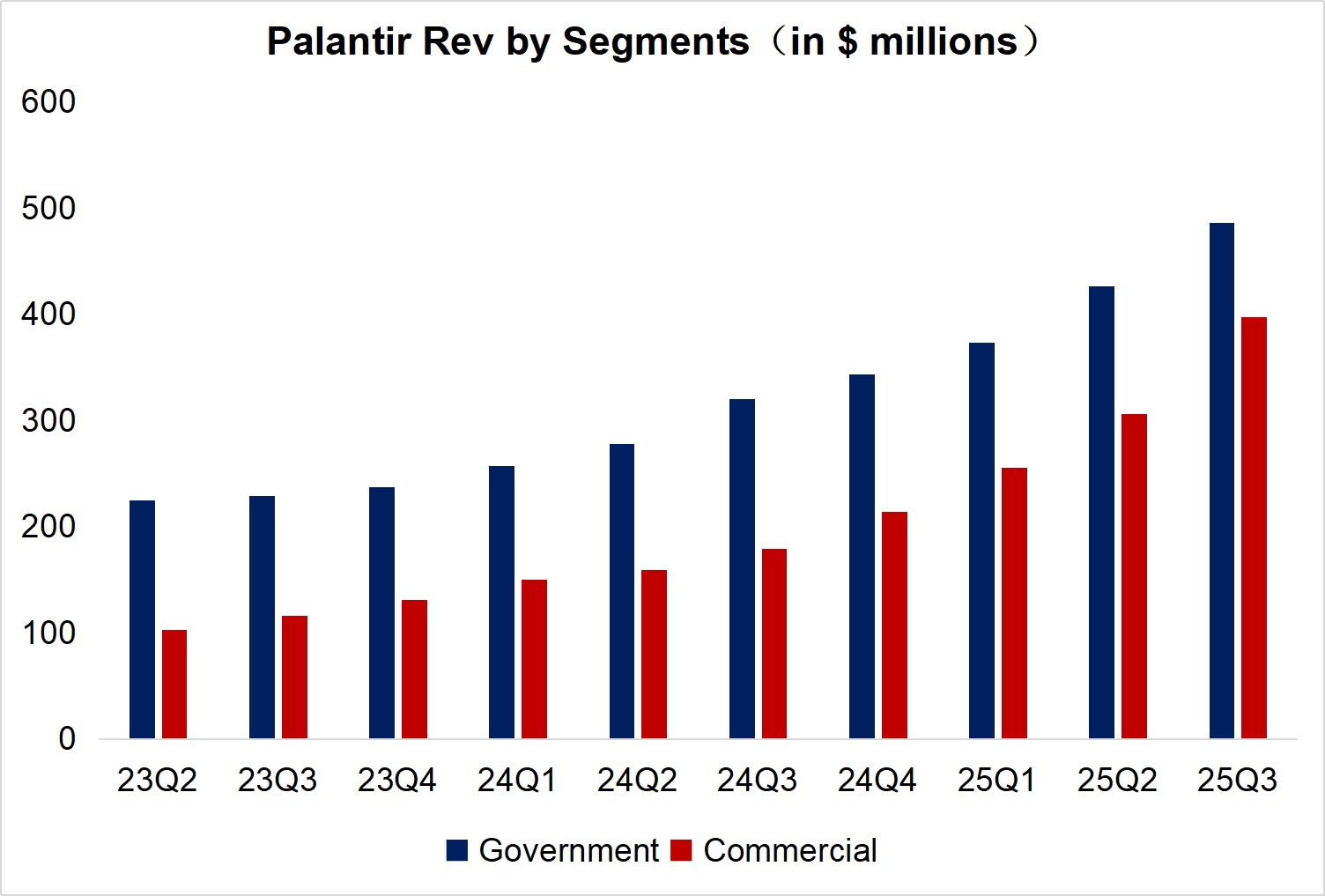

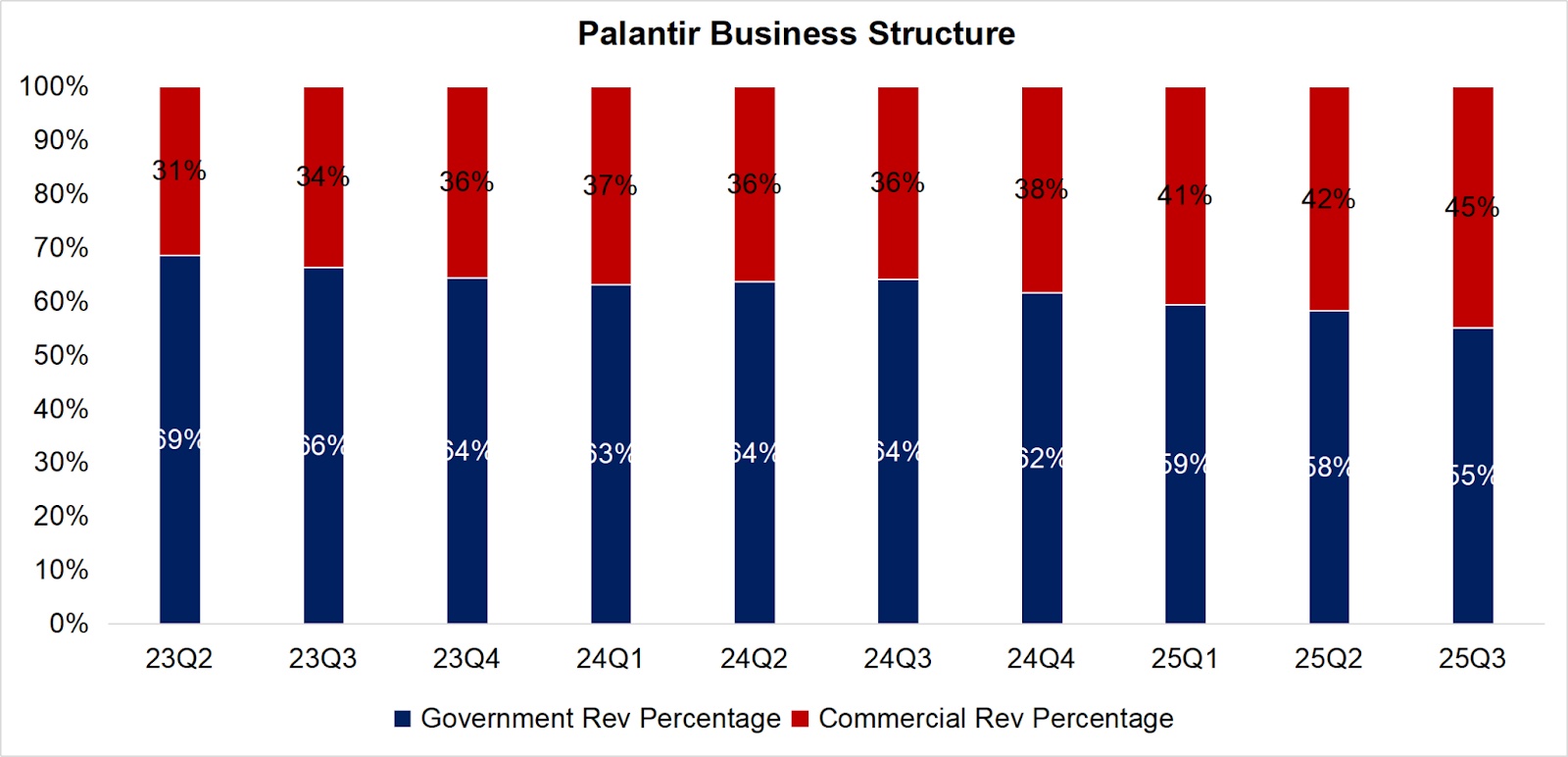

Palantir’s key growth engine continued to outperform, with commercial revenue increasing from $30.6 billion last quarter to $39.7 billion this quarter—a 30% sequential bump. Commercial now accounts for nearly half of total revenue.

This strength is being driven by greater uptake of AIP (Artificial Intelligence Platform) standardized templates, which are reusable across industries—improving both gross and net margins through scale. Q3 gross margin rose to a striking 82%, while net margin hit an impressive 40%, up 1.7 and 7.7 percentage points respectively from Q2.

Customer retention and expansion are also accelerating. Lead clients are increasingly shifting from purchasing individual modules to full-suite solutions, powered by cross-sector portability of AIP templates. Contract value from signed commercial deals skyrocketed 4x this quarter to $1.31 billion.

2. Government Business:

Palantir’s foundational government segment remains a reliable base. Revenue grew from $42.6 billion in Q2 to $48.6 billion, a 14% sequential increase. While U.S. federal agencies remain the anchor customers, Palantir continues to expand internationally, gaining traction with clients like the UK, Germany, and Poland—broadening its NATO-related revenue streams.

Data Sources: Reuters, TradingKey As of: November 4, 2025

Data Sources: Reuters, TradingKey As of: November 4, 2025

Key Questions from Investors

1. Are major enterprise clients expanding their purchasing scope?

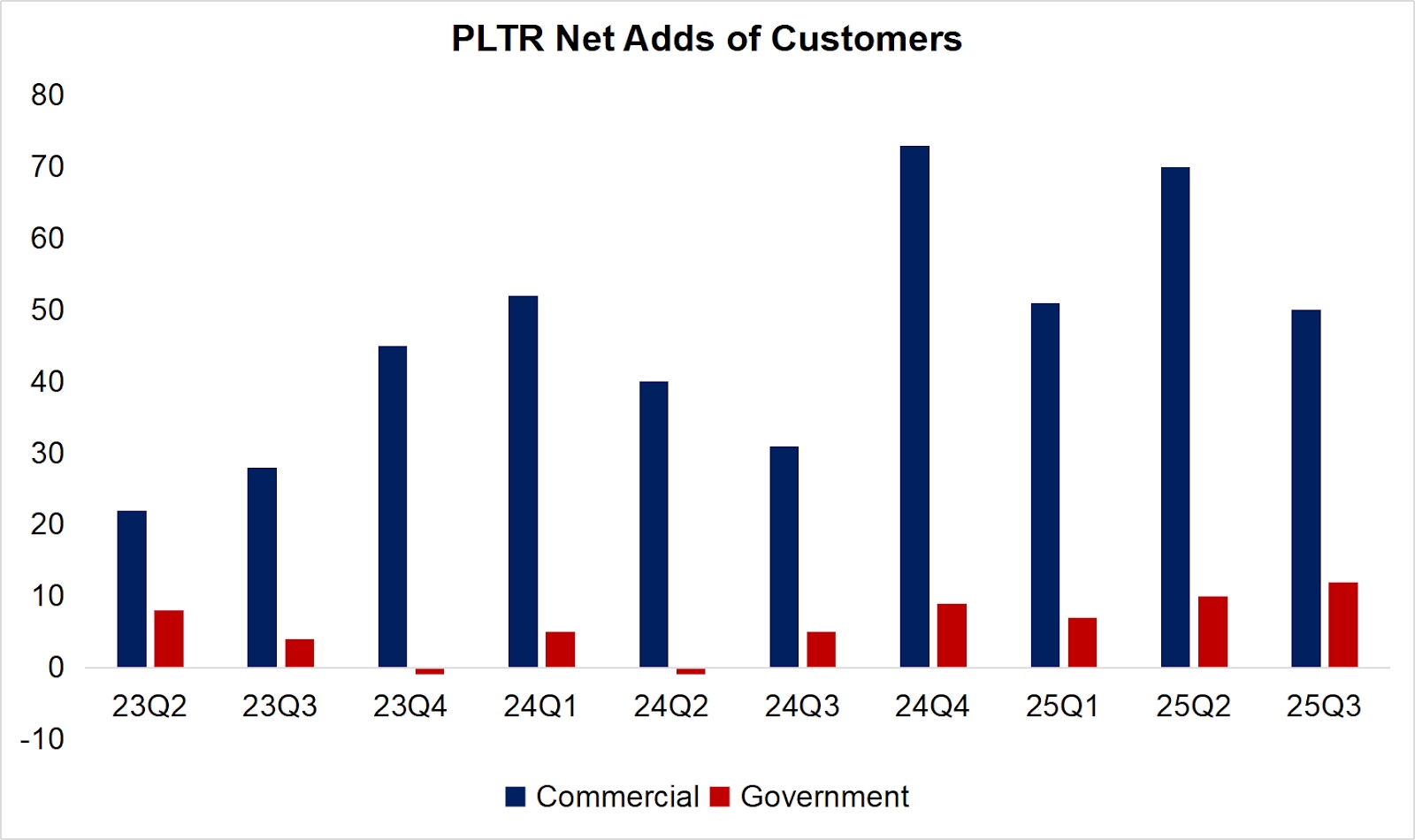

Yes. Both commercial and governmental customers continue increasing their usage, particularly enterprises based in the United States. Palantir added a net 62 new clients this quarter, of which 50 were from the commercial segment—and 45 of those were U.S.-based. Industry penetration expanded beyond defense and financial services, reaching healthcare, energy, manufacturing, and more.

Data Sources: Reuters, TradingKey As of: November 4, 2025

2. What’s the status of order conversion and operational metrics?

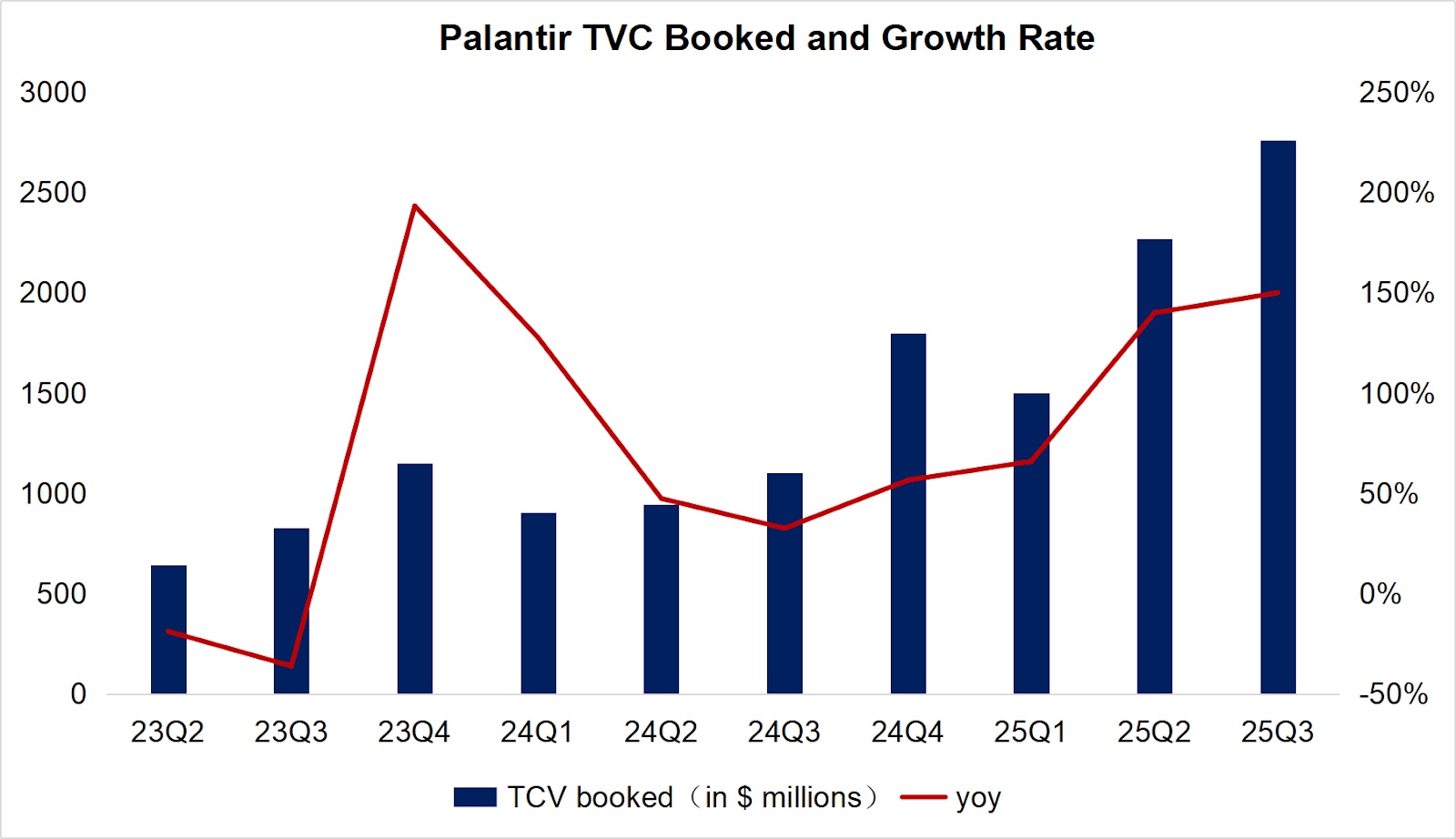

Palantir's total contract value (TCV) for Q3 rose sharply to $2.76 billion, up $490 million from the prior quarter. Remaining performance obligations (RPO) came in at $2.6 billion—signifying revenue from signed but not yet recognized contracts. While RPO grew 66% YoY, QoQ growth slowed to $180 million, showing a noticeable deceleration compared to previous quarters.

Data Sources: Reuters, TradingKey As of: November 4, 2025

3. How sticky are legacy clients? Any signs of expansion?

Customer loyalty is strengthening, with strong top-ups from existing clients. Overall contract liabilities (including client deposits) grew by $50 million sequentially. Existing customer spend growth hit 134% YoY, and Palantir’s U.S. commercial net dollar retention rate surpassed 130%—meaning average client spend rose more than 30% YoY.

4. What’s the latest on government pipeline and defense partners?

As the U.S. and NATO nations prepare for significant defense budget expansions in the upcoming fiscal year, Palantir is well positioned to benefit. NATO partners have begun piloting Palantir’s AIP system in joint military exercises. The company expects to further grow this channel, with potential pipeline value north of $5 billion.

Balance Sheet: Strong Liquidity, Minimal Financial Risk

As of Q3 2025, Palantir’s balance sheet remains exceptionally strong. The current ratio stands at 6.43—well above the industry benchmark of 1.5—thanks to a wave of new business and efficient cash cycle management.

Notably, Palantir holds virtually no interest-bearing debt, and most liabilities stem from operating activities. Its $6.4 billion cash reserve (including equivalents and short-term Treasuries) accounts for a stunning 78.9% of total assets, giving the company ample firepower for continued AI R&D and global expansion.

Cash Flow: High Earning Quality, Strong Momentum

Palantir recorded Q3 net profit of $476 million and operating cash flow of $508 million—a gap of only $32 million, suggesting robust earnings quality. Adjusted free cash flow reached $540 million, a 46% margin on quarterly revenue. These surplus flows offer ample support for R&D investment (e.g. AIP upgrades) and aggressive customer acquisition.

Final Take & Investment View

Despite another quarter of exceptional operational performance and a solid beat across metrics, the market reaction was cautious at best. The stock gained 3% intraday but dropped 4.3% after hours following the earnings release.

So... what’s the issue?

The simplest answer: Palantir is just too expensive right now.

At a market cap nearing $500 billion, the company is trading at over 100x expected 2025 revenue (around $4.5 billion). Its P/E ratio? A sky-high 640x. Even if Palantir can sustain 50%+ annual growth for the next several years, the current price bakes in extremely aggressive expectations. Any hiccup in growth could trigger a steep correction—classic “priced for perfection” dynamics.

More broadly, the long-term TAM (Total Addressable Market) assumptions still seem overstretched. Bulls currently peg Palantir’s TAM at $1 trillion—nearly 10x the $120 billion figure the company itself cited in its IPO filing. Even CEO Alex Karp’s own projection of 10x growth over five years seems hard to square with this ultra-bullish TAM sizing.

Moreover, some of Palantir’s existing strengths may eventually become liabilities:

- Its deep U.S. military ties, while helpful in winning federal defense contracts (e.g., the recent $1B U.S. Army deal), may limit adoption in geopolitically sensitive regions. European governments have growing concerns over data privacy, sovereignty, and national security—potentially capping the company’s international upside.

- While AIP supports modular reuse across clients, meaningful deployment still requires significant customization. Palantir often dispatches on-premise engineers to co-develop foundational structures with clients. This limits scalability and keeps customer acquisition costs high.

In short, four key risks remain on the table:

Risk 1: Unsupported TAM Projections

Management’s hike from $120B (IPO era) to $1T in claimed TAM appears disconnected from internal targets and actual traction. Government exposure remains crucial (e.g. 53% YoY growth in U.S. federal business Q2), but overseas expansion faces geopolitical and compliance headwinds.

Risk 2: Customization Bottlenecks

Despite modularity in AIP’s product suite, client setups still demand significant engineering resources. This hands-on engagement (e.g. deployment teams onsite) restrains economies of scale and keeps marginal costs stubbornly high.

Risk 3: Geopolitical Sensitivity

The firm’s reputation as a core military tech vendor may play against it as it pushes into more data-sensitive international markets. This could limit Palantir’s TAM ceiling in the public sector across NATO and the EU.

Risk 4: Valuation at Breaking Point

At a forward P/E ratio greater than 600x and a price/sales ratio north of 100x, Palantir is priced well beyond peers (e.g. Nvidia’s P/S ~45x). Sustained 50%+ revenue growth multiple years in a row is a tall order — and any miss could result in a painful de-rating.

Recommended Articles