Inflation Jitters and a Firmer Job Market Push U.S. Yields Toward 4.2%

Tradingkey - Geopolitical uncertainty—particularly the escalating standoff with Iran—has kept investors uneasy. Early in the week, that tension stirred a flight to safety, pushing demand for U.S. Treasuries higher and yields briefly lower. But as markets digested developments and risk appetite began to recover, the trend reversed, and yields quickly climbed back toward the year’s highs.

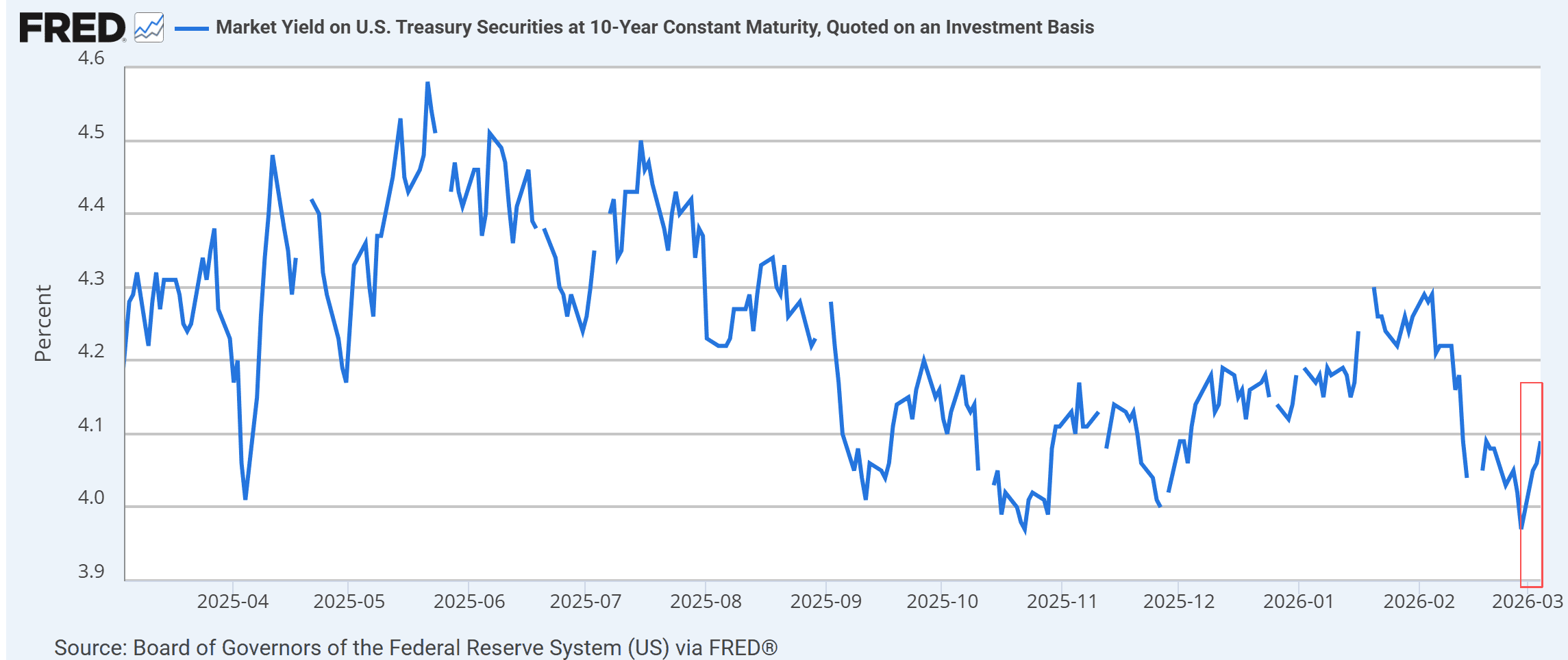

By midweek, the 10‑year Treasury yield had surged about 20 basis points, rising from roughly 3.94% on March 3 to an intraday peak around 4.13%–4.14%, its highest level in three weeks. The 30‑year long bond edged up to near 4.75%, while the 2‑year yield held close to 3.54%. The yield curve, once deeply inverted, has flattened noticeably—a signal that investors no longer see an imminent recession but expect inflation to stay stubbornly above the Federal Reserve’s 2 percent target.

Behind this move, the resurgence of inflation worries is unmistakable. Since mid‑December, crude oil prices have jumped close to 40 percent, reviving fears that higher energy and manufacturing costs will feed through to consumer prices. Higher yields reflect lower bond prices as investors demand greater compensation for the twin risks of persistent inflation and uncertainty about growth. The market’s message is straightforward: price pressures may last longer than many had assumed.

Wednesday brought fresh confirmation when the ADP employment report showed U.S. private‑sector payrolls rising faster than economists expected in February. The resilience of hiring reinforced the view that the economy remains too strong to justify early interest‑rate cuts. Traders dialed back expectations for Federal Reserve easing, and yields responded in kind.

Friday’s non‑farm payrolls data now loom as the next hinge point. Forecasts center on an increase of roughly 59,000 to 60,000 jobs and an unemployment rate of 4.3 percent. A strong report would likely postpone the Fed’s first rate reduction, while a weak one could reignite recession fears. Fed officials, including Minneapolis President Neel Kashkari, have repeated that monetary policy remains “data‑dependent,” underscoring that this jobs print could define the tone for the March FOMC meeting.

For the Trump administration, rising yields are no longer an abstract metric—they are a fiscal challenge. With the 10‑year hovering near 4.1 percent, the government’s annual interest burden on $38.6 trillion in federal debt has climbed to roughly $1.2 trillion. Such levels are politically and financially uncomfortable, feeding speculation that officials may seek unconventional ways to ease pressure. Some market watchers suggest Washington could try to lift gold prices—drawing safe‑haven demand away from Treasuries, just as the Fed’s asset purchases did in 2020—to ease bond‑market strain. Others believe the White House might slow its military escalation in the Middle East to curb the rise in oil prices and prevent another inflationary shock that would push yields even higher.

For now, the bond market is walking a narrow line. Inflation expectations remain sticky, payroll data continue to beat forecasts, and geopolitical risk isn’t fading. The result is a Treasury market increasingly shaped by tension—from Tehran to Washington—as investors weigh the cost of security, growth, and the stubborn arithmetic of higher rates.

Recommended Articles