Fed Chair Candidate: What Would a Hassett Nomination Mean for U.S. Stocks?

- US-Iran Rift Persists, Will Gold Rise or Fall Next?

- Gold rallies on hopes for US-Iran talks and falling US Treasury yields

- Gold Price Forecast: XAU/USD opens lower around $4,450 on fears of widening Iran conflicts

- USD/JPY Hits 160.00 Mark, Will Japanese Government Intervene? Will the Currency’s Rally Be Contained?

- Seesaw Effect Continues. US Pre-Market Three Major Index Futures Weaken, Oil Prices Rise, Bitcoin Drops Below 68,000 Mark

- Brent: Forecast lifted with $150 risk – Societe Generale

1. Introduction

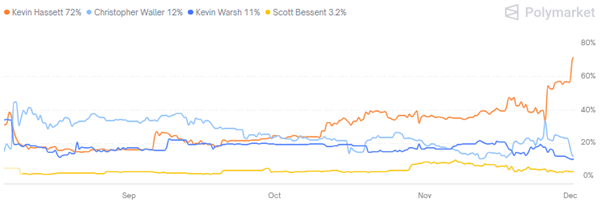

Over the past month, investors' expectations for a Federal Reserve interest rate cut in December first cooled and then reignited. These fluctuating expectations have directly triggered significant volatility in U.S. stocks recently. Looking ahead, alongside the sustainability of the AI theme and the severity of the U.S. stock market bubble, the trajectory of the Fed's monetary policy remains a key variable—and the direction of monetary policy formulation cannot be separated from the issue of who will be the next chairman of the Federal Reserve, especially amid lingering rumours that current Chair Jerome Powell may step down early. Currently, Kevin Hassett, Christopher Waller, and Kevin Warsh are the top contenders for the next Fed Chair nomination. According to betting data from Polymarket, Hassett's nomination probability has surged to 72%, a dramatic jump from 16% in early September. Meanwhile, current Fed Governor Christopher Waller holds a 12% chance, and former Fed Governor Kevin Warsh stands at 11% (Figure 1).

That said, some economists may hold differing views. From a traditional economic perspective, the Federal Reserve bears two core mandates: maintaining price stability and achieving full employment. Based on the Phillips Curve theory, inflation and unemployment exhibit an inverse relationship: during economic booms, falling unemployment tends to be accompanied by rising inflation, prompting the Fed to raise interest rates to curb excessive price hikes; conversely, in economic downturns, inflationary pressures ease but unemployment rises, and the Fed will then cut interest rates to stimulate labour market recovery. Given that both of the Fed’s mandates are guided by economic data in policy-making, traditional economists argue that the selection of the next Federal Reserve Chair will not have a substantive impact on the direction of monetary policy.

However, we disagree with traditional economists’ perspective — we believe the selection of the next Federal Reserve Chair is also one of the core factors determining the direction of its monetary policy. This view is based primarily on two key reasons: First, the Fed’s monetary policy decisions are guided not only by released historical data but also by forecasts of future data trends. In this forecasting process, the Fed Chair’s views and policy leanings (hawkish or dovish) will play a pivotal role. Second, while the Phillips Curve is highly effective in normal market conditions, it faces a policy dilemma in stagflation periods, where rising inflation coincides with slowing economic growth. In such cases, the Chair’s stance — whether to adopt a hawkish approach to prioritise inflation suppression or a dovish strategy to focus on stabilising employment — will become the core variable shaping the direction of monetary policy.

Given the significance of selecting the next Federal Reserve Chair, this analysis will proceed in three parts, following the logic: outlining top contenders — forecasting trends in Fed monetary policy — and analysing transmission effects on the U.S. stock market. Our research indicates that if Kevin Hassett — the front-runner with a nomination probability exceeding 70% — is successfully appointed, or if the dovish-leaning Christopher Waller wins the role, U.S. stocks are expected to continue hitting record highs, supported by a significantly accommodative monetary policy environment of interest rate cuts. Only if hawkish candidate Kevin Warsh — whose nomination probability stands at just 10% — emerges victorious, the pace of rate cuts may slow, thereby amplifying downward pressures on U.S. stocks.

Figure 1: Nomination Probability of Next Fed Chair

Source: Polymarket, TradingKey

2. Kevin Hassett

Kevin Hassett, the current Director of the National Economic Council, is the top potential candidate for the next Federal Reserve Chair. His recent remarks have not only revealed a pro-growth policy stance but also reflected a focus on preserving the Federal Reserve's independence. As a key confidant of Donald Trump, Hassett recently stated publicly that if appointed Fed Chair, he would "cut interest rates immediately," citing that "the data shows we should do so."

Hassett's resume shows he served as Chairman of the White House Council of Economic Advisers during Trump's first term. He returned to the White House in April 2020 amid the COVID-19 pandemic, taking on the role of Senior Adviser to President Trump. Now serving as Director of the National Economic Council, his core strengths as a candidate for Federal Reserve Chair lie in his profound economics expertise and the strong alignment between his historical policy stances and the Trump administration's ideological framework. Following the Federal Reserve's interest rate cut in September this year, he told CNBC in an interview: "This is a solid first step toward the goal of substantial rate cuts, and it’s exactly the right direction."

Furthermore, Hassett notes that the U.S. economy is in a supply-side driven expansion cycle — with growth momentum stemming from the production side rather than consumption stimulus. This dynamic implies that amid the current backdrop of aggregate supply outpacing aggregate demand, boosting domestic demand through interest rate cuts can both drive further economic growth and avoid significantly stoking inflationary pressures. Based on this, he supports continuing to pursue rate cuts on the premise that inflation remains manageable, thereby reducing financing costs for businesses and households. Hassett has been a vocal critic of Powell’s relatively conservative monetary policy, publicly calling for cumulative interest rate cuts of 1 to 1.5 percentage points over the next year and suggesting that single-rate cuts could exceed 25 basis points — a stance that aligns closely with Trump’s rate-cutting advocacy.

If Hassett secures the role of the next Federal Reserve Chair and fulfils his commitments, the Fed’s benchmark interest rate is expected to fall within the 2.5%-3% range in a year. Economists have not reached a consensus on the starting point of the current rate-cutting cycle: one school of thought argues that the cuts began in September this year, which would put the cumulative reduction at 150-200 basis points; the other contends that the current cycle started in September last year, with the September 2025 cut marking a resumption after a pause — under this definition, the cumulative easing would reach 250-300 basis points. Regardless of the statistical benchmark adopted, however, the magnitude of this preventive rate-cutting cycle significantly exceeds the 75-basis-point level of three typical preventive easing cycles in history (Figure 2).

From a historical perspective, during preventive rate cut cycles, the liquidity unleashed by accommodative policies has typically outweighed the negative impacts of economic slowdown, thereby propelling the U.S. stock market higher. Therefore, if Hassett is successfully elected, against the backdrop of the current resilient economy, aggressive preventive rate cuts will continue to provide upward momentum for U.S. equities. We project that the U.S. stock market will repeatedly hit new all-time highs over the next 12 months.

Figure 2: Fed Preventive Rate Cut Cycles (%)

Source: Refinitiv, TradingKey

3. Christopher Waller and Kevin Warsh

In addition to Hassett, both Christopher Waller and Kevin Warsh boast a nomination probability exceeding 10%. As a current Federal Reserve Governor, Waller stands as a highly competitive candidate, buoyed by his dovish monetary policy stance and extensive tenure within the Fed system. His recent remarks have maintained a cautiously dovish tone, as he explicitly stated: "We should implement interest rate cuts, but in a prudent manner—25 basis points at a time—while closely monitoring economic feedback." In fact, Waller's dovish leanings first emerged during the July 2025 FOMC meeting.

Kevin Warsh, the third-ranked candidate for the Federal Reserve, is a former Fed Governor and Fellow at the Hoover Institution. Widely regarded as a hawk on monetary policy, Warsh has long voiced concerns about inflation in the post-financial crisis era, opposing the Fed’s quantitative easing (QE) programs because monetary tightening should be initiated early to mitigate inflationary risks. For instance, in 2009, he warned that upside risks to inflation outweighed downside risks and expressed reservations during the 2010 debate over QE2. While reports in 2025 indicated his support for interest rate cuts—potentially influenced by political considerations—his core stance remains critical of excessive government spending and money creation as drivers of inflation.

4. Conclusion

In summary, the direction of the Federal Reserve's monetary policy stands as one of the core determinants of the U.S. stock market's future performance, and this policy trajectory is largely contingent on the appointment of the next Federal Reserve Chair. According to betting data from Polymarket, dovish candidate Kevin Hassett currently holds a 72% probability of being nominated, while the moderately dovish Christopher Waller stands at 12% and the hawkish Kevin Warsh at 11%. This implies that the likelihood of a dovish representative becoming the next Fed Chairman has exceeded 80%. Given the resilience of the U.S. economy, coupled with expectations of accommodative monetary policy (backed by over an 80% probability), we maintain a bullish stance on the U.S. stock market over the next 12 months.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.