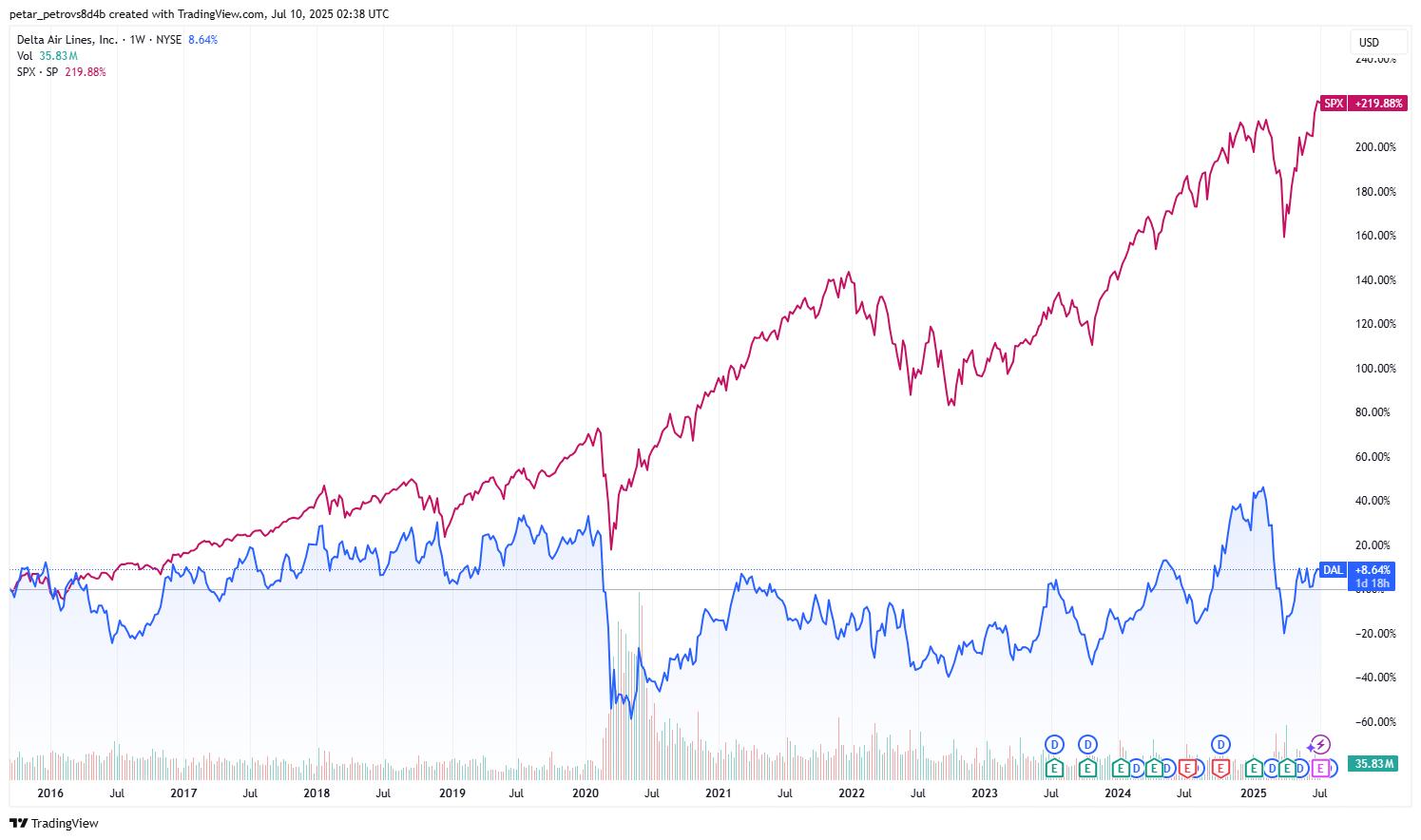

Delta Air Lines (DAL): No Turbulence Ahead

Share Price (USD) | 50.52 | 2024 Revenue (USD) | 61.64bn |

Market Cap (USD) | 32.99bn | 2024 EPS (USD) | 5.33 |

Listings | NYSE | Dividend Yield | 1.20% |

52-wk high/low (USD) | 69.98-34.74 | Target Price (USD) | 80.00 |

Source: TradingView

Investment Thesis

TradingKey - Delta Air Lines has been long underperforming the broad market, but we believe this should change. The market is yet to price in the resilient spending of the premium travelers, and the ability of DAL to increase their shareholder returns in the form of dividends and buybacks.

Company Background

Delta Air Lines is one of the largest and oldest airlines in the United States, headquartered in Atlanta, Georgia. With its massive fleet of over 900 aircraft, Delta serves nearly 300 destinations across more than 50 countries.

Revenue Breakdown

Surprisingly (or not), the revenue of DAL comes almost entirely from ticket sales, loyalty travel awards and all related services coming with air travelling. Additionally, DAL operates a refinery business so it can partially hedge against the fluctuations of the fuel costs.

70% of the revenue comes domestically, but the rest is from overseas flights, be it in Latin America or across the Pacific and the Atlantic.

Market Share and Competition

The airline industry in the US is still the largest by revenue compared to any other country, but also rather fragmented. The market share among players is quite evenly spread with Delta being the market share leader by revenue with a small advantage – 17.6%, closely followed by American Airlines, Southwest and United. These four players control nearly 70% of the total market share by revenue.

Delta along with United and American are considered full-service airlines, while Southwest is more on the budget-airline side. Full-service airlines have more pricy tickets but that includes checked baggage, meals, drinks, and they also provide business and first class. Budget airlines like Southwest do not provide such services (or if they do, they will be for an additional cost).

.jpg)

Source: Bureau of Transportation Statistics

Growth Potential

We believe Delta is well positioned for the coming months due to the following factors:

Premium Exposure: Nearly 60% of the revenue comes from premium and loyalty services, more than any other US carrier. In fact, revenue from premium services has been growing faster in the last two quarters (high single digits vs low single digits for economy) most probably because higher-income travelers’ spending is more resilient during economic softening. Not only this, but the margin for premium services is also higher. Additionally, the newly-passed Big Beautiful Bill will spur further consumption.

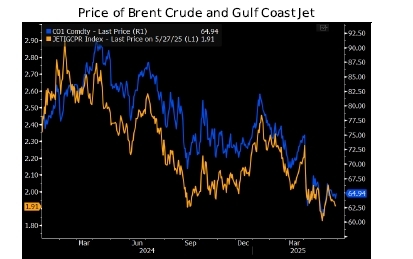

Suppressed Oil Prices: Jet fuel is a major expense item, representing 20% of DAL’s revenue, and it is also very correlated with crude oil prices. As the oil prices seem rather suppressed, this can be a tailwind for the margin and can also allow DAL to cut ticket prices and expand revenue further. Also, after the end of the tensions between Israel and Iran, the black gold prices would continue the downward direction.

Source: Bloomberg Intelligence

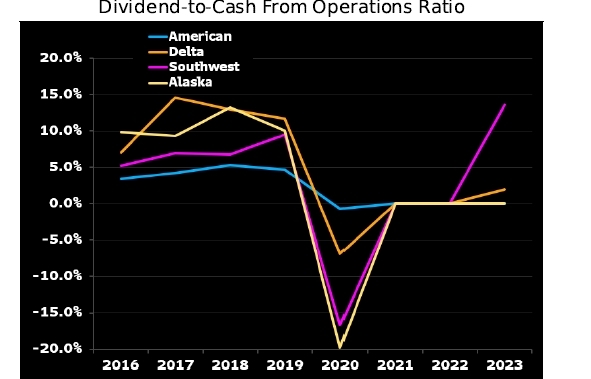

Increase in Shareholder Return: There is a lot of runaway for DAL to increase shareholder return and dividends in particular. Dividend payment is still way below pre-Covid levels.

Source: Bloomberg Intelligence

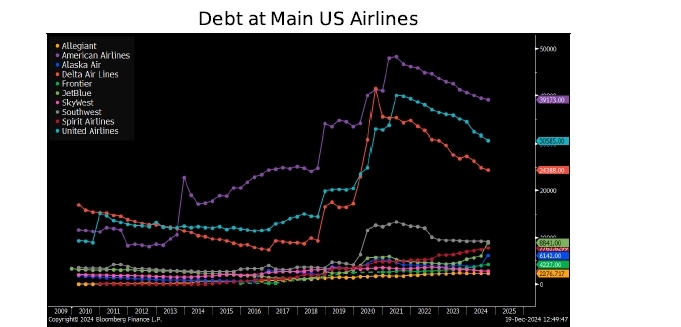

Delta and the other full-service carriers are confidently reducing the debt they have accumulated during the Covid era, which was the main reason why there were no dividends in 2021 and 2022. However, once they reach their desired leverage targets, they will ramp up the money on shareholder returns.

Source: Bloomberg Intelligence

Valuation

Our DCF model shows that the target price for Delta is USD80.00, far ahead of the current one of USD50.00. In addition, the PE ratio of DAL is relatively attractive at 9x – much lower than Southwest Airlines (28x) and American Airlines (15x), but slightly higher than United Airlines (7x).

Risks

We believe the competition risk in the face of Southwest Airlines (LUV) will be a long-term risk, as the company is making good efforts to move away from the budget airline image and become the fourth full-service career.

Another significant downside risk is the geopolitical tensions that can trigger a spike in the oil price which will affect the fuel costs and the profitability of DAL.

Get Started

Recommended Articles