Walgreens: Discount or Deadweight?

- Q3 2025 retail pharmacy revenue rose 7.8% to $30.7 billion, but front-end sales declined 5.3% year-over-year.

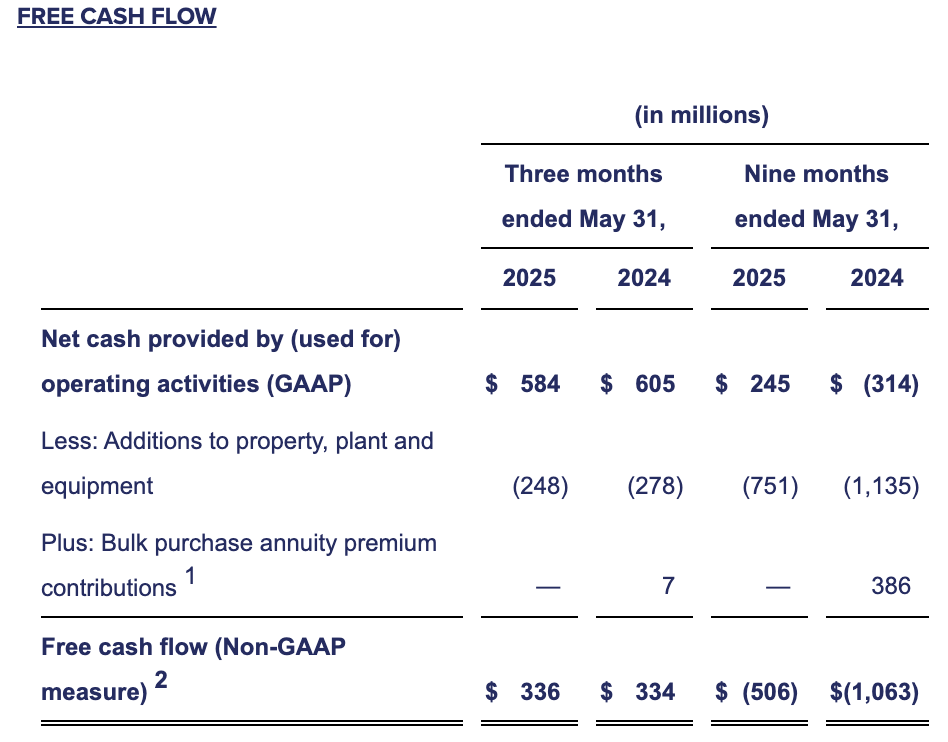

- Operating cash flow for nine months was only $245 million, with free cash flow at negative $506 million.

- Valuation remains depressed with a forward P/E of 6.8x and EV/Sales of 0.26x, far below peer averages.

- U.S. Healthcare turned adjusted profitable with $54 million in income, yet still posted a $64 million operating loss.

In an era when pharmacy retail is evolving at rocket speed from a narrow-based retail model into a broad-based healthcare ecosystem, Walgreens Boots Alliance (WBA) finds itself on a treacherous fork in the road: wholesale market expectations are cataclysmically misinterpreting its resilient value proposition core franchisee, or this severely discounted multiple is an illusion covering underlying structural decay.

With a forward P/E non-GAAP multiple of just 6.80x, some 59% off its peer group median, investors can say the retailer goes on and on and on with a rare margin of safety characteristic throughout the industry. And yet its third-quarter 2025 figures and gargantuan spread between its headline earnings and free-cash-flow measures stand as reminders of the harsh realities of speculating in a once-iconic pharmacy chain beset by front-end sales decline, legal risks, and a strategic transition plan cost overruns and risk of execution still too great.

Threatened by a potential Sycamore Partners buyout, there looms large the question of whether such underperformance is cyclical and fixable or a structural sign that the economic moat for the business model of the retail pharmacy is decaying faster than its turnaround thesis can restore. This analysis dissects Walgreens' business units, competitive environment, financial profile, and latent cracks that prove potentially most crucial for contrarian stakeholders among its institutional owners.

Prescription Strength or Retail Decay? Evolving DNA of Walgreens’ Model

Walgreens Boots Alliance's business these days is a patchwork quilt of retail pharmacy, international wholesale, and burgeoning U.S. healthcare holdings assembled together with a strategy to build out the front-end consumer footprint as a vertically integrated care network.

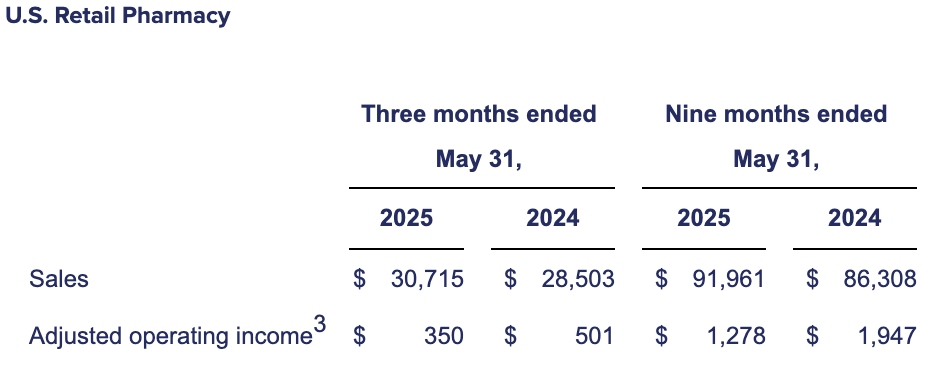

The Retail Pharmacy business still generates most sales, $30.7 billion for Q3 2025, up 7.8% year-over-year, mainly driven by pharmacy inflation and script volumes. Comparable pharmacy sales rose 14.6%, a reassuring sign that the script-filling machine is robust on an operational basis despite challenges faced by the business in retail. But retail sales declined 5.3%, and comparable front-end sales declined 2.4%, a reflection of secular decline from discretionary store-based buying as online and other non-store channels tap share.

Source: Walgreens Boots Alliance, FY2025 Q3 Results

International stores, led by Boots UK and Germany’s wholesale footprint, offer decent growth and diversification. The 18.7% leap in Boots.com’s online sales shows how the UK brand still punches above its weight in omnichannel retail. The Healthcare segment for the United States, the future once heralded by Walgreens, remains a mixed bag: Q3 sales dropped 1% year-over-year, but adjusted operating income swung back positive at $54 million from a loss last year due to gains from VillageMD and Shields. For all this good news, however, there is an underlying structural weakness: even after favorable trends from integration and impairment charges and costs, the segment still had an operating loss of $64 million.

Through ~12,500 stores across the globe and 312,000 workers, Walgreens is still an integral part of the community distribution chain for health, dispensing medicines and basic care, and enabling last-mile pharmaceutical distribution. But its historic footprint also confers operational leverage, growing cost pressures, lease obligations, and store-level ineffectiveness that make scale an uncertain advantage in a deflationary retail marketplace. The buildout of synergies between its retail pharmacy and healthcare services is theoretically robust but thus far incompletely capitalized, as Q3’s ongoing cost inflation and uncertain margin growth demonstrate.

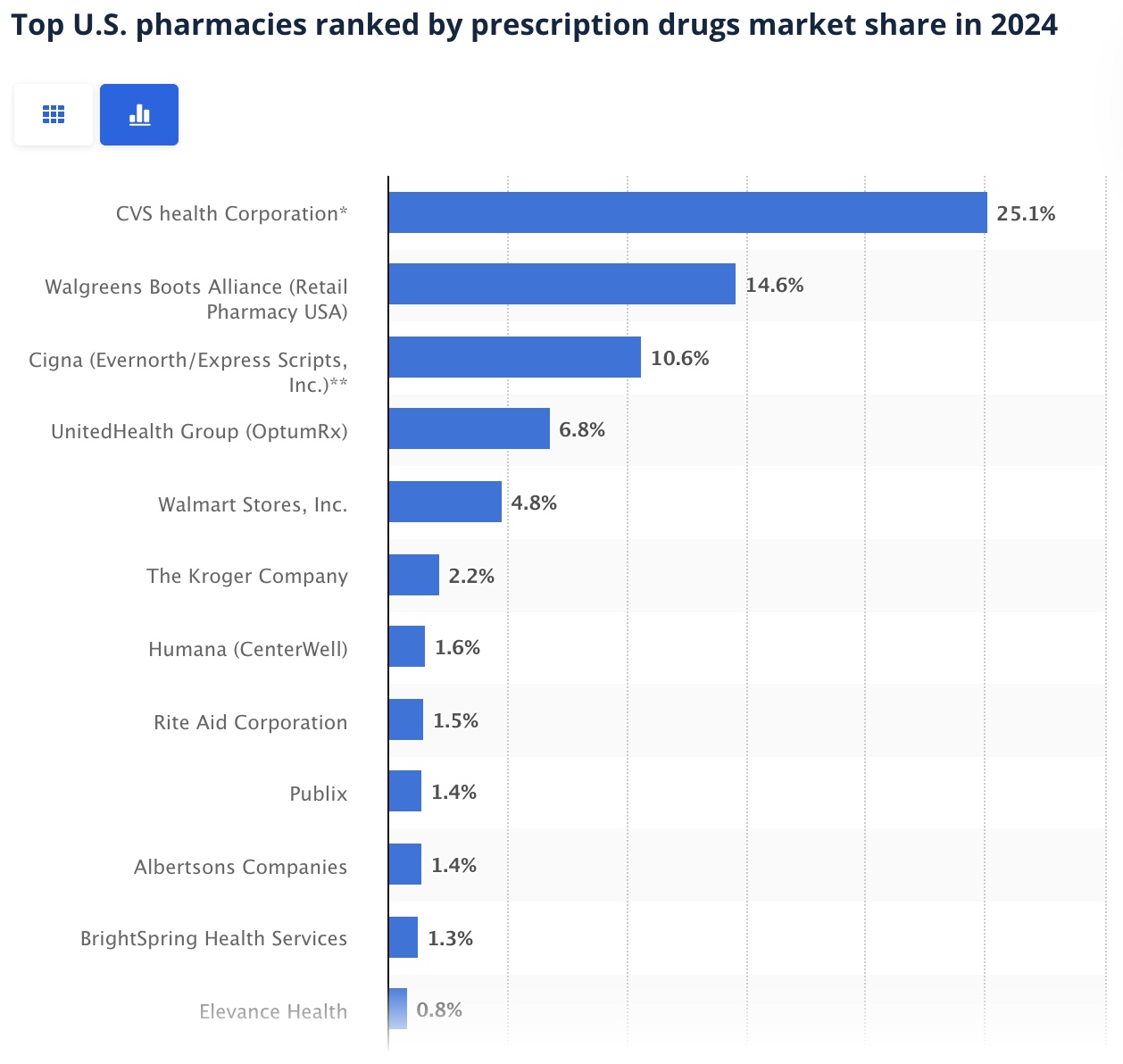

Under the Microscope: How Walgreens Performs in the Competitive Race

Alongside peers like CVS Health and boots-on-the-ground disruptors like Amazon’s PillPack, Walgreens' competitive positioning is exclusively constrained by its reliance on an aging front-end model and shallow vertical integration relative to peers with insurers on their own books or next-gen digital channels.

Source: Statista

CVS’s robust insurance float through Aetna enables customer stickiness and cross-subsidization unavailable to Walgreens. Instead, Walgreens must carve differentiation through alliance and bolt-on acquisitions, VillageMD, CareCentrix, and Shields among them, intended to craft a hybrid primary and specialty pharmacy layer that blurs the line between bricks-and-mortar and coordinated care.

Boots UK in Europe still enjoys brand equity but is also vulnerable to the same risk of retail erosion that is moderated in part by its deeper online penetration. This online silver lining is yet too narrow on its own to offset front-end business structure problems. Though Amazon’s invasion of home delivery for prescriptions is yet another deflationary factor of price competition, Walgreens' strategic response, moving toward embedded clinics and more upscale provision of care, hasn't scaled to a tipping point that would be worth heavy cost structure drag.

Big-box rivals like Target and Walmart also pose a significant competitive threat since their pharmacy store footprint has larger basket sizes across broader discretionary and essentials coverage. Walgreens' store footprint simplification strategy does indeed rationalize underperforming sites but leaves its revenue impact mixed and its cost reduction thus far unsuccessful in creating worthwhile operating leverage.

Unraveling the Numbers: Forensic Accounting Insights on the Deep Value

The dramatic discount inherent in the valuation multiples is tempting at first sight. Walgreens' forward P/E of 6.80x is roughly 59% lower compared with its peer group median, and its EV/Sales multiple stands at just 0.26x compared with a peer group median of 1.57x. This valuation discount is accounted for largely by ongoing GAAP losses and humongous goodwill write-downs, a year-to-date $5.8 billion charge substantially related to VillageMD and U.S. Retail Pharmacy. The Q3 net loss of $175 million on a GAAP basis vs. $334 million on an adjusted basis serves to show just how non-cash write-downs and historical legal fees distort headline numbers.

.jpg)

Source: Walgreens Boots Alliance, FY2025 Q3 Results

But the safety net vanishes once you apply the same lens to cash generation. Operating cash flow for nine months was a paltry $245 million, just sufficient to cover dividend payouts, and free cash flow still remains a negative $506 million, better than last year's worse burn.

Source: Walgreens Boots Alliance, FY2025 Q3 Results

EV/EBITDA multiple as a rough proxy for enterprise value relative to core earnings power is 12.96x on a trailing basis, within 7.5% of the sector median. Such a premium reflects that investors unwittingly impute the legal settlements, opioid liabilities, and store closure expenses as real money leaks, and they are. If U.S. Healthcare turns to fulfill promises of margin accretion and patient monetization, payback can be attractive. But right now, the sustainability of these changes is fragile due to lingering legal and integration liabilities that keep bleeding money.

By comparison with Walgreens’s ~1.42x P/B multiple, below industry median but just above its five-year range, the market signals no tangible hidden book value that can cushion a downturn. Jamming together non-core holdings and scarred goodwill stacks makes dubious an argument about breakup valuation, unleashing hidden value without attendant large write-offs.

Risk and Reward: M&A Gambit and Turnaround Execution

The Sycamore Partners transaction looms as a going-private trigger. While a going-private transaction can provide financial headroom to initiate an aggressive restructuring from public market pressures, there are also leverage growth risks, asset sales at unfavorable prices, and governance changes that can emphasize shorter-term cash generation over longer-term integration on the trajectory for healthcare. Additionally, retraction of explicit guidance in anticipation of the upcoming transaction also serves to highlight just how poor visibility there is on Walgreens’ turnaround schedule and cash flows.

The legal environment remains the primary overhang. Over $1.4 billion in year-to-date legal expenses, composed largely of opioid settlements, continues to eat through operating cash flows while dwarfing working capital accretion and interest expenses. Already-elevated leverage would be jeopardized further if there is any miscue around the cost-cutting script or any further impairment fees.

Conclusion

Walgreens Boots Alliance offers textbook deep-value optics on paper but remains a capital trap until its faster scaling of its U.S. Healthcare pivot and litigation drain come down materially. For portfolio managers, the asymmetric setup is dependent on the private equity exit strategy and whether Sycamore's balance sheet discipline can hold through the operating turnaround without further value degradation.

If the buyout proceeds as planned, patient investors can be rewarded with moderate gains from cost eliminations and store simplification. However, there are several execution risks, integration costs, and legal uncertainties that make this quite a risky restructuring thesis and not simply a value restoration. Buy with clear eyes: perhaps the market is correct about writing off Walgreens for good.

Copyleaks Report: https://app.copyleaks.com/report/xnlm4hrc820fs3k6/preview?key=e6jlpxp0ie4feoqe&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

Recommended Articles