Tripadvisor (TRIP): An Undervalued Hidden Gem Riding the Experience Economy with AI

Investment Thesis

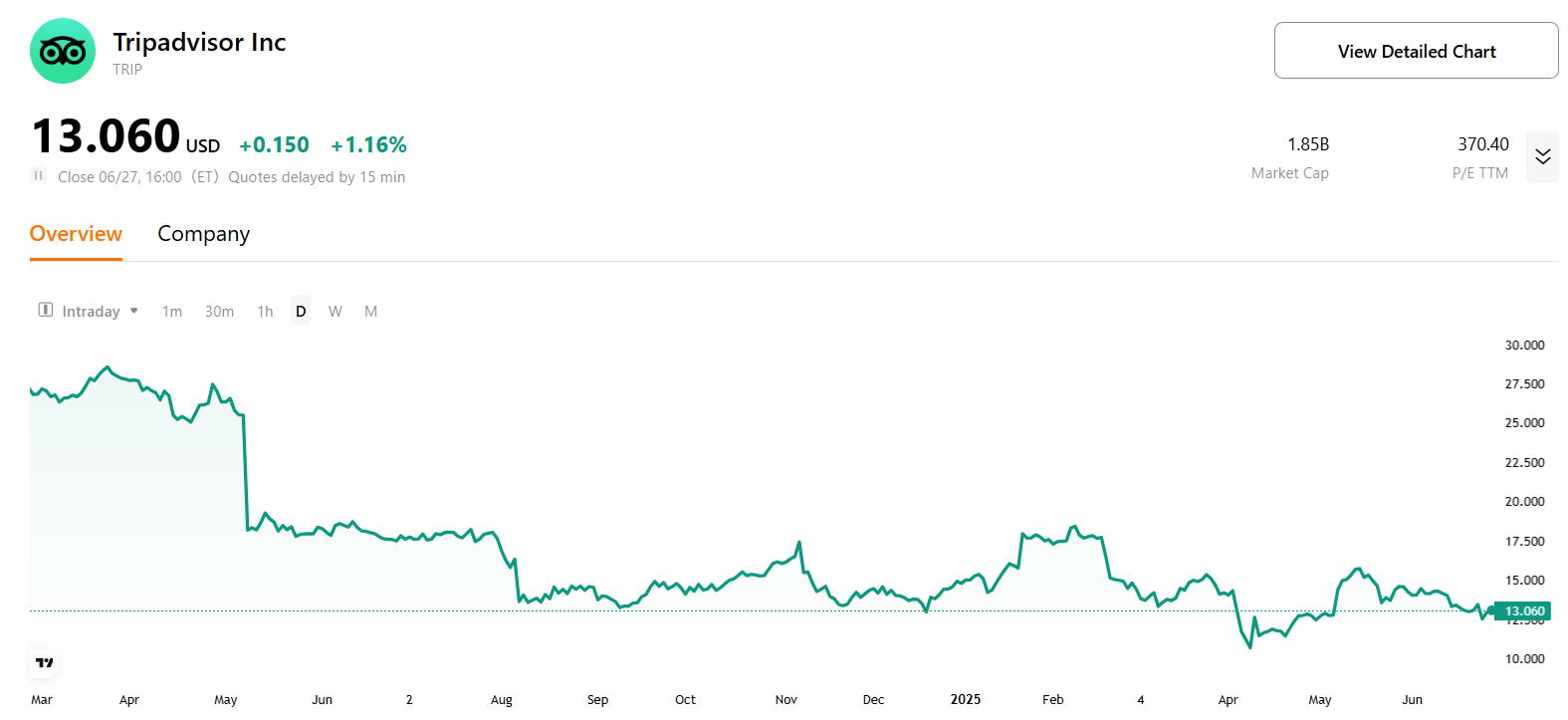

TradingKey - Tripadvisor, a leading global travel guidance platform, is shifting from an advertising-focused model to a transaction-based revenue model, showing strong growth potential. In Q1 2025, its Viator (experience bookings) and TheFork (restaurant bookings) segments grew revenue by 10% and 12%, respectively, reducing reliance on advertising. AI-powered tools, like trip planners and review summaries, boost user engagement and bookings, aligning with the trend toward unique travel experiences. Despite competition and economic risks, Tripadvisor’s stock, with a forward P/E of 8.7 (below the peer median of 15), looks attractive. Viator’s growth and AI-driven revenue potential is worth watch and support a target price range of $13–$22.

Source: TradingKey

Company Overview

Founded in 2000 by Stephen Kaufer to simplify trip planning, Tripadvisor is now the world’s largest travel guidance platform, with over 1 billion reviews covering 12.46 million businesses worldwide. It offers hotel and flight price comparisons (launched in 2013), experience bookings through Viator, and restaurant reservations via TheFork, providing travelers with clear, reliable information to make decisions.

Based in Needham, Massachusetts, Tripadvisor was acquired by IAC in 2004, merged with Expedia, and became an independent public company in 2011, trading on NASDAQ under TRIP. It operates in 43 countries, with over 100 million mobile app downloads driving user engagement. With 400 million monthly active users and a vast library of user-generated content (UGC), Tripadvisor stands out in travel tech. While traditionally known for its UGC and hotel ads, its Viator and TheFork platforms are now key drivers of revenue growth.

Business Model: Diverse and Evolving

Source: Tripadvisor

Tripadvisor is more than just a review website. It’s a comprehensive travel guidance platform. Its strength lies in its massive UGC library, with over 1 billion reviews of hotels, restaurants, attractions, and more. This depth and breadth provide trusted trip-planning information, building strong brand recognition and a loyal community.

Tripadvisor earns revenue from:

- Advertising: Hotels and travel providers pay for ads and listings on the core platform to reach its large audience.

- Commissions/Transaction Fees: The fastest-growing revenue source, driven by:

- Viator: An online marketplace for tours, activities, and experiences, earning commissions on bookings.

- TheFork : A restaurant booking platform, strong in Europe, charging fees for reservations.

- Other Revenue: Includes subscriptions and related services.

Tripadvisor’s shift to direct bookings mirrors the steady revenue models of SaaS companies, reducing dependence on volatile ad revenue. Its ability to cross-sell (e.g., suggesting Viator experiences to hotel bookers) boosts revenue stability.

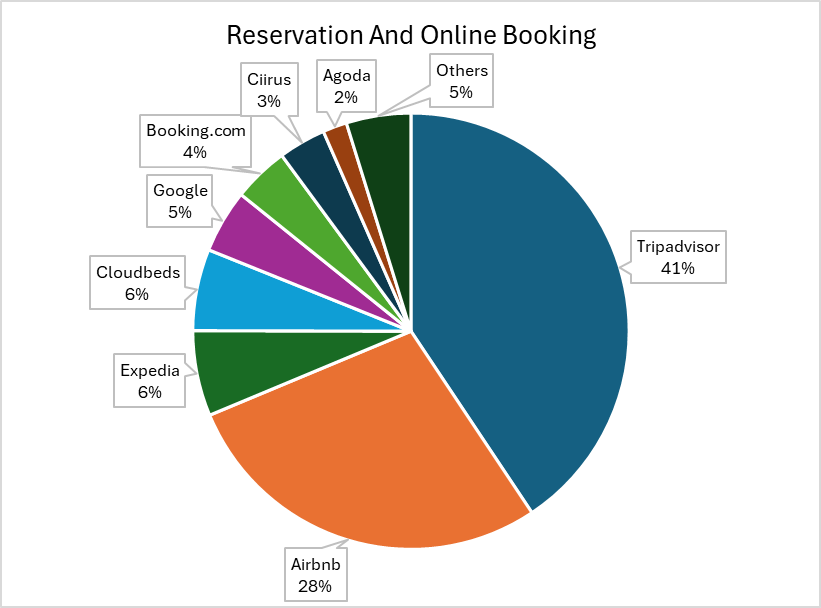

Competitive Advantage

Tripadvisor’s moat comes from its unmatched UGC scale, creating a network effect that competitors like Airbnb Experiences or Booking Holdings can’t easily replicate. Unlike rivals focused on low prices, Tripadvisor uses AI-driven ad optimization to deliver better returns for partners and higher satisfaction for users, strengthening its leadership in travel meta-search and experiences.

Source: 6sense

Main Competitors

- Online Travel Agencies (OTAs): Booking Holdings (Booking.com, Agoda, Kayak) and Expedia Group (Expedia, Hotels.com, Vrbo) dominate hotel and flight bookings with stronger direct booking capabilities.

- Search Engines: Google (Google Travel) integrates travel search and booking, posing a growing threat.

- Experience Platforms: Viator leads, but faces niche platforms and local operators. Airbnb also competes in experiences and alternative accommodations.

- Restaurant Booking Platforms: TheFork competes with local and global platforms like OpenTable.

The shift to online travel planning and booking supports Tripadvisor’s digital-first model. Growing demand for unique local experiences over traditional sightseeing fuels Viator’s rapid growth, positioning Tripadvisor well in this high-growth segment.

While often labeled an OTA, Tripadvisor’s unique strength is its content and guidance role. Its vast UGC and authentic reviews make it a trusted source for trip research and inspiration. Unlike Booking Holdings or Expedia, which focus on transactions and price competition, Tripadvisor prioritizes content quality and user engagement. This strategy avoids price wars, potentially leading to better margins and a more loyal user base.

AI Advancements

Tripadvisor is using AI to transform trip planning and boost revenue. Its three key initiatives are:

1. AI-Powered Summaries: Tripadvisor analyzes its 1 billion reviews to create short, AI-generated summaries of hotels and services, highlighting key themes. This helps users make faster, smarter decisions. The feature is rolling out in the U.S. and Canada, complementing traditional reviews.

2. AI Trip Planner: Built on OpenAI’s models, the “Trips” tool creates personalized itineraries based on user inputs (destination, dates, companions, interests). It recommends hotels, restaurants, and activities based on proximity and preferences. Users can save, edit, and share plans. It’s live in the U.S. via web and mobile, with plans for global expansion.

3. Perplexity Partnership: Since January 2025, Tripadvisor’s data licensing with Perplexity’s AI search engine brings high-intent traffic. Perplexity users seeking specific travel recommendations convert at higher rates than traditional search traffic, increasing bookings and cutting marketing costs. Tripadvisor’s CEO noted in the earnings call that AI-driven traffic delivers 3 times the conversion and revenue of regular users.

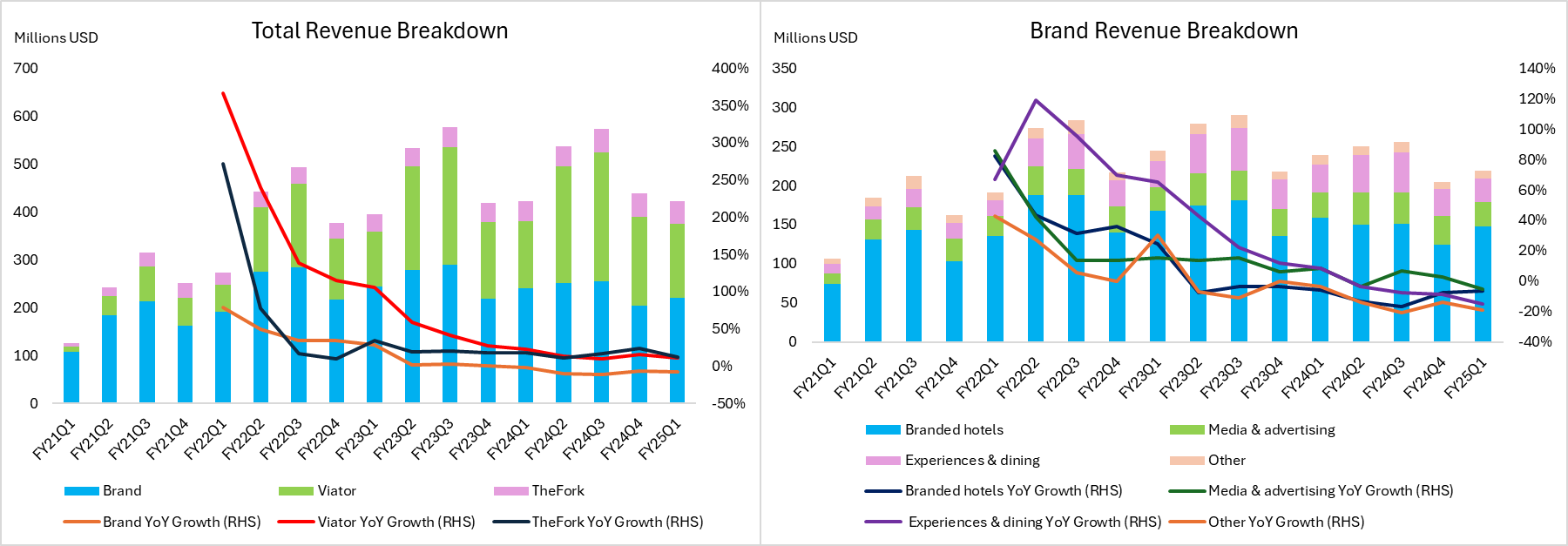

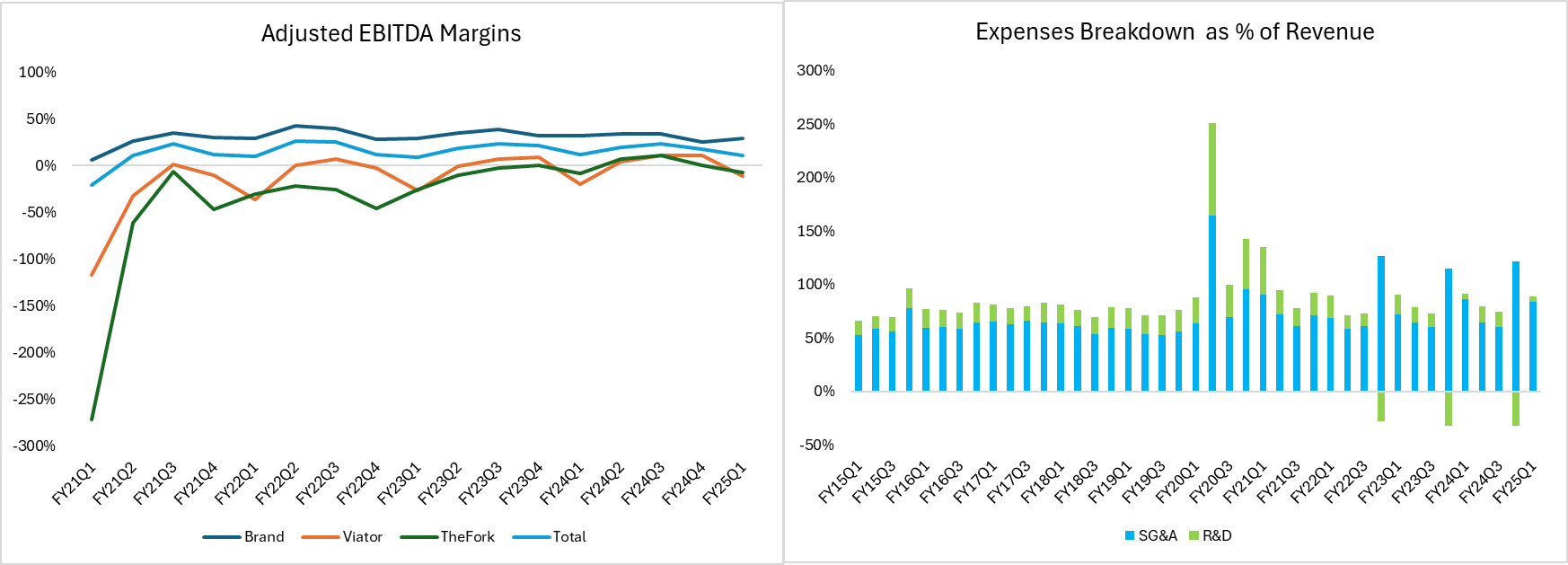

Financial Performance

Overall Results (Q1 2025)

- Revenue Growth: Total revenue reached $398 million, up 1% YoY.

- Profitability (Adjusted EBITDA): Adjusted EBITDA was $44 million, with an 11% margin. Viator’s revenue growth and TheFork’s high-growth software subscriptions (over 90% growth) improved profit structure.

- Net Income: Non-GAAP earnings per share (EPS) was $0.14, up 17%, beating market expectations.

Source: Tripadvisor Earnings Report, TradingKey

Segment Performance

- Viator: Revenue (39% of total) grew 10% to $156 million, with gross booking value (GBV) at $1.1 billion, also up 10%. Higher direct booking share supports long-term margin growth. Adjusted EBITDA loss narrowed to $18 million (11.3% loss rate) from 19.5% last year.

- TheFork: Revenue (12% of total) rose 12% to $46 million. Adjusted EBITDA loss was $4 million, short term loss of investments to capture Europe’s restaurant booking market.

- Brand Tripadvisor: Revenue (55% of total) fell 8% to $219 million but delivered $65 million in adjusted EBITDA (30% margin), beating expectations due to optimized hotel meta-search pricing and cost control. This segment has slowed growth but provides solid base revenue support.

Source: Tripadvisor Earnings Report, TradingKey

Tripadvisor’s focus on AI-driven high-intent traffic, direct booking expansion, and high-growth segments offsets short-term pressures in its core business. TheFork’s investments in product, market, and tech are expected to drive growth in H2 2025, further boosting group profitability.

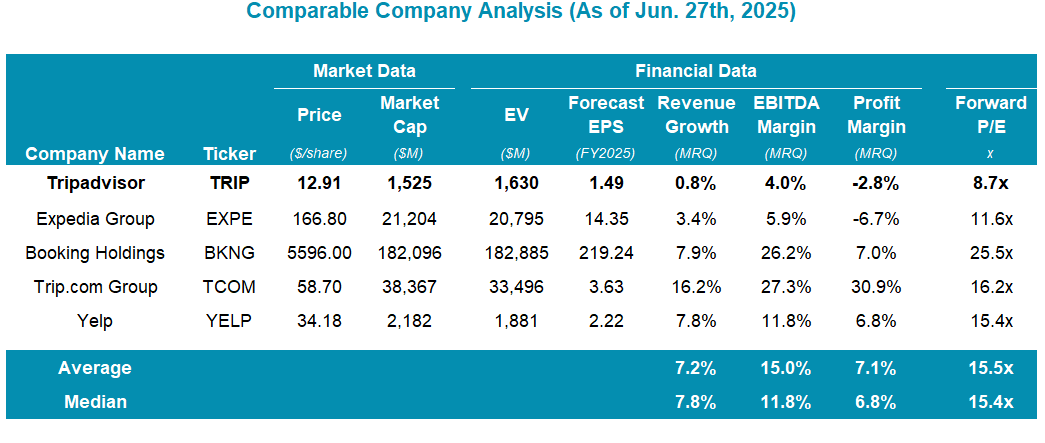

Valuation

Tripadvisor’s forward P/E of 8.7 is below the peer median of 15.4, reflecting its modest revenue growth (0.8%) and EBITDA margin (4.0%) compared to peer averages of 7.2% and 15.0%. Applying a P/E range of 8.7–15 to its 2025 EPS forecast of $1.49 gives a target price of $12.96–$22.35. The lower end accounts for margin and growth challenges, while the higher end reflects potential from stronger revenue growth, better Viator and TheFork margins, or successful AI monetization, which could lead the market to revalue the stock closer to peers.

Source: StockAnalysis, TradingKey

Risks and Challenges

Tripadvisor faces intense competition from Booking Holdings and others, which could squeeze market share and margins. Regulatory scrutiny of online reviews and advertising raises compliance costs and risks. Its reliance on ad revenue makes it vulnerable to economic downturns and shifts in digital ad spending. TheFork’s shift from third-party to self-managed sales may temporarily reduce revenue.

Get Started

Recommended Articles