From Chips to Limbs: The Humanoid Robot Industry in One Chart

TradingKey - At last month’s JPMorgan China Tech Summit, one of the biggest themes was the rapid progress in humanoid robotics — especially Tesla’s Optimus robot, which now has an accelerated mass production schedule. Morgan Stanley has previously outlined the key players in the humanoid robotics value chain.

In recent U.S.–China talks, rare earth export controls became a hot-button issue again. These raw materials — including neodymium and praseodymium — are essential for building high-performance motors and magnets inside humanoid robots. Elon Musk has warned that strict controls in China could slow down production of Optimus, and new forecasts from Wood Mackenzie don’t put investors at ease: if humanoid robots take off as expected, we could see a material shortage growing from just 1% to over 35% by 2037.

That’s why capital markets were quick to react. As soon as there was a signal of potential cooperation from the latest U.S.–China talks, rare earth and AI hardware stocks jumped sharply. With more robot-specific names expected to follow, investors should keep an eye on this sector.

The Global Robotics Map: West Leads R&D, Asia Owns the Hardware

There’s actually a clear split forming in the humanoid robotics supply chain.

Players like Tesla, NVIDIA, and ABB dominate in AI models, simulation capabilities, and high-end chips — areas where the U.S. and Europe generally lead. But if you're looking for the gears, batteries, and motors that actually bring robots to life, Asia is where they’re made: 73% of robot suppliers and 77% of integrators are based in Asia. China alone makes up 56%, thanks to strong policy support and fully integrated production ecosystems.

Some names to note here: CATL (batteries), Inovance (motors), and BYD (system integration). Japan stays strong in precision components like gear reducers, and Korea plays a major role in batteries and electronics.

Tesla’s Optimus Gears Up — but Faces Cheaper Chinese Rivals

Tesla’s Optimus robot has been a big headline-grabber, and it’s now moving from R&D to real use: the company is planning to deploy it in its own EV factories as early as 2025. The new Optimus Gen2 model is lighter (about 10kg less), more precise (thanks to planetary roller screws), and aims to cut costs to $20,000. That’s down significantly from the $50K–$60K range today.

But there's growing competition. Chinese company Unitree is already shipping humanoid robots starting at just $16,000 — nearly one-third cheaper than Tesla’s current version. Local media reports that Unitree robots are popping up inside factories owned by BYD and Geely.

Under the Hood: Sensors Getting Smaller, Smarter

Advanced sensors are the backbone of humanoid robots. These machines use dozens — even hundreds — of sensors to mimic human perception: they need to see, hear, feel, and balance like real people. There are two game-changing tech trends here:1) Miniaturization of precision force sensors; 2) More powerful, high-res vision sensors.

For example, Tesla’s Optimus Gen2 robot uses six-axis force sensors in its wrists and ankles. This helps it detect interaction forces with the environment in real time — allowing for safer, more autonomous movement. Companies like ATI are leading this area.

AI Is the Brain — and It’s Learning Fast

While the sensors are critical, the real leap comes from software. With the rise of multimodal AI models that can fuse language, vision, and motion — humanoid robots can now “understand” instructions in more human-like ways.

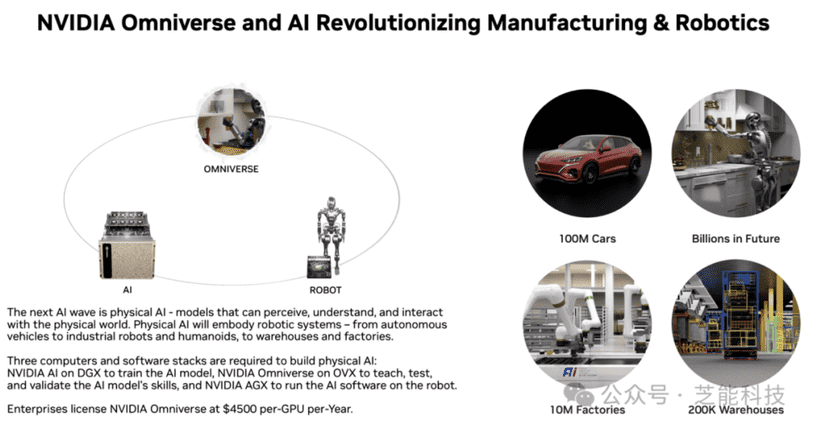

NVIDIA’s role can’t be overstated here. Its Omniverse platform, paired with the Project GR00T foundational model, creates simulated training environments that drastically reduce training time. As CEO Jensen Huang said in May, NVIDIA is positioning itself across the entire AI stack — from chips and simulations to industrial and autonomous robotics. “From training to deployment,” he said, “AI is ready to power the next-gen factory.”

Why Automakers Are Going All In

One of the more surprising trends? Global automakers are entering the humanoid robot race in full force.

Tesla kicked it off, but now Chinese giants like GAC, XPeng, and BYD, along with Toyota and Hyundai, are also ramping up efforts. Why? The reasoning is simple: growth in global vehicle sales is slowing (down to ~2.4% annually), and automakers are looking for “second growth curves.” Humanoid robots not only offer a new product market, but can also help reduce factory labor costs.

Also, there’s a natural fit: many of the core technologies — batteries, motors, drive systems — overlap with what automakers already do. So it’s not really a stretch for them to enter this space. In fact, they may have a leg up on startups.

Meanwhile, Samsung has emerged as a unique player — it’s the only major name involved in all three layers of the robotics value chain: the “brain,” “body,” and end-to-end integration. The firm recently upped its stake in Korea's Rainbow Robotics to 35%, signaling a longer-term bet on humanoid automation. Rainbow Robotics, in case you missed it, built South Korea’s first humanoid robot, Hubo.

The Robotics Investment Landscape: Key Players to Watch

The Brain (Semis + Software)

- AI foundations: NVIDIA (Project GR00T), Google (DeepMind), Microsoft, Meta

- Simulation & digital twin: NVIDIA Omniverse, Dassault Systèmes

- Data platforms: Palantir

- Semiconductors: NVIDIA, Intel, Qualcomm (compute); Ambarella, Mobileye (vision); Samsung, Micron (memory); ARM & TSMC (design + foundry)

The Body (Actuators + Sensors + Energy)

- Motors: Nidec, Inovance

- Gearboxes: Harmonic Drive, NIDEC

- Bearings & screws: Schaeffler, NSK, Hiwin

- Sensors: Sony, Keyence (vision); Novanta, Keli (force); Robosense, Aptiv (lidar/RADAR)

- Batteries: CATL, LG Energy Solution

- Materials: lightweight frames (e.g., Xusheng aluminum castings)

The Integrators (Complete Robot Systems)

- Tesla (Optimus), Toyota (T-HR3), Hyundai (via Boston Dynamics)

- Chinese OEMs: BYD (“Yao Shun Yu”), GAC, XPeng

- Consumer tech: Xiaomi (CyberOne), Apple (rumored)

Recommended Articles