Nike Stock Analysis: Can Nike Still Be Invested In? 2026 Nike Stock Price Investment Outlook and Risk

TradingKey - We believe that in the short term, NIKE's stock price has reached technical support levels. Coupled with CEO Tim Cook's increased stake, which has boosted market confidence, we foresee certain upside potential for NIKE's stock price in the short term.

From a long-term perspective, given that NIKE Inc.'s fundamentals are still constrained by the Greater China market and competition from other international brands, with no significant improvement yet evident. We believe that for value investors, although NIKE's stock price has fallen significantly from its peak, it is not advisable to open large positions. We recommend that investors consider dollar-cost averaging and initiating a foundational position in NIKE's stock price to ensure the widest possible margin of safety.

NIKE Inc. Background and Introduction

In 1964, an American sports enthusiast, Philip Hampson Knight, approached his friend, William Jay Bowerman, and told him that he had acquired the U.S. distribution rights for Tiger shoes from Onitsuka Co., Ltd. He proposed forming a company together, and this brand, which began with distribution, was NIKE's predecessor — Blue Ribbon Sports .

NIKE, Inc. designs, markets, and distributes athletic footwear, apparel, equipment, accessories, and related services. The company's operations are divided into four segments: North America, Europe, Middle East & Africa (EMEA), Greater China, and Asia Pacific & Latin America (APLA). The company sells a range of equipment and accessories under the NIKE brand, including bags, socks, sports balls, eyewear, timepieces, digital devices, bats, gloves, protective gear, and other sports equipment.

Furthermore, the company also designs products specifically for the Jordan Brand and Converse brand. The Jordan Brand primarily focuses on basketball performance and culture, designing, distributing, and licensing athletic and casual footwear, apparel, and accessories featuring the Jumpman trademark. The company also designs, distributes, and licenses casual athletic footwear, apparel, and accessories under the Chuck Taylor, All Star, One Star, Star Chevron and Jack Purcell trademarks.

How Has NIKE's Stock Price Performed?

[NKE Stock Price Trend, Source: TradingView]

NIKE was undoubtedly a favored asset for most investors before 2021. Its vast consumer market share, serving as a 'moat,' consistently drove steady stock price appreciation, and its continuously growing dividends were a core attraction for many investors.

Year | Market Cap | Change |

2025 | $88.69 B | -22.03% |

2024 | $113.75 B | -31.16% |

2023 | $165.23 B | -9.74% |

2022 | $183.07 B | -30.54% |

2021 | $263.55 B | 18.17% |

2020 | $223.02 B | 41.21% |

2019 | $157.94 B | 35.09% |

2018 | $116.91 B | 15.1% |

2017 | $101.58 B | 20.68% |

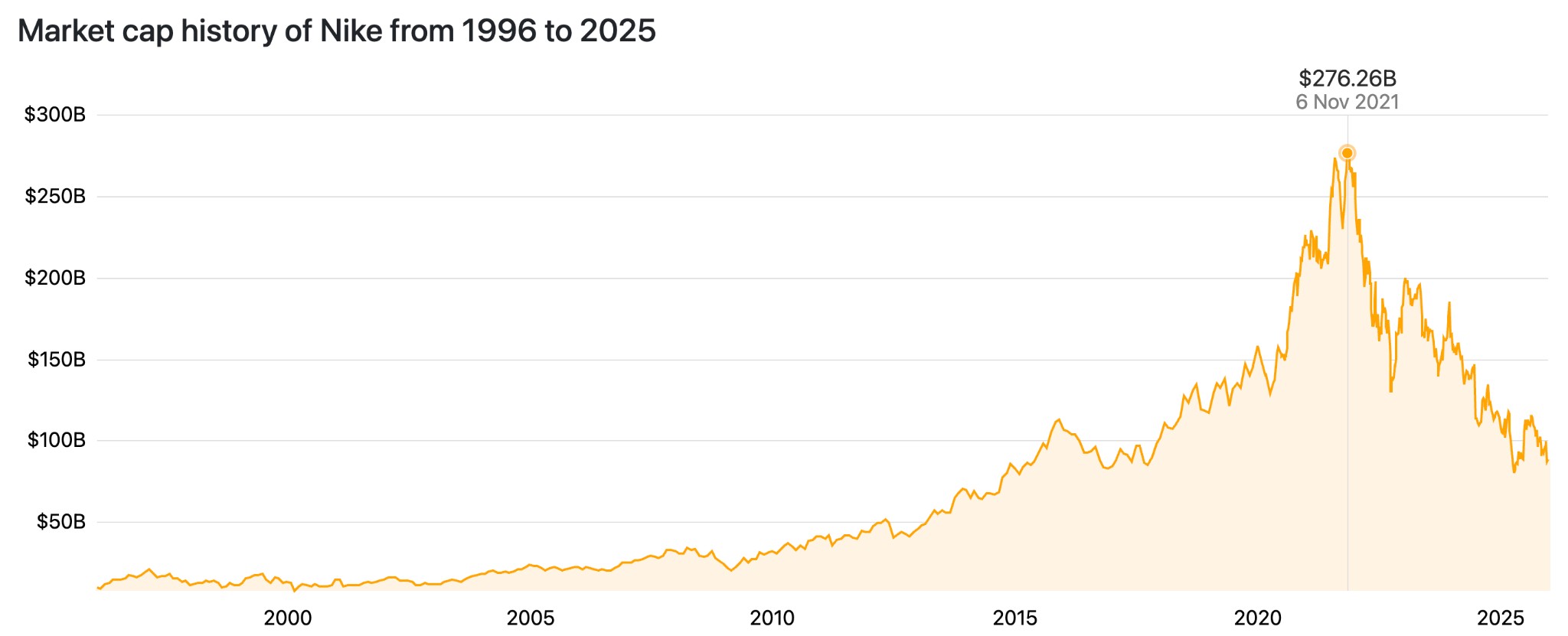

However, after 2021, this buoyant trend rapidly reversed. NIKE's stock price began a continuous decline from 2021, with a maximum drop of nearly 70%, and its market capitalization plummeted from almost $280 billion to $80 billion.

Why Has NIKE's Stock Price Declined?

Since reaching its historical peak in the second half of 2021, NIKE's stock price has continuously fallen, accumulating a decline of over 65% by the end of December 2025, with its market capitalization shrinking from a peak of approximately $281 billion to about $90 billion.

[NIKE Market Capitalization Overview, Source: Companiesmarketcap]

NIKE's fiscal Q2 2026 revenue was $12.43 billion, marking an approximate 1% year-over-year increase, but net income declined by 32%, and earnings per share (EPS) were only $0.53. The gross margin decreased by 300 basis points to 40.6%, and the operating margin was merely 7.4%, which directly triggered a single-day stock price drop of over 10%.

This decline was not driven by a single event but rather by a combination of factors, including erosion of profitability, strategic execution deviations, market regional slowdowns, innovation lag, and external geopolitical pressures.

I. Profitability and Gross Margin Compression

In 2021, affected by pandemic lockdowns in Vietnam and Indonesia, NIKE lost over 10 weeks of production capacity (Vietnam accounts for approximately 50% of its footwear production), leading to global product shortages.

Subsequently, the company significantly increased orders, which, coupled with slowing demand, resulted in a surge in inventory: by the end of 2022, inventory was up 44% year-over-year, peaking at over $9 billion in fiscal year 2023.

To clear the pandemic-era over-ordering induced inventory backlog, NIKE Inc. continuously implemented large-scale promotions and discounts in the North American market. While this maintained sales volumes, it severely damaged the brand's premium positioning and unit profitability .

Concurrently, in 2025, affected by the Trump administration's tariff policies, NIKE's import costs significantly increased. The company anticipates an additional $1.5 billion in tariff-related expenses for fiscal year 2026, further compressing gross margins.

II. Greater China Slowdown: Fastest Engine Becomes Biggest Drag

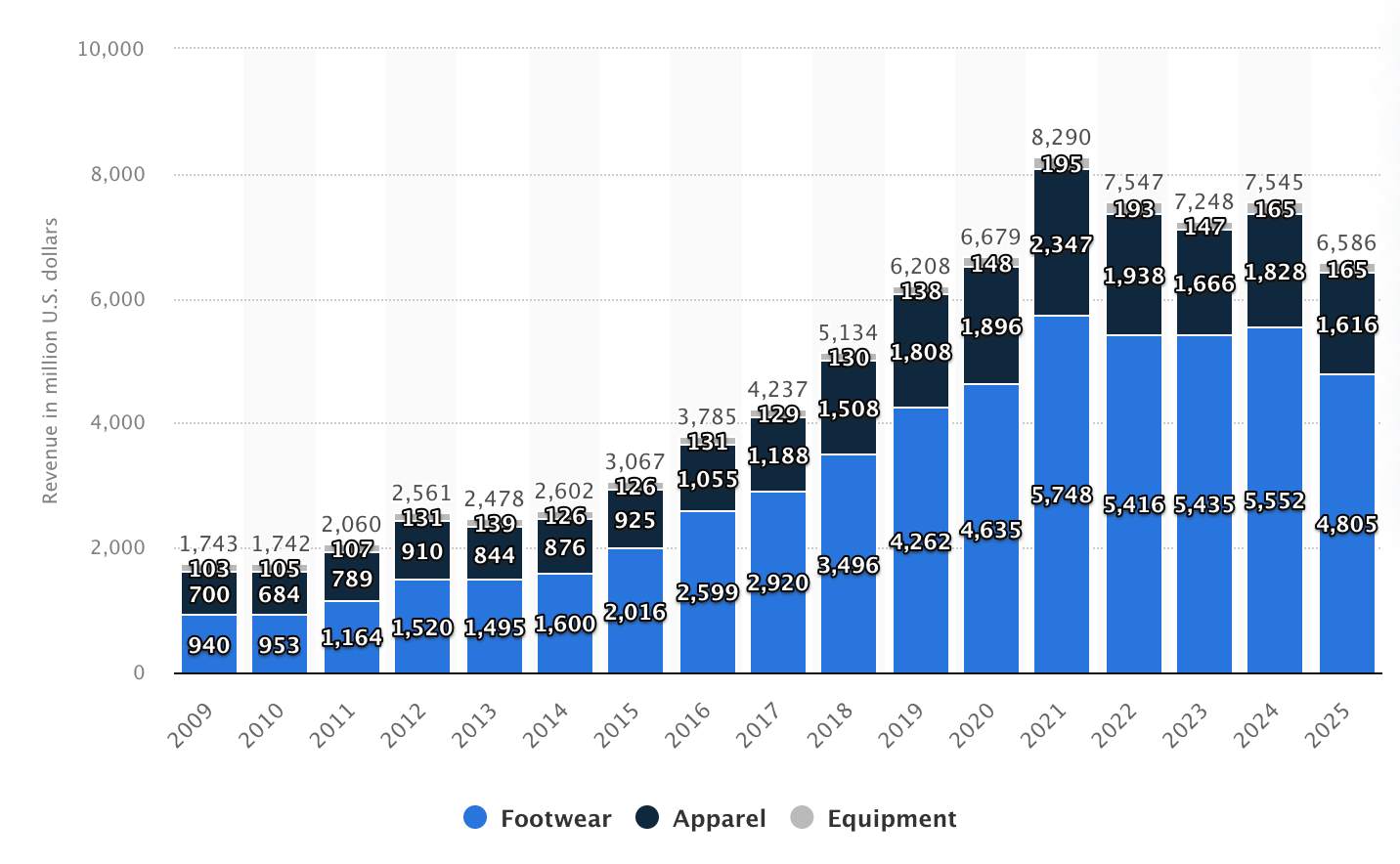

Revenue in Greater China has declined for six consecutive quarters, dropping 17% in the second quarter, making it the largest drag on NIKE's growth.

[NIKE Q2 FY2026 Earnings Report, Source: NIKE investors ]

Consumer spending in the region has become more rational, shifting towards supporting local brands (such as Anta and Li-Ning). These domestic brands have eroded NIKE's brand premium and popularity through cultural resonance and localized marketing. For instance, renowned marathon runner Suguru Osako, after his contract with NIKE expired, publicly changed his Japan Athletics Federation registration to 'Tokyo Li-Ning' on October 17.

Concurrently, NIKE's digital transformation has lagged, failing to adequately integrate into social e-commerce ecosystems like Douyin and Xiaohongshu. Its overreliance on the traditional Direct-to-Consumer (DTC) model has resulted in a slow response to market changes.

[NIKE Inc.'s Revenue in Greater China from Fiscal Year 2009 to 2025, Source: Statista]

GRI News points out that this contrasts with competitors' rapid adaptation, amplifying structural challenges. Forbes also noted that slowing sales in China are one of the key concerns for NIKE's stock price decline.

III. DTC Strategy Miscalculation Leads to Channel Imbalance

Former CEO John Donahoe's 'Consumer Direct Acceleration' strategy excessively pushed for a higher DTC share, significantly reducing orders from wholesale partners (such as Foot Locker). While this temporarily boosted per-unit profit and data control, it led to high logistics, return, and customer acquisition costs, and reduced consumer access in physical multi-brand stores, with emerging brands filling the channel gaps.

Following the launch of the 'Win Now' strategy by new CEO Elliott Hill, the company began to correct course, with wholesale revenue growing by 8% in the second quarter, showing initial signs of recovery. However, rebuilding distribution relationships will require higher marketing expenditures and time.

IV. Innovation Exhaustion and Encroaching New Competition

NIKE has long relied on classic series like Air Jordan, Dunk, and Air Force 1, but it lacks groundbreaking new technologies or eye-catching new products, leading to accusations of 'losing its soul.'

Younger consumers are experiencing aesthetic fatigue and turning to brands like Hoka and On Running. These brands have rapidly eroded market share in core categories like running, leveraging their thick-soled cushioning technology and performance-fashion crossover appeal.

GRI News emphasizes that this is a core manifestation of NIKE's 'innovation exhaustion,' leading to continuous market share loss.

Is NIKE Stock Worth Investing in in 2026?

Although NIKE (NKE.US) stock price has cumulatively fallen over 60% from its 2021 peak, we believe that with the gradual implementation of the 'Win Now' strategy by new CEO Elliott Hill, 2026 could mark a turning point for the company's recovery.

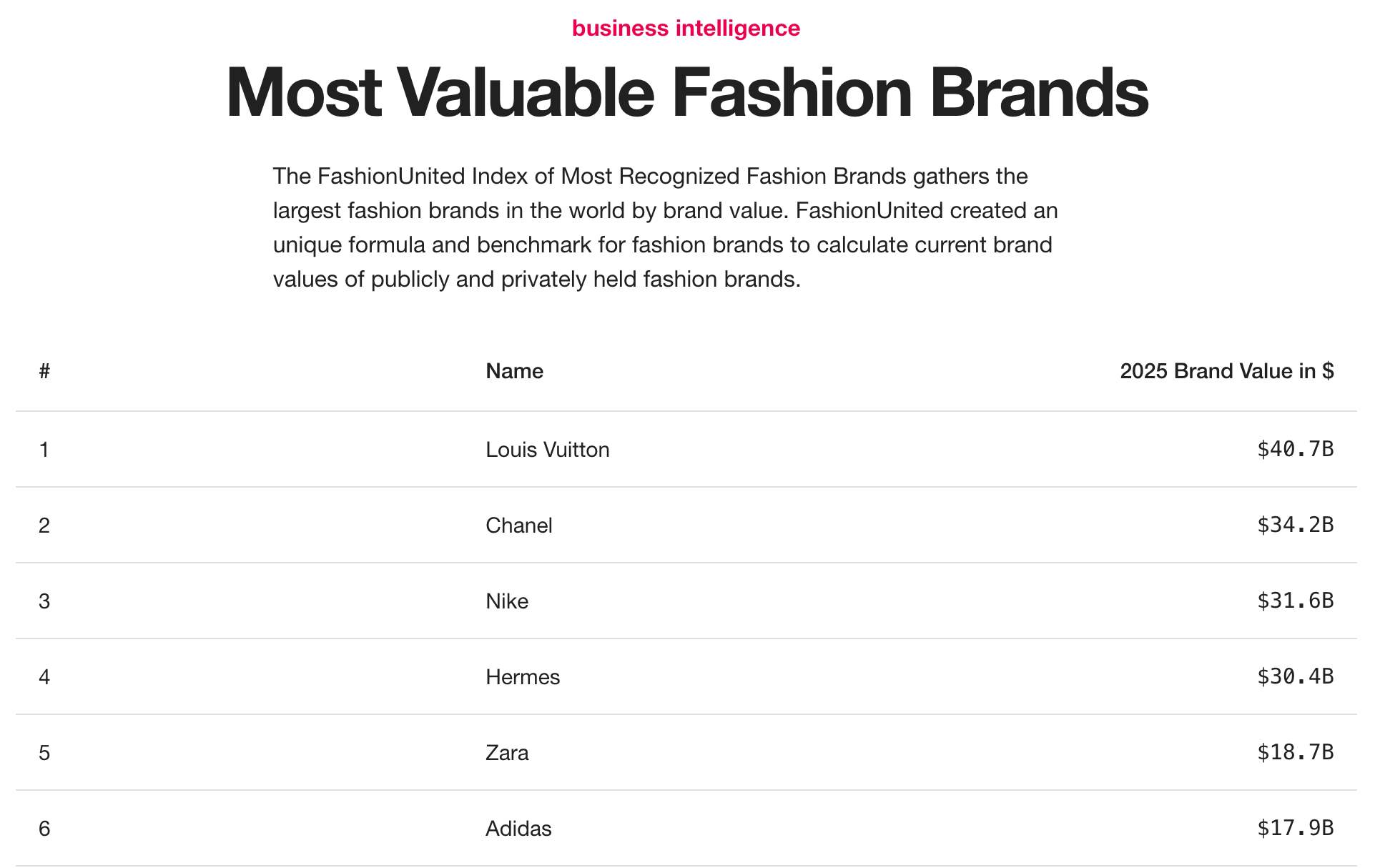

I. Strong NIKE Brand Moat

As a global sportswear giant, NIKE's international brand recognition inherently provides it with a certain premium. The company, relying on classic series like Air Jordan and top athlete endorsements, maintained its brand value among the industry's leaders in 2025, with Statista data showing its global brand value at approximately $31.6 billion.

[Global Brand Value 2025, Source: Fashionunited]

Despite the continuous decline from 2021 to 2025, NIKE Inc.'s current P/E ratio is in a relatively overvalued range. This stems from its brand premium, but historically, when its stock price falls into an undervalued P/E range, it often presents a favorable entry opportunity.

[NIKE Inc. Valuation Overview, Source: TradingKey]

Apple CEO Tim Cook recently increased his stake by nearly $3 million in NIKE stock, raising his holdings to 105,000 shares, which is also seen as a positive signal of confidence in management.

II. 'Win Now' Strategy Showing Results

The 'Win Now' strategy focuses on returning to sports roots, repairing wholesale channels, and accelerating innovation. North American wholesale business grew by 8% in fiscal year 2026 Q2.

['NIKE Mind'; Source: NIKE Official Website]

The 'NIKE Mind' platform, set to launch in January 2026, will introduce neuroscience-based footwear technology, aiming to revitalize the running category and compete against emerging brands like Hoka and On Running.

Management anticipates that through product portfolio optimization and cost control, revenue for fiscal year 2026 is expected to achieve low single-digit growth, with EPS potentially rising to $2.49-$3.00.

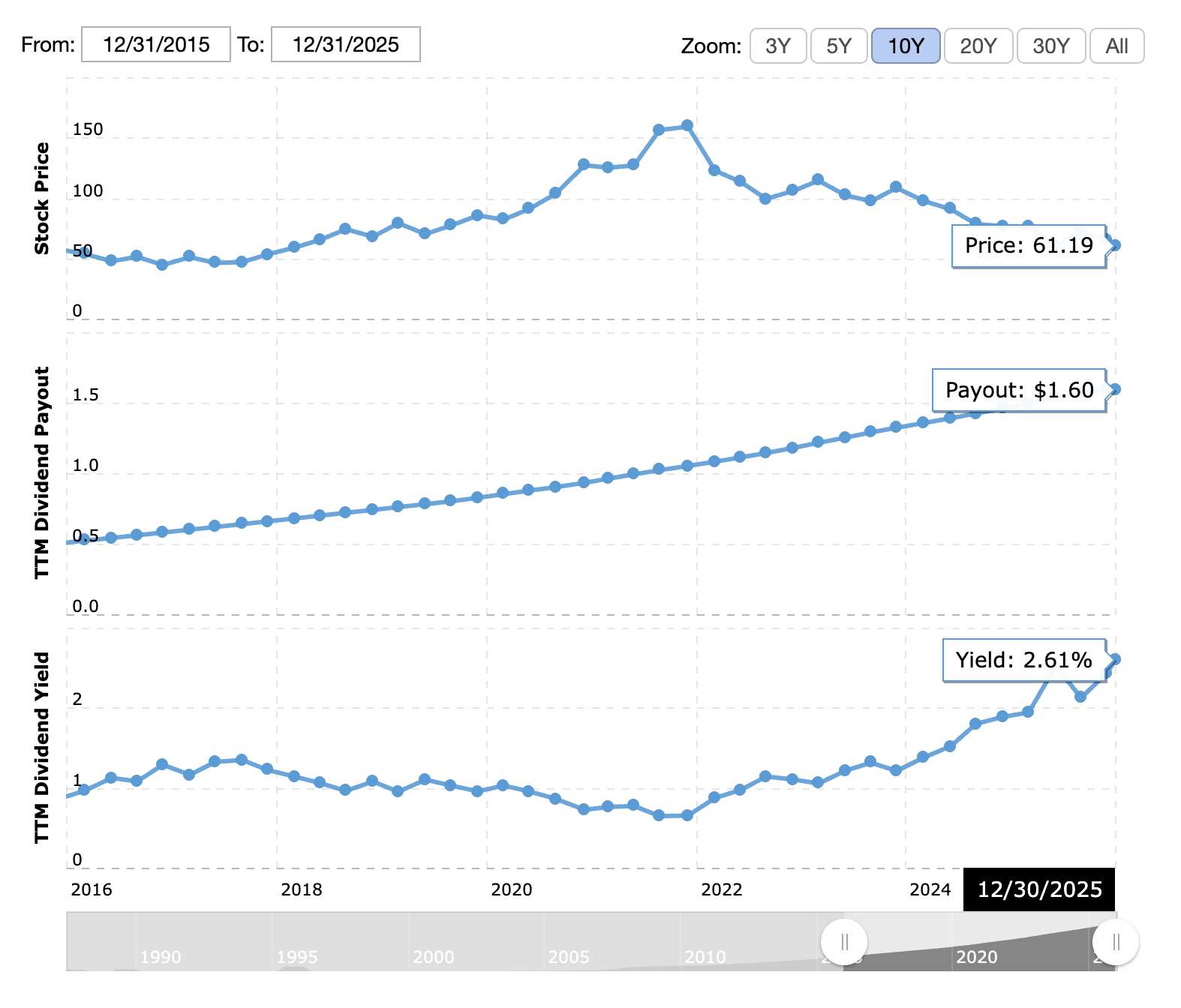

III. Dividend Appeal Provides Buffer for Long-Term Investors

NIKE's current dividend yield is approximately 2.6%. As a 'value stock' with consecutive years of dividend payouts, its continuously positive dividend feedback has alleviated some investor concerns stemming from the stock price decline.

Although tariff pressures are expected to result in an additional $1.5 billion in costs for 2026, the company has reduced inventory to $7.7 billion through inventory clearance and supply chain optimization. The gross margin is expected to gradually recover to over 42%.

[NIKE Dividend Overview, Source: Macrotrends]

Overall, NIKE is suitable for value-oriented investors to build positions at current lows, but close monitoring of quarterly earnings reports is necessary to confirm the recovery trajectory. Should the macroeconomic environment deteriorate, stock price volatility may intensify.

NIKE Future Stock Price Outlook and Investment Recommendation

We believe that in the short term, NIKE's stock price has reached technical support levels. Coupled with CEO Tim Cook's increased stake, which has boosted market confidence, we foresee certain upside potential for NIKE's stock price in the short term.

From a long-term perspective, given that NIKE Inc.'s fundamentals are still constrained by the Greater China market and competition from other international brands, with no significant improvement yet evident. We believe that for value investors, although NIKE's stock price has fallen significantly from its peak, it is not advisable to open large positions. We recommend that investors consider dollar-cost averaging and initiating a foundational position in NIKE's stock price to ensure the widest possible margin of safety.

[NIKE Stock Price Chart, Source: TradingView]

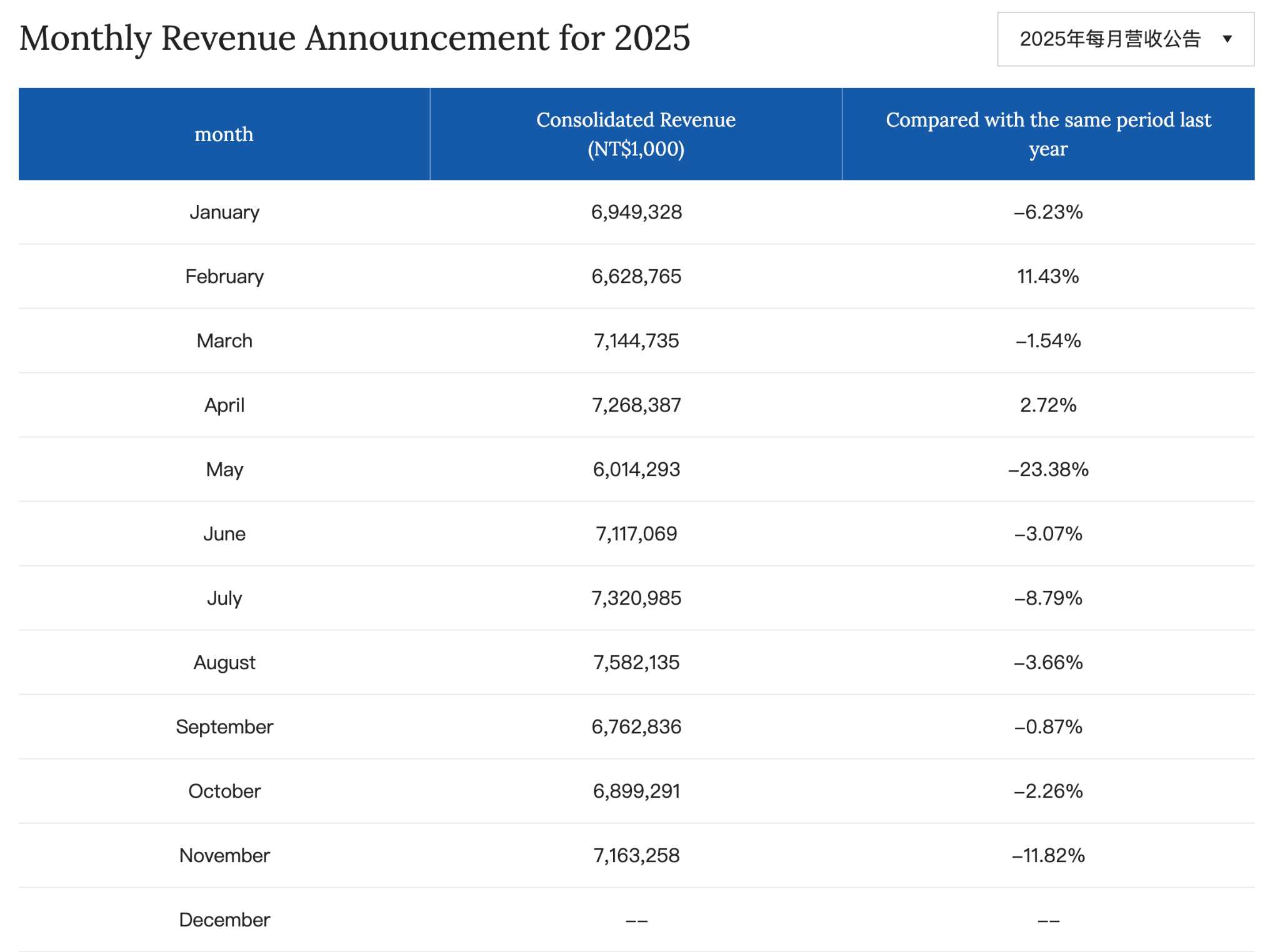

Additionally, we can also forecast NIKE's revenue by observing the earnings performance of its deeply partnered manufacturers to make stock price and financial reports forecasts.

NIKE's manufacturing partner, Feng Tay ( 9910.TW ), with the vast majority of its orders coming from NIKE. Unlike other manufacturers, Taiwanese manufacturers are required to disclose reports monthly.

[Feng Tay Monthly Revenue Announcement 2025, Source: fengtay]

Therefore, leveraging such information asymmetry can help us ascertain changes in NIKE's demand earlier, thereby predicting its revenue performance and enabling us to make more confident investment decisions.

Recommended Articles