Meta’s AI Play Deepens with $2 Billion Acquisition of China’s Manus — But Can It Deliver?

TradingKey - After DeepSeek captured global attention early this year, the spotlight on frontier AI has shifted back toward China again—but this time with a twist.

According to a Wall Street Journal report, Meta is acquiring Chinese startup Manus for over $2 billion.

This marks Meta’s second-largest deal of the year and follows its earlier acquisition of Scale AI in the first half of 2025.

Why Manus?

In March, Manus drew widespread attention for unveiling an AI model capable of generating detailed research reports and building complex websites.

That demo came just weeks after the release of DeepSeek, the Chinese AI foundation model that stunned Silicon Valley with its performance and compute efficiency. Since its launch this spring, Manus has focused on building general-purpose AI agents. The company has reportedly served millions of users, processed more than 147 trillion tokens, and created over 80 million virtual computing environments.

In April, its parent company, Butterfly Effect, raised $75 million in a Series B led by Benchmark Capital, with Tencent, ZhenFund, and HSG also participating.

Prior to the Meta deal, Butterfly Effect was reportedly in the middle of a funding round that valued it at $2 billion. Meta now says it intends to keep Manus operational and continue selling its services, with plans to integrate the technology into Meta’s existing suite of social platforms.

For Manus, the acquisition further solidifies its ambition to lead at the AI application layer.

The Big Picture Behind Meta’s AI Spending Spree

Meta’s earlier purchase, Scale AI, raised eyebrows as well.

Scale’s core business lies in high-quality data labeling and model evaluation technology. It has quietly become an indispensable partner to nearly every major AI company in the U.S., including Google and OpenAI. For LLMs to train and improve, clean, well-labeled data is critical. Scale AI excels here—combining automation with human-in-the-loop workflows to handle everything from text and images to video and 3D sensor input.

At first glance, the two deals seem unrelated. Scale builds data foundations. Manus builds agents and apps on top of existing foundation models. But taken together, they reflect Meta’s potential long-term strategy: a bet on building an AI-native ecosystem that spans social platforms, hardware, and compute infrastructure.

A key enabler is capital. Meta, now valued at $1.66 trillion, generates highly stable cash flows via its mature ad business. In its latest earnings, Meta disclosed improvements in ad performance and pricing, driven by AI-powered recommendations. This gives Meta the room to spend aggressively.

For 2025, the company has guided toward capital expenditures of $66–72 billion, with a majority earmarked for AI data centers, GPUs, chips, and global infrastructure buildout. Key projects include Prometheus (in Ohio) and Hyperion (in Louisiana)—two of the largest dedicated AI superclusters in the world. Meta has reportedly purchased millions of GPUs for these efforts.

Scale AI’s role fits here: it helps lay the foundation not just for large language models but for improved ranking algorithms, content moderation, and generative ad rendering systems—moving from infrastructure to revenue.

Manus sits at the other end of this vision. It will help Meta ship AI agents, consumer-facing interfaces, and enterprise tools trained on or compatible with Meta’s flagship models like Llama.

Zuckerberg’s approach spans the stack.

He wants to upgrade Meta’s in-house models Llama to power both internal services and external, open-source ecosystems. These models already underpin Meta AI—its assistant now embedded across Facebook, Instagram, and WhatsApp.

One opinion has been repeatedly emphasized that one of the primary use cases of AI infrastructure is to train and deploy better ranking, recommendation, and generative ad engines. In theory, AI → better ads → higher monetization → more reinvestment.

Meanwhile, the open-sourcing of Llama is a calculated bet: get enterprises to build agents on Meta infrastructure. The Manus acquisition supports that bet—providing an application layer and agent framework to help businesses plug into Meta’s AI vision.

Meta in Distress

Tools may be in place. But the flywheel still hinges on two things: user retention on Meta’s sprawling social platforms, and meaningful progress on Llama development.

Right now, both face pressure.

Meta’s core advantage—social media dominance—is no longer secure. X’s owner, Elon Musk, now rivals Zuckerberg not only in cultural reach but product ambition.

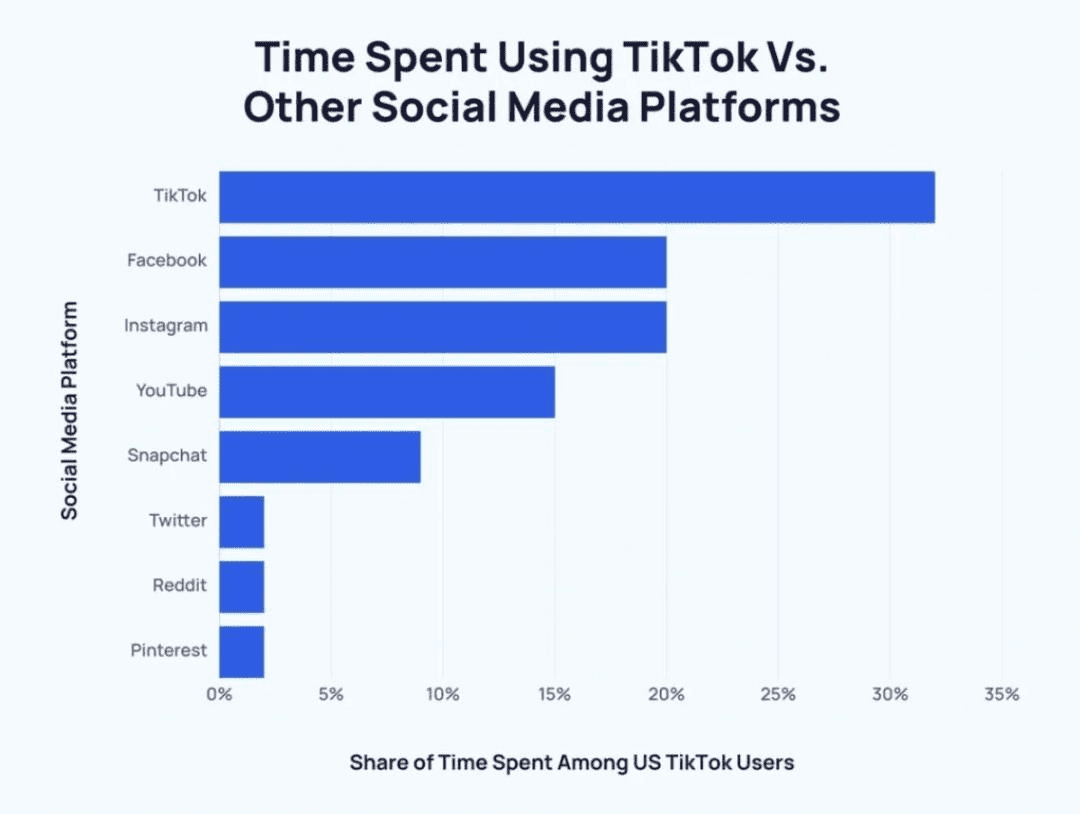

More worryingly for Meta, competition from China is growing. TikTok, with over 2.05 billion MAUs, has become the dominant global platform. In the U.S. alone, users now spend nearly 32% of their social media time on TikTok—far more than on Facebook or Instagram.

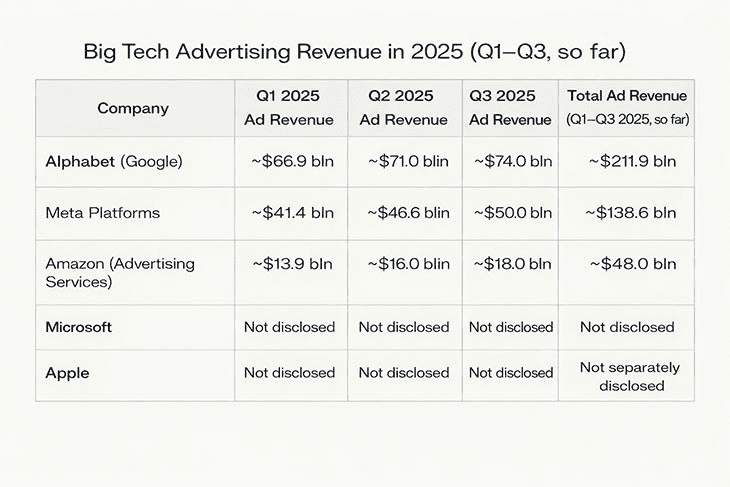

Beyond that, Alphabet and Amazon are both gaining ground in digital advertising—in some cases faster. YouTube’s monetization benefits from AI-enhanced search and recommendations; Amazon's ad business has outpaced both Meta and Google in three-year CAGR metrics.

The greater challenge for Meta’s AI vision may lie not in the pressure on its core business—but in the strategy and leadership guiding it. In 2021, Zuckerberg doubled down on the metaverse—announcing $100 billion in long-term R&D over 10 years. The stock soared at that time.

Despite early hype, Meta has offered no substantial updates on the metaverse this year. Its most recent “mixed reality” headset rollout underwhelmed analysts, and Q2 VR shipments totaled just 710,000 units. AR hardware sales globally remain capped at ~4 million annually.

Its Phoenix MF-X goggles—originally slated for H2 2026—have now been delayed to 2027, with Meta citing the need for more refinement. In December, reports emerged that the Reality Labs division would see budgets cut by up to 30%.

Meanwhile, Llama 4 failed to make a major impression among developers. Disappointed by the tepid response, Meta restructured its GenAI org and reassigned key AGI leadership—signaling internal dissatisfaction.

Is Now the Time to Buy Meta?

News of the Manus acquisition pushed Meta stock up over 1% pre-market Tuesday—clear evidence that investors still reward ambitious AI moves.

And there are fundamentals to support optimism.

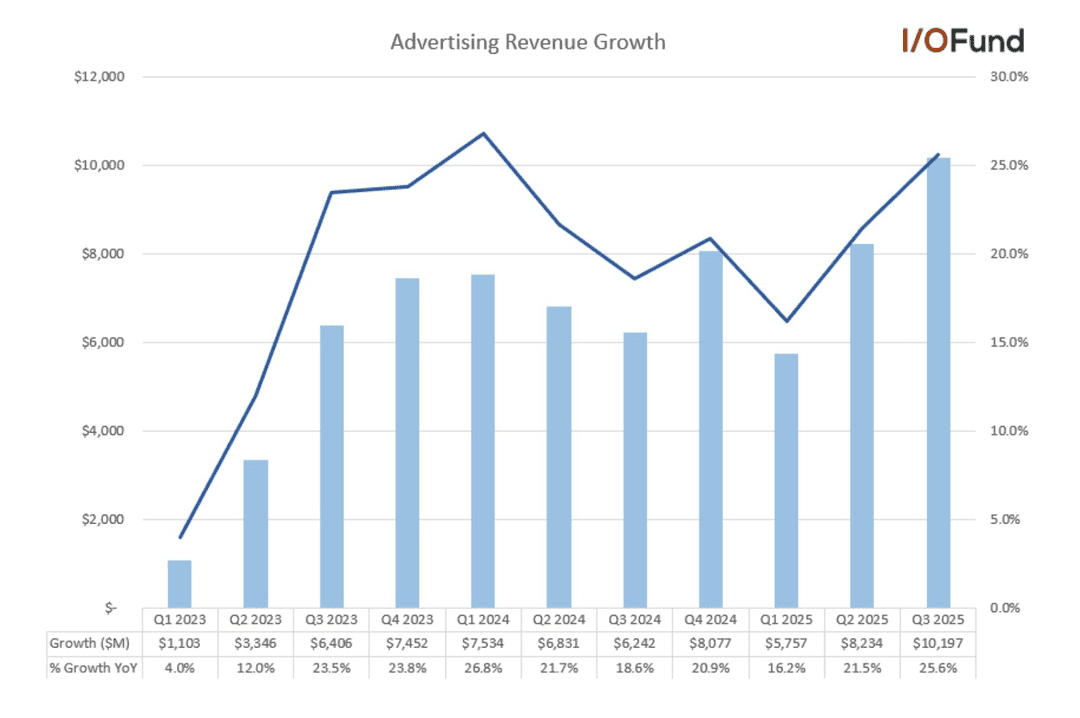

In Q3, Meta’s ad revenue rose 25.6% YoY—its fastest pace in six quarters. Q2 and Q3 represented two of the strongest revenue acceleration prints ever, up 16.2% and 21.5%, respectively. That momentum may continue into Q4, and even may hold over 20% through 2026.

But rising CapEx may complicate the picture.

In Meta’s last earnings call, management devoted significant time to explaining why aggressive investment in compute infrastructure is necessary. The cost? Free cash flow pressure and a drag on operating margins.

The company expects 2026 CapEx to be "significantly above" the 2025 range—due to rising infrastructure, new cloud service costs, depreciation, and personnel expenses. Seeking Alpha analysts estimate 2026 CapEx could hit $103 billion—up $32B YoY.

If so, FCF may fall nearly 50% in 2026—a structural echo of the 2022 cash crunch.

From a valuation standpoint, Meta still looks inexpensive relative to peers.

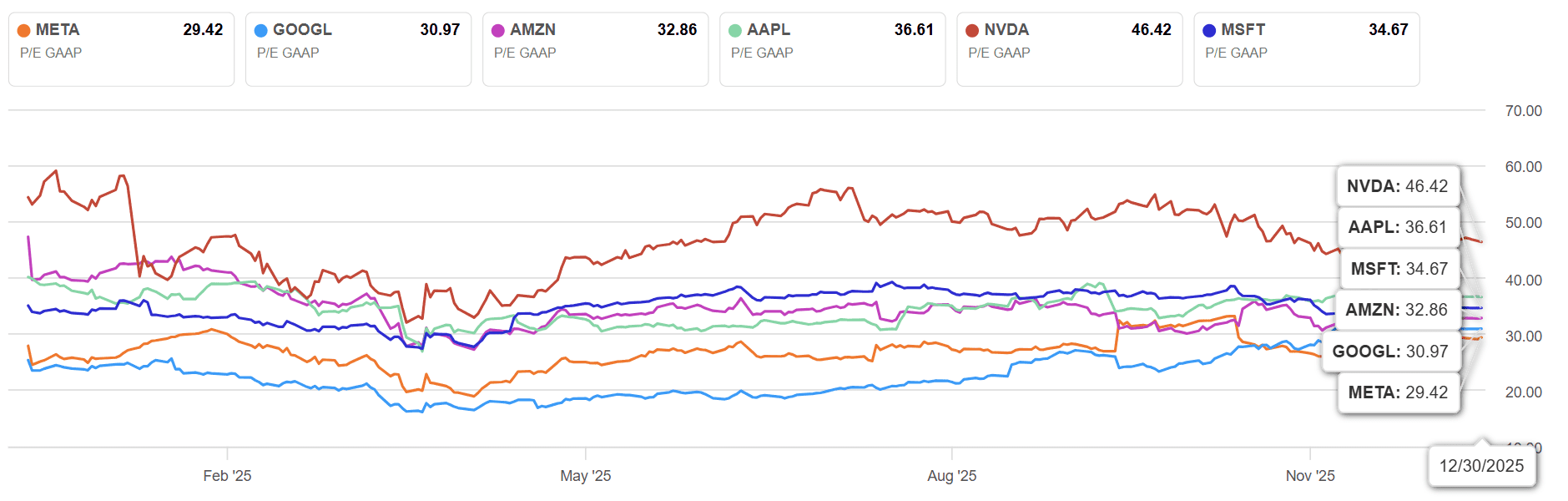

According to Seeking Alpha, its TTM PE ratio stands at 29.1—below Google (30.97) and Amazon (32.86). On that basis, Meta is the cheapest among the “Magnificent Seven.”

However, its 5-year forward PE average is 22.8—well below today’s forward PE of 26.2. The stock isn’t expensive, but it’s no longer obviously cheap.

Fundamentally, Google has Gemini and TPUs. Amazon dominates cloud infrastructure with real AI-linked revenue. Meta has yet to land a definitive result. Its strategy reflects a bold full-stack bet on AI—but ROI is still unclear, and monetization pathways, less proven.

For now, a wait-and-see approach remains a cautious yet reasonable stance.

But if Meta surprises with major AI product gains—or executes its open platform gambit more effectively than expected—it may once again redefine the narrative.

Investors, as always, are watching.

Recommended Articles