Alibaba Cloud & AI: Can Full-Stack Capabilities, Business Use Cases, and a Data Flywheel Reshape the ‘China Google Cloud’ Valuation Narrative?

Key Takeaways

The core strength of Alibaba Cloud’s AI business does not lie in any single point technology, but in the integrated system of “full-stack capabilities + live business use cases + data flywheel”. In the China market, its role is closer to a China version of Google Cloud, enhanced by e-commerce and local services ecosystems, rather than simply a domestic copy of AWS. At group level, cloud and AI have already taken over as the main growth engine, while the company has chosen to trade near-term profit and free cash flow for a new round of heavy investment, a phase that has some similarity with Azure’s development stage back then. Market pricing of these assets remains conservative: the revenue contribution from cloud and AI and the capex trajectory are already visible in the financial statements, but from the valuation performance so far, a full-blown AI rerating has yet to happen.

Global Cloud AI Landscape: Where Alibaba Cloud Stands

Within the global cloud and AI landscape, AWS, Azure, Google Cloud and Alibaba Cloud each show distinct strategic focus and ecosystem characteristics. The table below provides a brief comparison of the four players:

Company | Core positioning | Ecosystem foundation | AI strategic focus | Main customer types |

Alibaba Cloud | Full-stack AI capabilities + e-commerce / local services scenarios | Taobao, Tmall, local services, payments, finance, government | Qwen model family, Bailian platform, industry solutions, closed-loop scenarios | Chinese enterprises, multinationals operating in China, vertical-industry clients |

AWS | General-purpose cloud infrastructure and developer platform | Internet and innovation-driven companies | Broad AI services and tools | Enterprises of all sizes, with a high share of developers |

Azure | Enterprise IT + AI platform | Office, Windows, Active Directory, GitHub enterprise ecosystem | Embedding AI into enterprise productivity and business systems | Traditional medium and large enterprises, IT departments as primary owners |

Google Cloud | Cloud + AI native | Search, advertising and developer ecosystem | AI-first strategy centered on Gemini and Vertex AI | Technology and data-driven companies |

AWS is more oriented toward general-purpose infrastructure and developer platforms, serving customers from start-ups to large internet players with a wide range of IaaS and PaaS offerings on top of which enterprises build their own systems. This model gives customers a high degree of technical freedom but also requires strong in-house capabilities for architecture design and operations.

Azure, backed by Microsoft’s Office, Windows, Active Directory and GitHub ecosystems, is more like a platform that helps traditional enterprises upgrade their IT systems as a whole, focusing on migrating legacy IT assets to a cloud+AI architecture and embedding AI into day-to-day productivity and business workflows via Copilot, Teams and Microsoft 365, which gives it a natural edge among enterprises already deeply tied into Microsoft products.

Google Cloud in the past two years has pushed its AI-first strategy to the forefront, with the Gemini series of models and the Vertex AI platform at the core of its cloud business, and many new services are designed from day one with an AI-native mindset, which is highly attractive to companies that are heavily dependent on data and model capabilities.

Alibaba Cloud’s situation is not fully comparable with any of the three. On the one hand, it has to play the role of a general-purpose cloud service provider; on the other hand, it is deeply embedded in Alibaba’s own e-commerce, local services and payments businesses.

Structurally, Alibaba Cloud in the China market effectively owns a complete loop from compute, platform and models to applications and data: at the compute layer, it runs a hybrid architecture of self-developed chips and Nvidia GPUs; at the platform layer, it has the Bailian MaaS platform and data middle platform; at the model layer, it has the Qwen family of models; at the application layer, it powers large-scale businesses such as Taobao, Tmall, local services, payments, finance and government services; and at the data layer, it is fed by the real transaction and behavioral data generated by these businesses each day. This structure makes Alibaba Cloud closer to a cloud+AI platform with e-commerce and local services in its DNA, rather than simply a cloud vendor selling compute or tools.

From a valuation perspective, Alibaba is often compared to Google, whose current forward P/E is just above 30 times, whereas Alibaba trades around 20 times. A naïve multiple comparison would suggest that Alibaba is undervalued, but this ignores multiple layers of differences:

On one hand, large-cap U.S. tech companies enjoy higher liquidity and legal-transparency premia; on the other hand, the cash-flow stability and maturity of Google’s cloud and advertising businesses remain higher than Alibaba’s at this stage; more importantly, Alibaba’s full-stack ecosystem, while offering structural advantages, also increases internal coordination complexity. The introduction of AI also disrupts existing monetization models, leading investors to take a cautious stance on valuation and to adjust their views gradually based on management’s execution.

Looking at capex and balance sheet data versus global tech giants makes the intensity of AI+cloud investment more intuitive, with data as of September 30, 2025:

Company | Cash & short-term investments ($B) | Capex over last 4 quarters ($B) | Notes | Ratio (Capex / Cash) |

Alibaba | 46.118 | ~16 | Investment in AI and cloud infrastructure | ~35% |

Alphabet | 98.496 | ~87–90 | Majority into AI and cloud computing | ~93–109% |

Microsoft | 102.012 | ~50–55 | Mainly data centers and technical infrastructure | ~49–54% |

Amazon | 94.197 | ~60–70 | Mainly into AWS and AI | ~64–74% |

Meta Platforms | 44.450 | ~70–72 | Mainly AI infrastructure and data centers | ~62% |

On the AI infrastructure layer, Alibaba’s capex strategy in the past two years has shifted from defense to offense. Although Alibaba’s absolute capex still lags U.S. peers, the investment intensity relative to its own cash scale is high.

For a long time, Alibaba Cloud’s spending on servers and data centers mainly aimed to keep up with industry progress, meet existing client needs and defend market share. Since mid-2024, management has explicitly highlighted ramped-up AI investment and announced a roughly RMB 380 billion three-year capex plan.

The main directions are AI servers, GPUs and self-developed chips, and expansion and upgrades of domestic and overseas data centers, with about 80% of the funds going to AI servers, Nvidia GPUs and in-house AI chips, and the remainder to domestic node upgrades and overseas expansion.

This strategy is similar in some respects to Azure’s earlier heavy-investment phase: when cloud and AI enter a scale game, companies first build out infrastructure to secure high-quality customers and key scenarios, and then repair margins through scale and product mix. The difference is that Alibaba already holds a leading position in China’s cloud market and owns e-commerce and local services traffic and data as a starting advantage.

In the short term, such land-grab investment directly compresses margins and free cash flow and does not look attractive at first glance in financial statements. However, whether the strategy is reasonable cannot be judged on current-period profit alone, but needs to be assessed from a medium- to long-term perspective:

Whether unit compute cost declines as self-developed chips scale up; whether the share of AI-related external revenue keeps rising; and whether overseas nodes can translate into revenue and profit from multinational clients within three to five years. If the answers to these questions skew positive, today’s investment is likely to support a valuation rerating over the medium to long term.

FY2026Q2 Earnings: Cloud & AI Take Over the Growth

The latest quarterly report shows that cloud and AI have taken over as Alibaba’s main growth driver, while profit and cash flow are clearly being held back by investment. For the quarter ended September 30, 2025, Alibaba’s total revenue grew roughly 5% year-on-year. Adjusted for the deconsolidation of Sun Art Retail and some offline businesses, comparable revenue growth would be around 15%. Net income attributable to ordinary shareholders was RMB 20.99 billion, down more than 50% year-on-year, mainly due to increased investment in on-demand retail and cloud AI infrastructure rather than deterioration in core operations.

Data Source: StockAnslysis, TradingKey

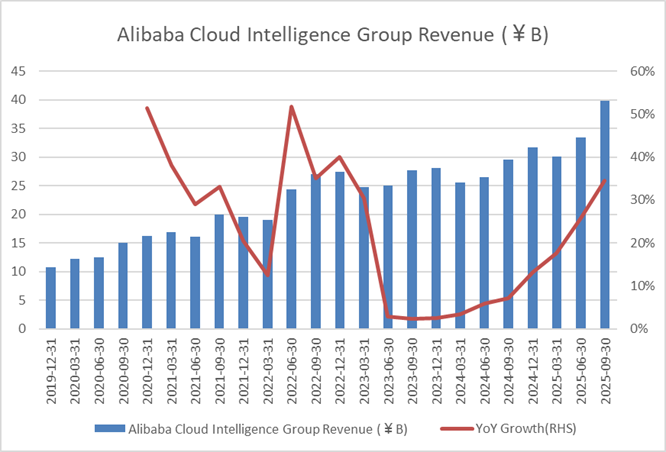

Cloud was the standout segment of the quarter. Cloud computing revenue was about RMB 39.8 billion, up 34% year-on-year, with revenue from external customers rising about 29%. Management disclosed that AI-related product revenue has delivered triple-digit year-on-year growth for nine consecutive quarters and now accounts for more than 20% of Alibaba Cloud’s external commercial revenue, indicating that AI has moved from concept and pilots to being a meaningful revenue contributor within the cloud business.

While cloud and AI revenue growth has clearly accelerated, margins and free cash flow have moved in the opposite direction, a pattern often seen when cloud businesses enter a heavy-investment phase in infrastructure. These investments are helping Alibaba build structural advantages.

Self-Developed Chips: Positioning & Comparsion

On the chip side, Alibaba has built a self-developed portfolio centered on the Yitian 710 CPU, the Hanguang 800 inference accelerator and the PPU, designed to complement the Nvidia ecosystem. In terms of positioning and benchmarks:

Chip | Role | Benchmark | Core function |

Yitian 710 | Server CPU | Intel Xeon / AMD EPYC | Improve energy efficiency and lower base-layer cloud computing costs |

Hanguang 800 | AI inference accelerator | Nvidia T4 / L4 | Reduce inference costs and improve AI business gross margin |

PPU | General-purpose training + inference | Nvidia H20 | Provide high cost-performance compute and enhance supply-chain autonomy |

In practical deployment, training of large models and high-complexity inference workloads still rely heavily on Nvidia GPUs, which reflects current industry reality and reasonable client preferences. However, for large numbers of standardized inference tasks and some general-purpose compute workloads, substituting part of imported chips with self-developed chips can significantly lower compute cost and energy consumption.

For the cloud business, this is both a key lever to improve gross margins and a risk buffer against external policy uncertainties.

Qwen, Bailian & Data Flywheel

Alibaba’s AI strategy is not about betting on a single large model or platform tool, but about pushing forward across the whole chain. The model layer is Qwen, the platform layer is Bailian, the compute layer is Alibaba Cloud plus self-developed chips, and the application and data layers are Taobao, local services, payments, finance and other business scenarios.

On the model layer, Qwen has evolved from an internal-use large model into the foundational infrastructure of Alibaba’s AI system. The Qwen family continues to broaden parameter scales and task coverage, and offers variants tailored for verticals such as finance, government, manufacturing and healthcare, providing a model base for subsequent industry solutions. Through open-sourcing and community building, external developer adoption of Qwen continues to rise, strengthening its influence as AI infrastructure.

On the platform layer, Bailian undertakes the task of productizing model capabilities. Traditional enterprises building an RAG system from scratch must handle multiple steps such as vectorization, retrieval, reranking, dialog management, log monitoring and compliance, which involves high engineering complexity. Bailian encapsulates these complexities into components and templates, enabling developers to accomplish within a much shorter timeframe what used to require months of engineering work. For Alibaba itself, Bailian also serves as a platform to standardize and externalize its internal learnings: many best practices refined repeatedly in Taobao, local services and payments are distilled into reusable modules and process templates.

Alibaba’s fundamental differentiation from other cloud vendors lies in its closed-loop capability at the application and data layers. Other cloud providers can offer compute and models, but lack high-frequency, large-scale e-commerce scenarios like Taobao and local services networks like Ele.me and Koubei.

Alibaba can continuously test and optimize AI solutions in these environments and, when selling to enterprise customers, demonstrate how long solutions have run in its own systems and what concrete improvements they have delivered, rather than staying at the level of lab metrics and theoretical arguments. Over the long term, this closed loop grounded in real business scenarios and data will likely become the hardest-to-replicate part of Alibaba’s AI system.

Consumer-side Challenges, Enterprise-side Scaling

From a business-model perspective, consumer and enterprise AI applications follow very different paths.

On the consumer side, new AI apps emerge constantly and product iterations are rapid, but so far, neither in China nor overseas has a large-model consumer app established a highly certain and sustainable profit model. Users can switch between apps at low cost, subscription revenue is sensitive to sentiment and competition, and players are still exploring different monetization paths including subscriptions, advertising and revenue sharing. At this stage, it is more prudent to view consumer AI primarily as brand exposure and entry-point layout.

Enterprise AI has moved from pilots toward production-grade systems. More and more companies are no longer just seeing what AI can do, but are introducing RAG systems, vertical-industry models and automation flows with clear objectives, such as reducing customer-service cost, improving conversion, strengthening risk control or optimizing supply chains. These projects tend to involve larger contract values, longer implementation cycles, and meaningful upsell and renewal opportunities, and once embedded into core processes, switching costs rise over time. Alibaba’s edge in this segment lies in Qwen and Bailian providing general and platform-level capabilities, while its extensive experience in e-commerce and local services helps package common needs into semi-standardized industry solutions.

For clients, building an AI system from scratch involves four stages: requirements analysis, system design, model tuning and iterative launch, whereas using solutions already proven at Alibaba can significantly shorten the first three stages and reduce uncertainty. As capital markets shift their focus from consumer AI hype to enterprise orders, renewals and project margins, this structural advantage is becoming more visible.

Risks & Long-term Outlook

Overall, the key risks for Alibaba’s cloud and AI business fall into three areas.

First is competitive risk: intense competition among domestic cloud vendors, e-commerce platforms and on-demand retail players will continue to pressure near-term margins.

Second is capex and execution risk: the current high-investment strategy assumes sustained high growth in cloud and AI over the next several years, and if macro conditions or technology progress fall short of expectations, payback periods may lengthen.

Third is policy and supply-chain risk: U.S. export controls on advanced chips remain uncertain, and there are timing and performance uncertainties in the R&D and mass production of self-developed chips.

With these risks in mind, the long-term outlook for Alibaba’s cloud and AI business remains constructive for several reasons.

First, cloud and AI are already delivering high growth in reported numbers and are likely to keep increasing their share of group revenue, representing one of the few segments still capable of mid- to high-speed growth.

Second, self-developed chips, Qwen, the Bailian platform and e-commerce/local services scenarios have formed a mutually reinforcing structure, making it less likely that any single-point risk will escalate into a systemic issue.

Third, compared with other domestic players, Alibaba’s resource commitment and business foundation give it a relatively advantaged position in China’s AI infrastructure race.

Fourth, from a valuation angle, relative to overseas cloud vendors, the market has yet to fully price in Alibaba’s cloud and AI assets, leaving room for future performance and execution to close the gap.

Over a three- to five-year horizon, as long as cloud revenue growth stays at a healthy level, AI-related revenue share rises steadily, cost advantages from self-developed chips gradually materialize, and the roles of internal business lines in the AI era become clearer, Alibaba’s cloud and AI business can continue to act as a key force driving a rerating of the group’s overall valuation.

Recommended Articles