U.S. Q1 Stagflation Confirmed – Could Q2 GDP Growth Rebound Above 3%?

TradingKey - Newly released data from the U.S. Department of Commerce shows that the U.S. economy unexpectedly contracted in the first quarter of 2025, reversing a three-year growth trend. Combined with upward revisions to inflation indicators, this confirms that the U.S. economy entered a stagflationary phase during the period. However, analysts believe that thanks to shifting tariff policies, Q2 GDP growth could rebound above 3%.

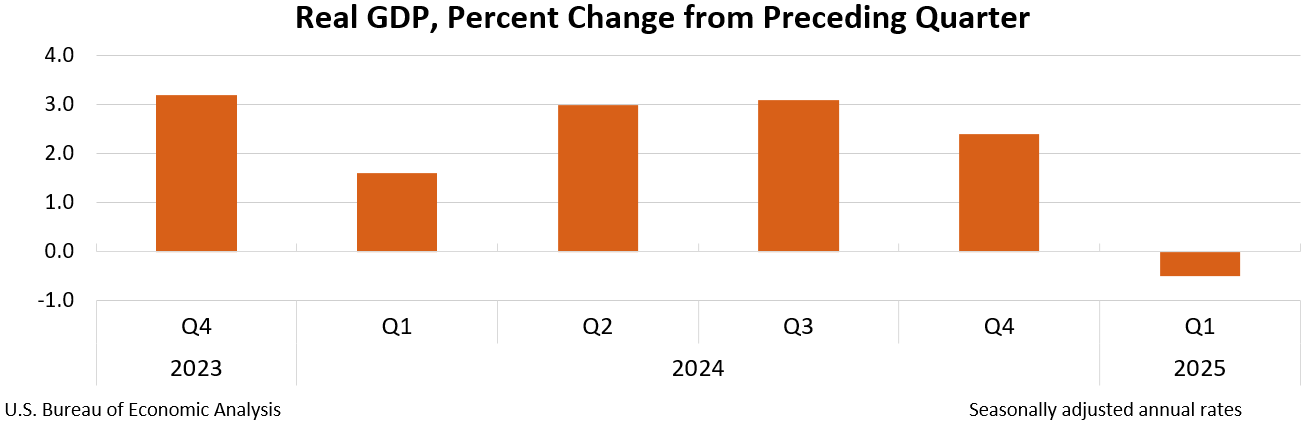

On Thursday, June 26, the U.S. Bureau of Economic Analysis released its third and final estimate for Q1 GDP: real GDP declined by 0.5% year-over-year, worse than the previous revised reading of -0.2%, and a sharp contrast to Q4 2024’s +2.4% growth. This marked the first economic contraction since Q1 2022 — ending a nearly three-year streak of expansion.

U.S. Real GDP YoY, Source: BEA

The report attributed the Q1 decline to a surge in imports (+37.9%), reduced government spending (-4.9%), and slowing consumer expenditure.

Ahead of President Trump’s announced tariff hikes on April 2 — dubbed “Liberation Day” — many U.S. companies accelerated purchases to avoid additional costs, causing a sharp rise in imports, which act as a subtraction in GDP calculations. Meanwhile, large-scale government spending cuts led by Elon Musk’s Department of Government Efficiency (DOGE) also weighed on economic momentum.

More concerning, however, was the slowdown in personal consumption, which rose just 0.5%, far below the initial estimate of 1.7% and the prior revised level of 1.2%. That marked the weakest consumer growth since the early days of the pandemic. As a result, the contribution of personal consumption to GDP was revised down from an initial 1.21% to just 0.30% .

Economists at Oxford Economics noted that the downward revision to final sales to domestic purchasers — the engine of the U.S. economy — was more worrying than the headline GDP contraction itself. Analysts at EY pointed out that American households significantly cut back on discretionary spending, particularly in entertainment and dining sectors.

Meanwhile, the GDP price index rose 3.4% year-over-year, up 0.1 percentage point from the previous estimate. The Personal Consumption Expenditures (PCE) price index and core PCE (excluding food and energy) were both revised higher by 0.1 percentage points, reaching 3.7% and 3.5% , respectively.

This means that the U.S. economy officially entered a stagflationary environment in Q1 — a scenario long feared by Wall Street.

Q2 Outlook: Hope on the Horizon

Despite the disappointing Q1 performance, analysts are taking a more optimistic view of Q2 GDP growth, citing evolving tariff policy dynamics and normalization of import activity.

According to FactSet, Q2 GDP is expected to rebound to above 3% .

Some analysts argue that the surge in Q1 imports will not be repeated in Q2, removing a key drag on GDP figures.

As of June 20:

- Bank of America forecasts 2.6% Q2 GDP growth.

- Goldman Sachs expects 4.1%.

- The Atlanta Fed’s GDPNow model projects 3.4%, with the next update scheduled for June 27.

Recommended Articles