Eurozone August CPI Commentary: Will the Euro's Range-Bound Fluctuation Continue?

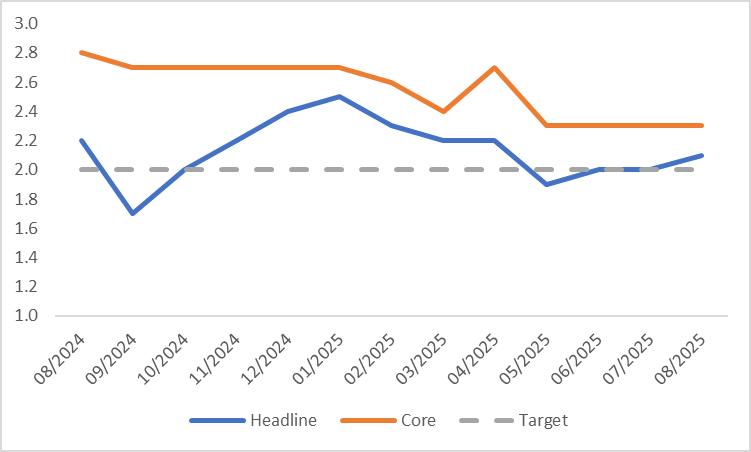

TradingKey - On 2 September 2025, the Eurozone released its inflation data for August. The headline Consumer Price Index (CPI) edged up to 2.1% from 2.0% in July, in line with market expectations; the core CPI remained unchanged from July at 2.3%, 0.1 percentage points higher than the market forecast.

Looking ahead, inflation in the Eurozone will continue to be shaped by two opposing forces—one reducing and the other driving it. Factors that will reduce inflation include: a slowdown in Eurozone economic growth, a moderate easing of trade frictions between Europe and the U.S., and persistently low energy prices. On the other hand, factors that will drive inflation higher are: slightly stronger-than-expected wage growth in the Eurozone and Germany’s plan to raise the minimum wage over the next two years. With these two forces counterbalancing each other, the risk of severe reflation is expected to remain low. Consequently, we anticipate that the European Central Bank (ECB) will continue to maintain its accommodative monetary policy.

In the analysis of the foreign exchange market, on one hand, the global trend of de-dollarization and the Federal Reserve's resumption of the interest rate cut cycle will continue to weigh on the U.S. dollar; on the other hand, the weak economic growth in the Eurozone, coupled with the European Central Bank's ongoing interest rate cut measures, will drag on the euro. Affected by the weakening of both currencies in this pair, we believe that EUR/USD will enter a phase of range-bound fluctuation.

Source: TradingKey

Main Body

On 2 September 2025, the Eurozone released its inflation data for August. The headline Consumer Price Index (CPI) edged up slightly from 2% in July to 2.1%, in line with market expectations; the core CPI remained unchanged from July at 2.3%, 0.1 percentage points higher than market forecasts (Figure 1).

Figure 1: Market Consensus Forecasts vs. Actual Data

Source: Refinitiv, TradingKey

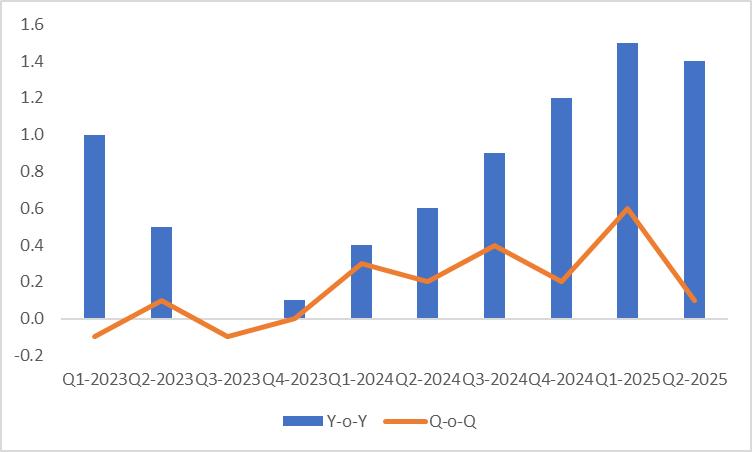

From the perspective of inflation classification, although service sector inflation has continued its downward trend, the stickiness of core goods prices persists. This indicates that even as the Eurozone economy remains weak, the price pressures at the goods level have not been significantly alleviated. From a country perspective, Germany’s inflation rose to 2.1% due to the low base effect from the same period last year; Italy and Spain saw generally stable inflation levels, while France’s inflation declined slightly.

Figure 2: Eurozone CPI (%, y-o-y)

Source: Refinitiv, TradingKey

Looking ahead, inflation in the Eurozone will continue to be shaped by two opposing forces—one reducing and the other driving it upward. On the inflation-reducing side, the slowdown in Eurozone economic growth (Figure 3), the easing of trade frictions between Europe and the U.S., and persistently low energy prices are all alleviating inflationary pressures in the region. On the inflation-driving side, wage growth has been slightly higher than expected: in the second quarter, hourly wages and collectively agreed wages rose by 3.7% and 4.0% year-on-year, respectively. Additionally, Germany’s plan to raise the minimum wage over the next two years will further add upward momentum to inflation.

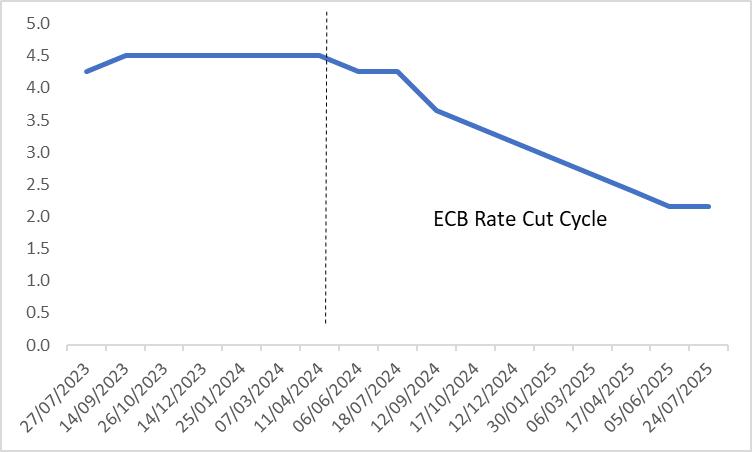

Under the interplay of these dynamics, the Eurozone CPI is expected to hover near the European Central Bank's (ECB) target level in the coming months. Given the low risk of significant re-inflation, we anticipate that the ECB will maintain its accommodative monetary policy (Figure 4), with the Eurozone likely entering a low-interest-rate environment by the first half of 2026.

In the forex market analysis, the global trend toward de-dollarisation and the Federal Reserve’s resumption of its rate-cutting cycle are expected to continue weighing on the U.S. dollar. Meanwhile, the Eurozone’s sluggish economic growth, combined with the ECB’s ongoing rate cuts, will likely pressure the euro. Given the weakening forces on both currencies, we anticipate that the EUR/USD exchange rate will enter a phase of range-bound trading.

Figure 3: Eurozone Real GDP (%)

Source: Refinitiv, TradingKey

Figure 4: ECB Policy Rate (%)

Source: Refinitiv, TradingKey

Get Started

Recommended Articles