Bank of England Chief Sounds Alarm on Big Bank Stablecoin Issuance

Bank of England Governor Andrew Bailey has warned against allowing major banks to issue their own stablecoins.

This clearly contrasts with the US, where stablecoin adoption remains one of the biggest agenda items in Trump’s push to make the US a crypto capital of the world.

Bailey Favors Tokenized Deposits Over Stablecoins to Safeguard Financial Stability

Bailey cited risks to financial stability, lending capacity, and the potential for large-scale money laundering as reasons for his preference for banks adopting tokenized deposits.

This means the BoE chief favors digital versions of traditional money as opposed to creating or supporting privately issued stablecoins.

His remarks come amid ongoing transformation in the global financial system, with the lines between traditional banking and decentralized finance (DeFi) increasingly becoming blurred.

Bailey’s position reflects deep concern within the UK’s central banking leadership that the unchecked rise of stablecoins could undermine the core functions of modern banking, which are monetary control and credit creation.

“If stablecoins take money out of the banking system, banks have less capacity to lend,” Bloomberg reported Bailey’s warning, citing an interview with the Times.

The BoE governor also argued that financial institutions’ mass adoption of stablecoins could lead to disintermediation, liquidity imbalances, and a heightened risk of sudden withdrawals, especially during periods of market stress.

Notably, such a scenario is termed a Bank run, akin to what happened during the FTX collapse.

It aligns with a recent report, where European officials warned that USD stablecoins threaten euro sovereignty and stability.

Against this backdrop, MiCA regulations introduce strict rules to boost euro-backed digital innovation.

Stablecoin Crime Risks and a Growing UK–US Policy Divide on Digital Money

Bailey, who also chairs the Financial Stability Board (FSB), a key global body overseeing systemic financial risks, extended his critique to include concerns over financial crime.

With vast sums potentially moving through private stablecoin networks outside regulated channels, he said there is an increased danger of enabling criminal activities such as money laundering, without sufficient oversight or safeguards.

This stance puts the UK at odds with the US under President Donald Trump, whose administration has taken a far more permissive approach.

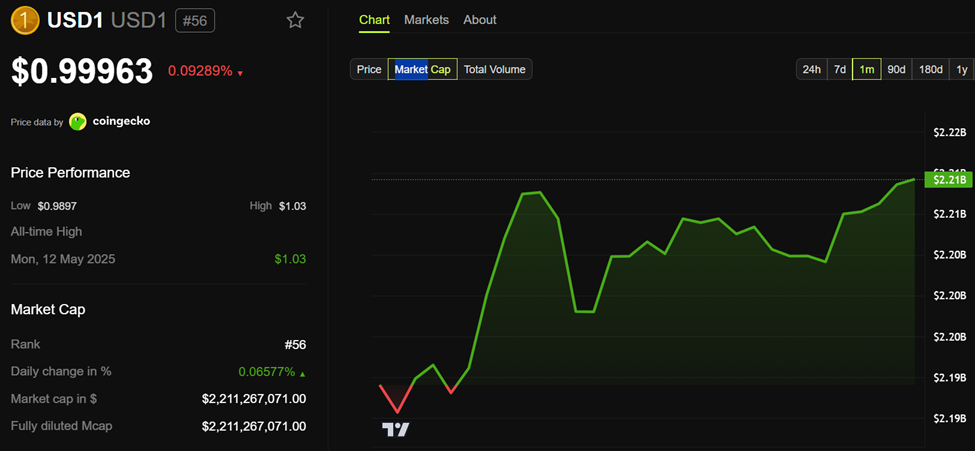

New US legislation lays the groundwork for regulated stablecoin adoption under the GENIUS Act. In the same way, it sets the stage for a Trump-affiliated dollar-backed stablecoin, USD1, which has already amassed a $2.2 billion market cap.

USD1 Stablecoin Market Cap. Source: BeInCrypto

USD1 Stablecoin Market Cap. Source: BeInCrypto

The UK, by contrast, appears more cautious, preferring a model that integrates digital finance into existing monetary infrastructure rather than bypassing it.

“As a result of this growing concern with US stablecoins, the ECB has once again underscored the need for the digital euro as a possible counterweight,” Economic Governance and EMU Scrutiny Unit (EGOV) said recently.

Bailey’s comments also cast doubt on the prospect of a central bank digital currency (CBDC) in the UK. He hinted that issuing a digital pound may be unnecessary, calling it “sensible” for the UK to focus instead on digitizing commercial bank deposits.

The BoE chief says this model is more compatible with the existing banking system and less disruptive to monetary policy transmission.

Meanwhile, his preference for tokenized deposits signals a broader push to modernize payments and settlement rails while preserving banks’ role as credit intermediaries.

Recommended Articles