1 Outstanding Growth Stock That Is a No-Brainer Buy on the Dip

Key Points

Shopify is looking to turn the threat of artificial intelligence into an opportunity, with some success so far.

The company's financial results remain strong.

Shopify isn't cheap, but it could justify its valuation over the long run.

- 10 stocks we like better than Shopify ›

Software companies are experiencing a sell-off this year. Shopify (NASDAQ: SHOP), a corporation that runs a cloud-based platform that allows online merchants to start and run e-commerce stores, hasn't escaped the bloodbath. The company's shares are down by 34% to date. However, at current levels, it might be a great idea to invest in Shopify, as the stock has what it takes to rebound and perform well over the long run. Here's why the e-commerce specialist might be a no-brainer buy.

Image source: The Motley Fool.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Financial results tell a compelling story

One reason some investors are running away from software stocks is that they think artificial intelligence (AI) might displace many of their services. My view is that AI is an extremely useful tool that will improve productivity. That is already happening: innovative companies are evolving in tandem with AI and launching tools that make their customers' lives easier. Shopify is doing the same. The company launched an AI website generator that can get the job done in a few minutes with just a basic description of what people want. Shopify has launched other AI tools, including an AI assistant that helps answer questions and navigate services more quickly and effectively.

Besides the work it is doing with AI, Shopify's financial results remain excellent. In the first quarter, the company's revenue grew by a strong 34% year over year to $3.2 billion, on the back of an almost 35% growth in gross merchandise volume, which reached $100 billion. The company's free cash flow margin held steady at 15%. Shopify's net loss narrowed to $581 million, up from the $682 million net loss recorded in the year-ago period. Excluding the impact of equity investments, the company reported a net income of $360 million, up 59% year over year.

True, Shopify expects its second-quarter revenue growth rate to be in the high twenties, a slight deceleration compared to the first quarter. However, the business still looks solid, despite fears that AI will wreak havoc.

Looking at the valuation concerns

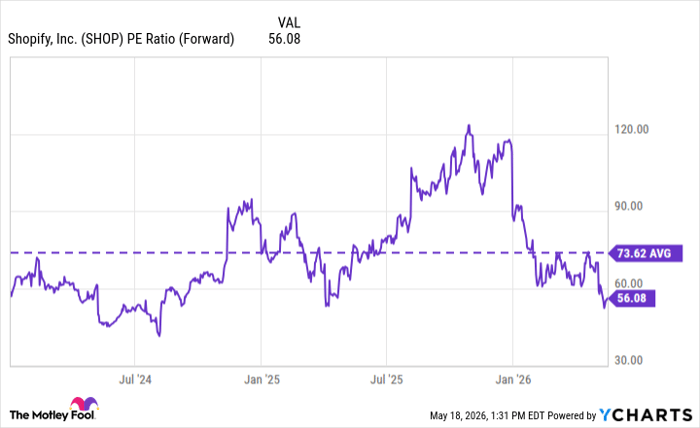

There is another thing the bears can point to: Shopify's shares look extremely expensive. The company is trading at about 56x forward earnings. That's miles ahead of the 24.3x average for information technology stocks. At these levels, Shopify has little room for error, and anything that falls short of market expectations might trigger a sell-off. However, it's worth pointing out that Shopify's current forward price-to-earnings ratio is well below its average over the past two years.

SHOP PE Ratio (Forward) data by YCharts

What does this mean for the stock? Growth stocks like Shopify often trade at high valuations. Provided Shopify can continue posting strong results while tapping into attractive opportunities, the stock could rebound and deliver market-beating returns, even from its current levels. My view is that Shopify is well-positioned to do that. The company has built a deep ecosystem of services that go well beyond just starting an online storefront and are invaluable to the merchants it serves.

It also boasts a strong moat from switching costs, considering the time and effort it can take to customize a store and attract clients to it, work that merchants won't want to have to redo, nor will they want to switch to another provider (which can bring business disruptions) unless they absolutely have to. Shopify has grown its market share in recent years, rising from 12% at the end of 2024 to 14% by the end of 2025.

Shopify also powers about 30% of e-commerce stores in the U.S., according to some estimates. Meanwhile, most retail commerce still takes place on-premises. And as that continues to move online, Shopify could be a major beneficiary. So, what's the verdict? Shopify is an excellent stock to buy on the dip. And at its current levels, the stock could still provide strong returns over the long run.

Should you buy stock in Shopify right now?

Before you buy stock in Shopify, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Shopify wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $483,476!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,362,941!*

Now, it’s worth noting Stock Advisor’s total average return is 998% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 19, 2026.

Prosper Junior Bakiny has positions in Shopify. The Motley Fool has positions in and recommends Shopify. The Motley Fool has a disclosure policy.

Recommended Articles