I Bought This Growth Stock When Everyone Else Was Selling, and It's Starting to Pay Off

Key Points

Duolingo is focused on user growth through 2028, which has led to a slowdown in revenue and earnings growth.

This strategy shift should yield extremely positive results over the long term, making the discounted stock a buy now.

The stock is cheap based on two widely used metrics, which could set the stage for significant upside.

- 10 stocks we like better than Duolingo ›

I have followed Duolingo (NASDAQ: DUOL) stock since it went public in 2021, but I didn't actually buy it until March of this year. It was down by more than 79% from its June 2025 record high when I decided to dive in at a time when most investors were fretting over two potential headwinds for its business.

Duolingo operates the world's largest digital language education platform. Management recently announced a plan to focus on user growth for the next couple of years, which has already caused a slowdown in the company's revenue and earnings growth. At the same time, there have been concerns that artificial intelligence (AI) could disrupt the platform's success.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Personally, I think Duolingo's renewed focus on user acquisition will yield significant long-term rewards for shareholders, and I also believe AI will be a tailwind, not a threat, to its business. The stock has already jumped 25% from my initial purchase price of around $90, and while it's way too early to declare victory, here's why I think significantly more upside could be ahead.

Image source: The Motley Fool.

AI is enhancing the learning experience

Duolingo's success stems from its mobile-first approach, which puts language education at the fingertips of practically anyone with a smartphone. Plus, its gamified and highly interactive lessons keep learners engaged, which is the key to monetizing them over the long term.

Duolingo had 56.5 million daily active users at the conclusion of the first quarter of 2026 (ended March 31), which was up 21% compared to the year-ago period. The majority of them were free users who Duolingo monetizes through advertising, but 12.5 million of them were paying a subscription fee to unlock additional features to accelerate their learning.

While some investors believe new AI-powered translation tools will make Duolingo's platform obsolete, the company is proving it can use this new technology to its advantage.

In 2024, it launched a new feature called Video Call, which is only available to users who pay for a Super Duolingo or Duolingo Max subscription. It uses an AI-powered digital avatar to help users practice their foreign language speaking skills, and during the first quarter, the average number of spoken words per user who engaged with the feature more than doubled compared to the year-ago period. In other words, Video Call is already a massive tailwind for engagement.

But Duolingo is also using AI behind the scenes. The company published 20,500 course units during the first quarter, up significantly from an average of 7,100 per quarter in 2025, thanks to AI-powered automation. This means lessons are added and updated more frequently to keep users coming back, and it also reduces costs because fewer human workers are required to draft content.

Faster user growth could be great for shareholders

Duolingo generated $292 million in revenue during the first quarter, which was up 27% year over year. While that was a solid growth rate, it marked a deceleration from the 38% growth the company delivered in the same quarter of 2025.

That is one of the drawbacks of management's decision to prioritize user acquisition over monetization. As part of this new strategy, Duolingo is offering more speaking-based lessons to free users in order to appeal to a wider audience. However, this diminishes the value of subscription-only features like Video Call, hence the slower revenue growth.

Revenue and earnings tend to drive stock prices, which explains why Duolingo shed so much value over the past year. However, management believes the platform's daily active user base will almost double to 100 million over the next two years as a result of this strategy shift.

In theory, a larger user base will make Duolingo harder to disrupt, thus making its business more defensible against competitive threats. Plus, the company will have more prospects to monetize in the future, leading to more revenue and profit.

If Duolingo turns its attention back to monetization in 2028 and converts free users into subscribers at the same rate as it did in 2025, then we can assume its paying user base and annualized revenue would roughly double from current levels. In other words, once the company has fortified its user base, I think its revenue growth could reaccelerate.

Duolingo's valuation leaves room for more upside

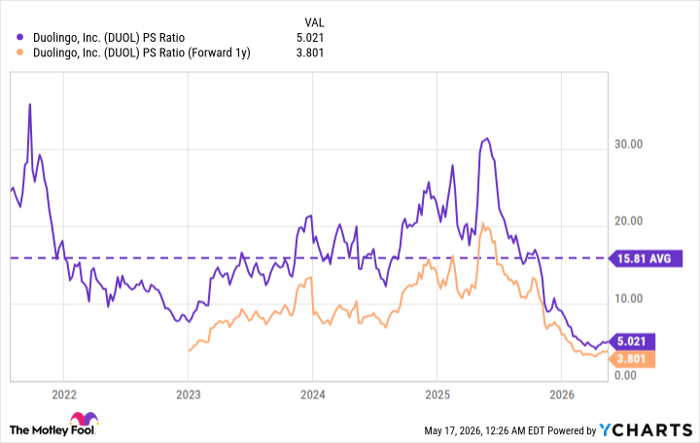

Duolingo stock is trading at a price-to-sales (P/S) ratio of just 5 as I write this, which is a steep discount to its average of 15.8 since going public in 2021. It's also trading at a forward P/S ratio of 3.8, based on Wall Street's $1.37 billion revenue estimate for 2027 (supplied by Yahoo! Finance). In other words, the stock looks like a bargain relative to its historical valuation.

Data by YCharts.

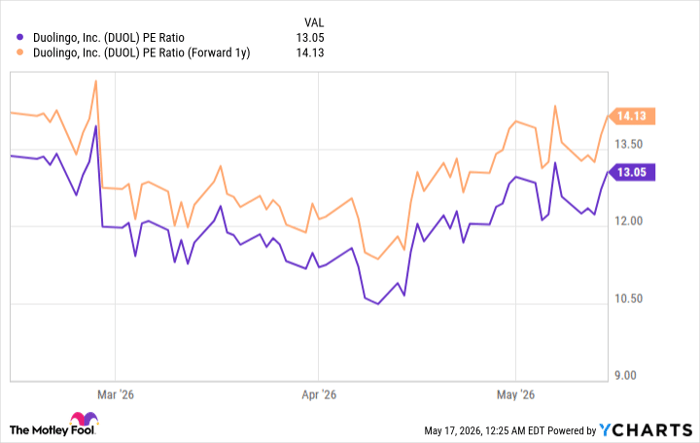

The stock also looks cheap by another widely used valuation method. Based on the company's trailing-12-month generally accepted accounting principles (GAAP) earnings of $8.74 per share, its stock is trading at a price-to-earnings (P/E) ratio of just 13.1, which is half the P/E ratio of the S&P 500 index. So, Duolingo is much cheaper than the broader market right now.

Moreover, Wall Street doesn't expect management's strategy shift to have a major impact on the company's bottom line, because the stock trades at a forward P/E ratio of 14.1 based on 2027 earnings estimates.

Data by YCharts.

In summary, Duolingo stock still looks cheap despite its 25% bounce since my purchase in March. That gives me confidence that more upside might be ahead -- but I plan to hold until at least 2028, because I think that's when investors will yield the biggest rewards.

Should you buy stock in Duolingo right now?

Before you buy stock in Duolingo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Duolingo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $469,293!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,381,332!*

Now, it’s worth noting Stock Advisor’s total average return is 993% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 19, 2026.

Anthony Di Pizio has positions in Duolingo. The Motley Fool has positions in and recommends Duolingo. The Motley Fool has a disclosure policy.

Recommended Articles