Prediction: Nvidia Stock Will Be Worth This Much by the End of 2028

Key Points

Nvidia's valuation is soaring thanks to accelerating buildouts of data centers from AI hyperscalers.

While data center infrastructure will continue to be a major growth driver for Nvidia, the company has a number of other tailwinds.

During the past several months, Nvidia has invested billions of dollars into opportunities across the AI infrastructure stack.

- 10 stocks we like better than Nvidia ›

With a market capitalization hovering near $5.5 trillion, Nvidia (NASDAQ: NVDA) stands as the most valuable company in the world. Nearly all of the optimism surrounding the company traces back to its thriving data center operation, where GPUs power the world's most advanced artificial intelligence (AI) models. In my eyes, the company's upside is far from exhausted.

While data center revenue will continue its explosive climb amid a capital expenditure supercycle, Nvidia is quietly transforming itself from a chip designer into a more diversified architect of the entire AI infrastructure stack. Targeted investments are the keys to securing the physical, optical, and wireless foundations that will scale AI to gigawatt factories and edge networks alike.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Nvidia.

Expect data center momentum to continue

During the next couple of years, I fully expect data centers to remain Nvidia's primary growth vector. Demand for accelerated computing is showing no signs of slowing down as hyperscalers deploy ever-larger chip clusters for training, inference, and now agentic AI.

As models grow more parameter-heavy due to more sophisticated applications, marginal returns on each successive GPU architecture rise. Networking revenue is poised to compound the hardware trend. This is all to say that data center buildouts are not merely firing on all cylinders; they are being supercharged by the infrastructure Nvidia helps build.

From chipmaker to full-blown AI architect

Nvidia's capital allocation strategy suggests the company is making deliberate moves upstream and downstream in the AI value chain. The company's multibillion-dollar investments are not passive bets. Rather, these moves are being made to help lock in supply, accelerate adoption, and open new addressable markets.

For instance, Nvidia's recent $2 billion stake in CoreWeave directly funds the build-out of more than 5 gigawatts of AI factories by 2030. In return, CoreWeave will deploy Nvidia's GPUs, Vera CPUs, BlueField storage systems, and networking equipment -- creating a virtuous loop of guaranteed demand.

As electrical interconnects consume more power and reach their physical limits, photonics is becoming essential for moving data at blistering speed and lower energy draw. Nvidia addressed these concerns by making two separate $2 billion commitments in Lumentum and Coherent.

By co-investing in manufacturing, Nvidia embeds itself deeper into the nuts and bolts of AI factories -- boosting attach rates and potentially securing premium pricing for complete optical-ready platforms.

In addition, the company's $1 billion investment in Nokia extends Nvidia's reach to the wireless edge. Through the partnership, Nvidia's accelerated computing platforms are integrated into Nokia's radio access networks (RAN) to build AI-native 5G-Advanced and 6G deployments. This opens a huge opportunity in telecommunications infrastructure, positioning cell towers as distributed AI compute nodes for edge inference and the Internet of Things (IoT).

Collectively, these moves position Nvidia as an end-to-end AI platform provider of chips, interconnects, storage, cloud orchestration, and wireless intelligence. Taken together, these investments de-risk Nvidia's data center ecosystem and pull forward demand across the entire infrastructure stack.

Where could Nvidia stock trade by 2028?

Nvidia currently sports a forward price-to-earnings (P/E) ratio of roughly 26. By 2028, I think investors are likely to apply more of a premium as the company demonstrates diversified infrastructure leadership.

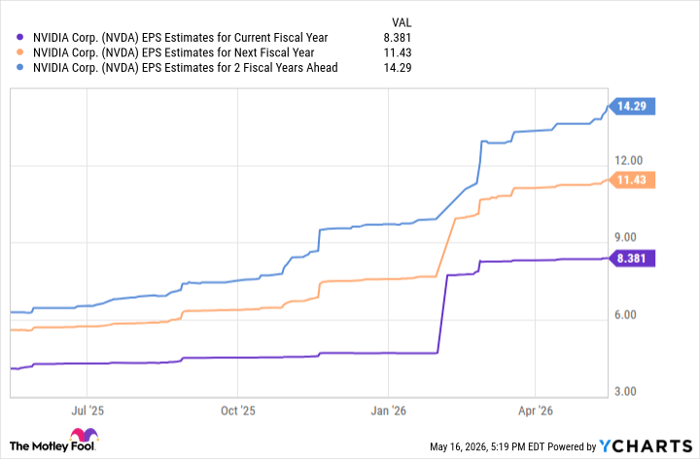

If Nvidia's forward P/E expands to 30, the stock could reach about $430 based on 2028 estimated EPS. That implies a market capitalization of roughly $10.5 trillion, or about double where Nvidia trades today.

NVDA EPS Estimates for Current Fiscal Year data by YCharts

Nvidia's infrastructure investments are quietly strengthening the company's competitive edge. As AI spending shifts from niche experiments to enterprise deployment, the company is positioned to capture disproportionate value compared to peers.

By the end of 2028, I do not think Nvidia will be valued solely on the basis of being the GPU king. I predict the company will be priced as an indispensable platform powering the AI economy.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $469,293!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,381,332!*

Now, it’s worth noting Stock Advisor’s total average return is 993% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 19, 2026.

Adam Spatacco has positions in Nvidia. The Motley Fool has positions in and recommends Coherent, Lumentum, and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles