Abel Era Debut: Berkshire Returns to Airline Stocks in First Quarter, What Signal Does It Send?

TradingKey - Berkshire Hathaway ( BRK.A) ( BRK.B) has officially kicked off the "Abel Era" with a quarterly holdings report featuring significant portfolio rebalancing.

A 13F regulatory filing submitted Friday ET shows that in the first full quarter after Greg Abel succeeded Warren Buffett as CEO on January 1, 2026, the investment giant executed its most aggressive structural adjustment to its portfolio in recent years.

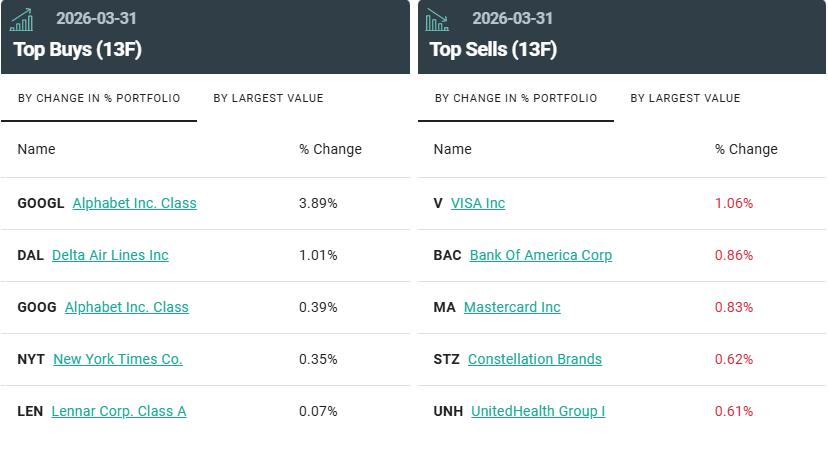

The most market-watched move was Berkshire establishing a new position in Delta Air Lines ( DAL) worth approximately $2.65 billion, while slightly increasing its stake in Macy's ( M ). This marks Berkshire's first bet back on the airline sector since it liquidated its holdings in the four major U.S. carriers during the 2020 pandemic.

Meanwhile, Berkshire further increased its holdings in Google's parent company, Alphabet ( GOOGL ), signaling its continued optimism regarding the long-term competitiveness of digital advertising and cloud infrastructure.

While adding to positions, Berkshire aggressively trimmed non-core assets; filings show the company liquidated its positions in Amazon ( AMZN) and UnitedHealth Group ( UNH) in their entirety, and significantly reduced its stakes in payment giant Visa ( V) and Mastercard ( MA ), while also selling a large block of shares in insurance broker Aon ( AON ).

The reduction in Chevron was the largest single transaction in this holdings report. Berkshire sold 45.78 million shares of Chevron at an average price of $182.59 per share in the first quarter, cashing out approximately $8 billion and reducing its position by 35%. With a remaining stake of 4.2%, it remains the fourth-largest shareholder. The timing of this reduction was precise—Chevron's stock hit an all-time high in March this year due to the U.S.-Iran conflict and surging oil prices, allowing Berkshire to successfully lock in gains at the peak.

In the first quarter, Berkshire purchased $16 billion in stocks and sold $24 billion, resulting in net sales of $8 billion, as its cash reserve climbed further to a record high of $397.38 billion. Ample cash flow provides the new management team with flexibility in positioning; Abel emphasized that "patience and discipline are core strengths" as they wait for more attractive investment opportunities.

Berkshire Hathaway Bets Big on Delta Air Lines

In the first investment scorecard led by new CEO Greg Abel, the move most sensitive to market nerves is undoubtedly the company’s return to airline stocks after a six-year hiatus—spending approximately $2.65 billion to build a position of 39.8 million shares in Delta Air Lines, accounting for about 1% of Berkshire's portfolio and instantly becoming its 14th largest holding.

The uniqueness of this move lies in its historical context.

Throughout the Oracle of Omaha’s investment career, the airline industry was once a "value trap" he avoided at all costs. In his 1996 shareholder letter, he quoted Richard Branson’s joke, saying, "If you want to be a millionaire, start with a billion dollars and launch a new airline." In 2007, he further quipped that a far-sighted capitalist should have shot down the Wright brothers at Kitty Hawk, and he even joked about setting up an "800-number" to call whenever he felt the urge to buy airline stocks.

In his view, the airline industry is characterized by capital intensity, powerful labor unions, and stringent regulation, with core resources largely controlled by governments and an economic moat that is virtually non-existent.

Buffett’s first foray into the sector was in 1989 with US Airways (AAL) preferred stock, which was followed by four consecutive years of losses and a suspension of dividends; although he eventually recovered his principal by sheer luck, he later characterized it as a "sloppy, unforced error."

In 2016, he entered the sector a second time, betting on the logic of capacity discipline following industry consolidation. He held stakes in the "Big Four" carriers and was once Delta's largest shareholder, but he liquidated all positions amid the 2020 pandemic, admitting that "the business model for the airline industry has changed fundamentally" and expressing a reluctance to continue subsidizing cash-burning enterprises.

Now, in this third entry led by Abel, Berkshire has chosen only Delta Air Lines, a departure from the diversified approach of 2016.

Markets have interpreted this as an optimistic signal from the new management regarding the recovery of U.S. consumer spending and business travel. Delta’s differentiated strategy of focusing on premium customer segments has allowed it to remain competitive despite high fuel costs. With its stock price up 1.75% year-to-date, this may be the key reason Berkshire selected it exclusively.

Following the announcement, Delta’s shares surged in after-hours trading, while also sparking market speculation. Given its scale, the $2.6 billion investment is a small fraction of Berkshire’s approximately $400 billion cash reserve, raising questions about whether it will further increase its exposure to the airline sector.

After all, how to efficiently deploy such massive cash reserves is the core challenge facing new chief Greg Abel, and this trade—which breaks a Buffett investment taboo—may just be the beginning of a stylistic shift in Berkshire’s "post-Oracle era."

Berkshire Hathaway’s Top 10 Holdings

As of the end of March 2026, the overall composition of Berkshire Hathaway's top ten holdings remained stable, with core assets such as Apple, American Express, and Coca-Cola continuing to hold dominant positions, though individual rankings saw minor adjustments, with Google's parent company Alphabet seeing the most significant rise in position.

According to the latest 13F regulatory filing, Berkshire's top ten holdings at the end of the first quarter were as follows:

- Apple ( AAPL) remained firmly in first place

- American Express ( AXP) ranked second

- Coca-Cola ( KO) jumped from fourth in the fourth quarter to third

- Bank of America ( BAC) fell from third to fourth

- Chevron ( CVX) maintained its fifth position

- Occidental Petroleum ( OXY) rose from seventh to sixth

- Alphabet ( GOOGL) climbed significantly from tenth to seventh

- Chubb ( CB) ranked eighth

- Moody's ( MCO) dropped from sixth to ninth

- Kraft Heinz ( KHC) slipped slightly from ninth to tenth

From the perspective of position weighting, the three major holdings—Apple, American Express, and Bank of America—collectively still account for more than 50% of the equity portfolio, highlighting the continuity of Berkshire's "long-term holding of core assets" strategy.

However, compared to the relatively static portfolio management of the Buffett era, the new management team has increased both the frequency of quarterly rebalancing and the extent of structural adjustments.

Recommended Articles