Fed Meeting Minutes Preview: What Signals to Watch For?

TradingKey - The Federal Reserve is scheduled to release the minutes of the April FOMC meeting on May 21. This will be the first set of minutes in 2026 not presided over by Jerome Powell. On May 15, Kevin Warsh officially took office as the 17th Chair of the Federal Reserve, with the leadership transition occurring precisely between the conclusion of the meeting and the release of the minutes.

Given the combination of policy continuity and the leadership transition, the density of signals these minutes send to the market may far exceed that of a routine report. The April FOMC voted 8-4 to maintain interest rates, marking the greatest internal dissent since October 1992.

Furthermore, the minutes may for the first time explicitly disclose whether discussions regarding the removal of "easing bias" language have entered the formal agenda, a move that several voting members strongly advocated for at the time.

April Federal Reserve Interest Rate Decision

On April 30, the Federal Reserve decided to maintain the target range for the federal funds rate at 3.50% to 3.75%, marking the third consecutive pause in rate cuts since December 2025. In its statement, the Fed listed three variables supporting its decision to "stand pat": developments in the Middle East, persistent high inflation, and sluggish employment growth.

However, the policy's vulnerability lies in the fact that this policy meeting was held at the end of April, before the April CPI data had been released.

Data released on May 12 confirmed the concerns of senior officials: April CPI growth accelerated to 3.8% year-on-year from 3.3% in March, while core CPI rose 2.8% year-on-year; PPI increased 6.0% year-on-year, the largest jump since 2022. Energy prices contributed approximately 0.4 percentage points to the gain. Manufacturing costs are facing significant pressure; if these continue to pass through to end-users, the final channel for rate cuts will be further blocked.

The labor market also demonstrated better-than-expected resilience. Nonfarm payrolls increased by 115,000 in April, far exceeding the market forecast of 62,000, while the unemployment rate remained at 4.3%. A deep-seated contradiction exists between the employment structure and inflationary pressures: job growth in the service sector continues to rise steadily, and the risk of a "wage-price" spiral has not yet been truly resolved.

May Policy Meeting Minutes

The market's focus lies on whether existing disagreements will be suppressed or validated following the release of these minutes. Simultaneously, the market is re-anchoring based on the signals released by this meeting.

First, whether the boundaries of inflation tolerance have been formally revised. How the minutes characterize inflation persistence—as a transitory factor or as having more enduring traits—will directly determine long-term expectations for the interest rate anchor.

Second, the extent of the discussion regarding "removing the easing bias." Three dissenting members had explicitly requested the removal of this wording; whether the minutes disclose details of the discussion on this proposal will serve as a yardstick for the committee's overall hawkish tilt.

Third, how the impact of Warsh's appointment on policy transmission is integrated into the outlook. During his Senate confirmation hearing, Warsh explicitly advocated for rate cuts, proposed trimmed-mean inflation as the primary metric, and argued for de-emphasizing reliance on the dot plot and forward guidance.

On the other hand, Warsh previously stated that balance sheet reduction is a long-term project, diverging from the path of accelerated QT during the Powell era. Whether the minutes contain implicit discussions regarding the balance sheet also warrants close attention.

Market pricing for the probability of a rate cut has fallen to near zero; a rate hike is no longer a black swan event.

Futures markets have almost entirely priced out any possibility of interest rate cuts in 2026.

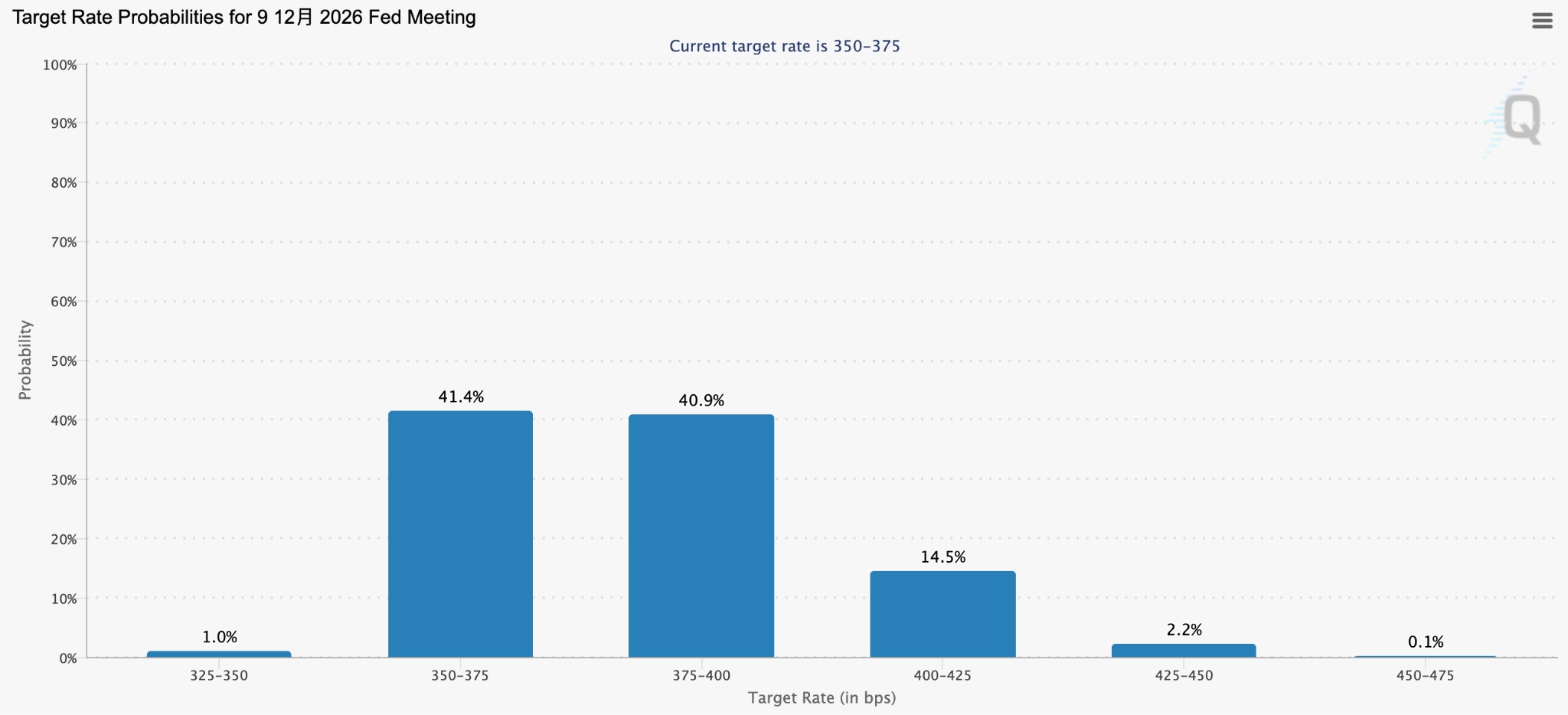

According to CME FedWatch data, as of May 19, the probability of traders pricing in a December rate hike has exceeded 50%, and the probability of a January hike has risen to 58%. On the Polymarket prediction market, the trading price of contracts for a 2026 Fed rate hike has surged to 34% from the 10% to 12% range in April.

[The probability of traders pricing in a December rate hike has exceeded 50%, Source: Cmegroup.com]

It should be noted that, recently, when Trump was asked in an interview whether Warsh would still cut rates, he offered a rare response, saying, 'I would let him do as he sees fit.' As the White House's suppression of rate hikes is fully loosened, the force truly constraining the market has shifted from political pressure to the inflation data itself.

Recommended Articles