CrowdStrike Holdings Inc Stock (CRWD) Moved Up by 3.33% on May 18: A Full Analysis

CrowdStrike Holdings Inc (CRWD) moved up by 3.33%. The Software & IT Services sector is up by 1.03%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Alphabet Inc Class A (GOOGL) up 1.26%; Microsoft Corp (MSFT) down 0.23%; Alphabet Inc Class C (GOOG) up 1.25%.

What is driving CrowdStrike Holdings Inc (CRWD)’s stock price up today?

The upward movement in CrowdStrike's stock today appears to be significantly driven by positive analyst sentiment and continued strong demand for its cybersecurity offerings, particularly those leveraging artificial intelligence. KeyBanc Capital Markets raised its price target for CRWD to $700 from $525, while maintaining an Overweight rating. This upward revision reflects a positive outlook on increased cybersecurity spending, fueled by the company's recent "Mythos" conference and its leadership in critical security areas such as cloud security, vulnerability management, and services. This follows other recent price target increases from firms like BTIG and Mizuho, indicating a growing consensus among analysts regarding the company's strong prospects.

The optimism stems from CrowdStrike's robust product innovation, especially within its AI-powered Falcon platform. The company recently unveiled its Falcon Platform Spring '26 Release, introducing advancements to secure AI across endpoints, SaaS environments, and cloud workloads. These innovations address emerging attack surfaces by focusing on AI agent discovery, governance, and real-time protection against AI-accelerated threats and data exposure risks. This strategic focus aligns with the broader cybersecurity industry trend, where the chaotic rise of agentic AI and an accelerating threat landscape are driving increased investment in advanced security solutions. CrowdStrike's recognition as Frost & Sullivan's 2026 Company of the Year for Identity Threat Detection and Response further validates its leadership in addressing critical enterprise security needs.

Furthermore, the company's solid financial performance and outlook contribute to the positive market perception. CrowdStrike reported robust revenue growth in fiscal year 2026, alongside a healthy gross profit margin. While first-quarter fiscal year 2027 results are anticipated in early June, the company had previously provided fiscal year 2027 revenue and first-quarter revenue guidance that exceeded analyst consensus, underscoring ongoing momentum and strong adoption of its cloud-native security platform. This combination of strong analyst confidence, innovative AI-driven product development, and a favorable market environment in the cybersecurity sector appears to be driving the stock's positive performance today.

Technical Analysis of CrowdStrike Holdings Inc (CRWD)

Technically, CrowdStrike Holdings Inc (CRWD) shows a MACD (12,26,9) value of [27.97], indicating a buy signal. The RSI at 82.57 suggests overbought condition and the Williams %R at -2.52 suggests oversold condition. Please monitor closely.

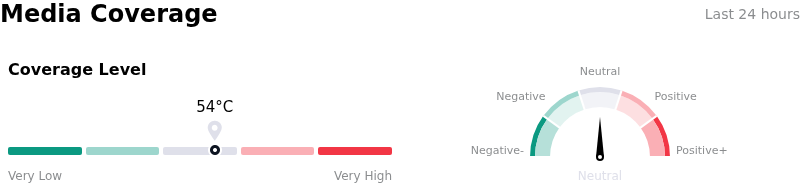

Media Coverage of CrowdStrike Holdings Inc (CRWD)

In terms of media coverage, CrowdStrike Holdings Inc (CRWD) shows a coverage score of 54, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of CrowdStrike Holdings Inc (CRWD)

CrowdStrike Holdings Inc (CRWD) is in the Software & IT Services industry. Its latest annual revenue is $4.81B, ranking 68 in the industry. The net profit is $-162.50M, ranking 545 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $488.93, a high of $706.00, and a low of $185.00.

More details about CrowdStrike Holdings Inc (CRWD)

Company Specific Risks:

- The stock is exhibiting technically overbought conditions with a high Relative Strength Index (RSI) and trades near its 52-week high, making it susceptible to profit-taking and potential consolidation.

- Recent channel checks indicate mixed signals and potential softness in core endpoint product seat counts, suggesting underlying operational challenges in a foundational revenue stream.

- The company continues to report negative GAAP operating margins, which are worsening, alongside intensifying competition from rivals such as Palo Alto Networks, posing a financial and market share risk.

- There are ongoing reputational and potential regulatory concerns stemming from the July 2024 global IT outage, which highlighted concentration risk among third-party cybersecurity providers.

Recommended Articles