TSMC Q3 Earnings Preview: Record Revenue Is a Lock, but an Upgraded Outlook Could Be the Real Catalyst

TradingKey - Global semiconductor foundry leader Taiwan Semiconductor Manufacturing Company (TSMC, TSM) will report its Q3 2025 earnings on Thursday, October 16, before U.S. markets open. With record-breaking revenue already confirmed by monthly reports, analysts expect record profits and double-digit EPS growth, as all eyes will be on whether the company raises its full-year guidance — the key catalyst for shares.

Q3 Results: A New High Is Guaranteed

Based on preliminary data, TSMC’s Q3 performance is already historic:

September revenue: NT$330.98 billion (+31.4% YoY), the strongest September ever

Q3 total revenue: NT$989.918 billion (~$324.7B USD), up ~30% YoY — exceeding both market expectations and TSMC’s own forecast

Now, with full financials coming, analysts project:

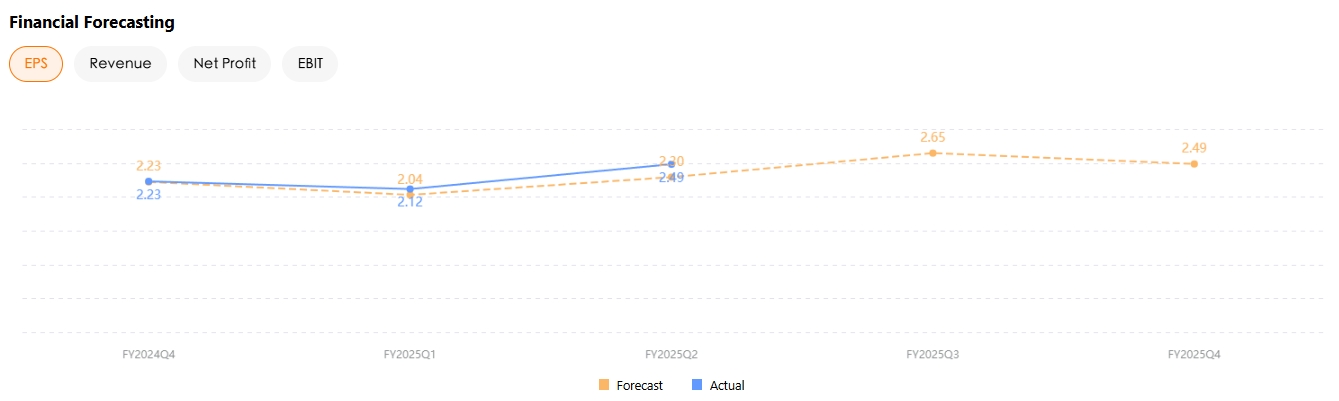

Revenue(LSEG) | $32.0B USD | +36.6% |

Net Profit | $13.55B USD | ~+28% |

EPS | $2.65 | +35.9% |

TSMC EPS Forecast, Source: TradingKey, LSEG

Zacks estimates slightly lower:

Revenue: $31.5B USD (+34%), below TSMC’s $31.8–33.0B guidance

EPS: $2.59 (+33.5%)

Any profit figure above NT$398.3 billion would mark TSMC’s highest quarterly net income ever and seven consecutive quarters of profit growth.

The Real Focus: Will Guidance Be Raised Again?

While strong results are priced in, the biggest upside driver will be whether TSMC raises its full-year revenue outlook — as it did in Q2, when it increased its annual USD-denominated revenue growth target from a mid-20% range to around 30%.

Morgan Stanley said that if TSMC raises its full-year guidance again due to strong AI demand, the stock will go up. They recommend adding exposure ahead of the report.

Citi expects ongoing AI-driven momentum could push TSMC’s revenue above even the upgraded 30% target.

Morgan Stanley forecasts:

Full-year revenue growth raised to 32–34%

Capital expenditure guidance slightly trimmed to ~$40B

In a bullish scenario: 35%+ revenue growth, potentially driving 3–5% stock upside

Mario Morales, VP at IDC, projects 30–35% annual revenue growth for 2025, noting:

“I am expecting that TSMC will continue to outperform its peers given the ongoing exponential growth of AI infrastructure investments and that the leading chip suppliers such as Nvidia and AMD have only one place to go - TSMC.”

Why TSMC Keeps Winning

TSMC’s dominance is built on:

Leadership in 3nm and 7nm process technology

Strong profitability from 5nm node

Ongoing R&D in 2nm and beyond

Expanding footprint in high-performance computing (HPC) and smartphones

It is also a key beneficiary of recent AI deals between OpenAI, Nvidia, and AMD — all of which rely on TSMC to manufacture their most advanced chips.

Stock Outlook: More Room to Run?

As of October 13, TSMC’s U.S.-listed shares (TSM) are up over 53% YTD, outperforming Nvidia’s 40% gain.

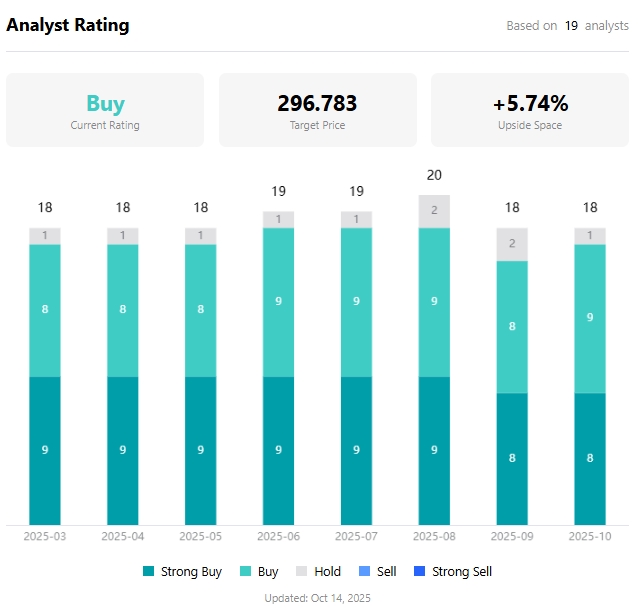

According to TradingKey, the Wall Street consensus target price is $296.78, implying about 6% upside from current levels.

Average Price Target for TSMC Stock, Source: TradingKey

Despite repeated record highs, some investors remain cautious due to risks from U.S. tariffs and broader concerns over an AI bubble.

But Morales argues that even with trade tensions, AI infrastructure remains a strategic land grab for cloud providers, manufacturers, and enterprises.

Recent analyst updates reflect growing confidence:

Barclays: Raised target from $325 → $330

BofA Securities: Set target at $330

Susquehanna: Bullish case target of $400

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.