Software Bear Market: 2 Monster Artificial Intelligence (AI) Stocks With up to 70% Upside to Buy Now, According to Wall Street

Key Points

Anthropic recently released a new suite of AI models targeting the enterprise software industry.

While some businesses are vulnerable to Anthropic's innovations, not all AI software platforms face this risk.

Specialized data analytics providers and cloud services platforms remain poised for robust AI-driven growth.

- 10 stocks we like better than Palantir Technologies ›

In late January, artificial intelligence (AI) start-up Anthropic released a suite of new plug-ins for its large language model (LLM) Claude, aimed at the enterprise software industry. Following the release of the Claude Cowork ecosystem, software stocks have been plummeting.

While the broader technology sector has lagged 4.5% so far this year, the application software and software infrastructure industries have fallen more dramatically -- declining by 21% and 14%, respectively.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

The ongoing sell-off in software stocks has been dubbed the "SaaSpocalypse" by analysts on Wall Street. While most are hitting the panic button and running for the hills, smart investors understand that times like these often feature rare opportunities to buy the dip in otherwise high-performing businesses.

Let's explore two AI software stocks poised for monster growth over the next several years -- despite Claude's intentions to dethrone these industry leaders.

Image source: The Motley Fool.

1. Palantir Technologies

Since OpenAI publicly launched ChatGPT in late November 2022, shares of data mining specialist Palantir Technologies (NASDAQ: PLTR) have surged by 1,900%. The catalyst behind Palantir's meteoric rise is the company's Artificial Intelligence Platform (AIP) -- a comprehensive software fabric stitched together by the company's core platforms Foundry, Gotham, and Apollo.

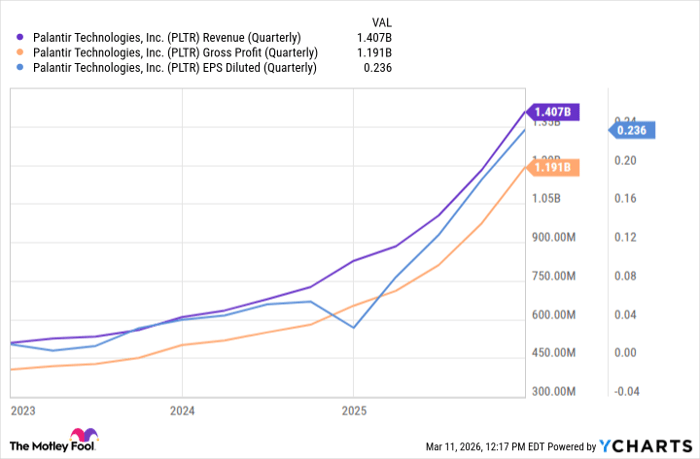

Ever since the company debuted AIP, Palantir's growth has been bonkers. While revenue growth is surging well over 50% year over year, the more impressive feature is the company's ability to command strong profit margins in parallel with accelerating sales.

Data by YCharts.

In the world of enterprise software, it's incredibly difficult to differentiate product lines. Said differently, companies that develop customer relationship management (CRM), enterprise resource planning (ERP), capital budgeting, or cybersecurity products are often at risk of being seen as commoditized, given the competitive landscape.

Palantir is different. The company specializes in making ontologies -- or detailed architectures of a company's anatomy, tracing granular data flows across the enterprise in real time. This specialty is incredibly difficult to replicate. Given these dynamics, Palantir doesn't have much in the way of direct competition.

Against this backdrop, Palantir is able to generate such robust growth across its top and bottom lines due to its pricing power and ability to maintain low churn rates. Nevertheless, the company's shares have declined 16% year to date -- now trading near its cheapest levels since the summer. With that said, Tyler Radke of Citigroup rates Palantir a strong buy -- placing a price target of $260 on the stock, or about 70% upside from current trading levels.

Considering Palantir boasts $4.4 billion of remaining deal value just in its U.S. commercial segment, combined with the pace at which it's onboarding customers -- closing 325 deals just in the fourth quarter -- I think the company remains in a strong position to benefit from AI-driven tailwinds over the next several years.

2. Amazon

Despite reporting impressive financial results for the fourth quarter and full year 2025, the share price of Amazon (NASDAQ: AMZN) has been cratering over the last month. The culprit behind the sell-off revolves around Amazon's capital expenditure (capex) budget for 2026. Management's guidance for $200 billion in capex far exceeded Wall Street's expectations.

Rotating capital away from Amazon due to its rising infrastructure spend seems backwards. Over the last few years, Amazon has poured billions into data centers, custom training and inference chips, as well as strategic investments in AI start-ups -- namely, Anthropic.

Amazon made its initial investment in Anthropic in September 2023. The thesis behind this partnership was to integrate Anthropic's generative AI models into Amazon Web Services (AWS). By the end of 2023, AWS was operating at a $97 billion annual revenue run rate and boasted 30% operating margins. Fast forward to the fourth quarter of 2025 -- where AWS achieved a $142 billion annual revenue run rate and increased operating margins to 35%.

Not only has Anthropic's integration into the AWS ecosystem propelled sales, but Amazon is becoming more efficient from a profitability standpoint, as well. Considering AWS accounts for the majority of Amazon's profit, the company's close ties with Anthropic should be viewed as nothing short of a strategic asset. With this in mind, smart investors are supporting the company's decision to double down on its AI infrastructure roadmap.

As of this writing (March 11), Robert Sanderson of Loop Capital Markets has the highest share price target for Amazon at $360 -- representing roughly 70% upside from its current price. That said, Sanderson hasn't issued a report since November.

Numerous analysts have issued more recent reports with price targets in the range of $300 to $325. This suggests that Wall Street remains largely bullish on Amazon's long-term potential despite some near-term pressure.

Should you buy stock in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $514,000!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,105,029!*

Now, it’s worth noting Stock Advisor’s total average return is 930% — a market-crushing outperformance compared to 187% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 16, 2026.

Citigroup is an advertising partner of Motley Fool Money. Adam Spatacco has positions in Amazon and Palantir Technologies. The Motley Fool has positions in and recommends Amazon and Palantir Technologies. The Motley Fool has a disclosure policy.

Recommended Articles