Walmart Q3 Earnings Preview: The 'Defensive Buy' Amid Economic Headwinds and Market Turmoil

TradingKey - Walmart (WMT), the largest U.S. retailer, is scheduled to report its fiscal third-quarter 2026 earnings, for the period ending October, before the U.S. market opens on Thursday, November 20. Despite facing headwinds from tariff policies and weakening U.S. consumer vitality, Walmart has demonstrated greater resilience than its retail peers, bolstered by its low-price model, leadership in groceries, and expanding e-commerce business.

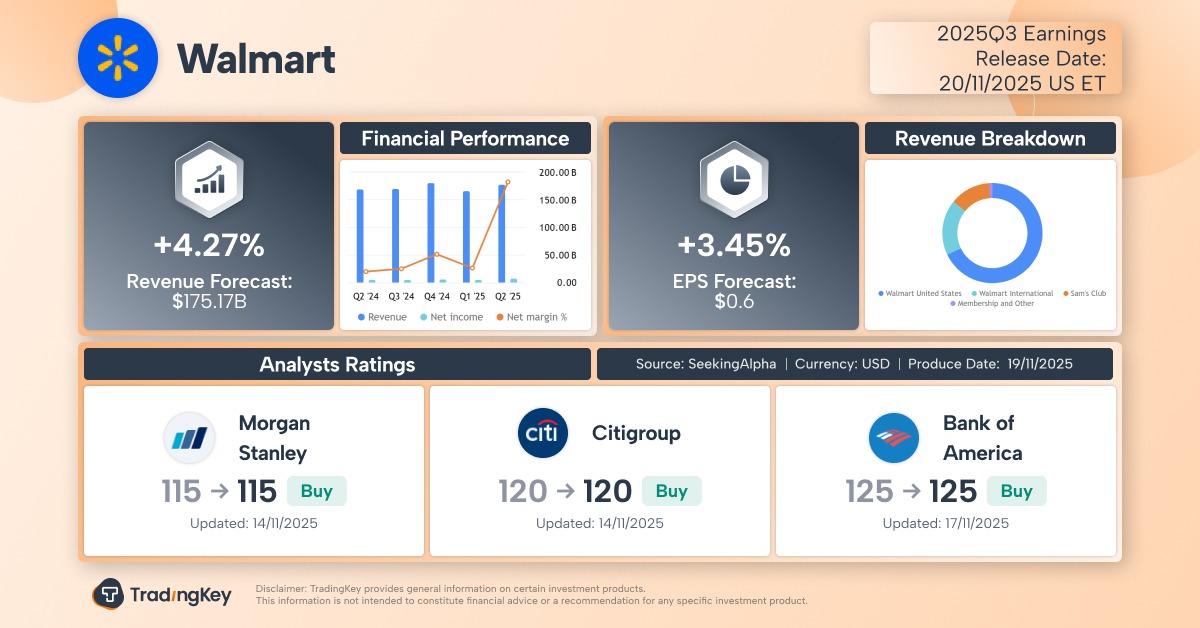

According to Seeking Alpha, analysts anticipate Walmart's revenue for the fiscal third quarter of 2026 (roughly equivalent to Q3 2025) to increase by 4.27% year-over-year (YoY) to $175.17 billion. Earnings Per Share (EPS) are projected to grow 3.45% YoY to $0.60.

This consensus revenue growth forecast aligns with Walmart's steady 3% to 5% growth trend over the past year. Walmart has recorded at least 20 consecutive quarters of YoY revenue growth, while competitors like Target, Kroger, and Lowe's have seen inconsistent revenue during the same period.

In the second fiscal quarter, Walmart's Q2 revenue surpassed analyst expectations, driven by a healthy 4.6% comparable store sales growth in its largest segment, Walmart U.S., and robust 26% growth in e-commerce sales.

Furthermore, despite anticipating tariff-related pressure on costs and pricing in the second half of the year, Walmart still raised its full-year sales guidance.

A Fortunate Few Amid Tariff Impacts

Walmart is widely regarded as a "barometer of the U.S. economy." Its earnings reports offer insights into the resilience of American consumer activity, and conversely, other indicators of U.S. consumer health can provide advance signals about the retail giant's financial performance.

Walmart's enduring position in the U.S. retail market is largely due to its low-price strategy, extensive customer base, strong supply chain management capabilities, and logistics automation.

These advantages are particularly salient amidst Trump tariffs and signs of slowing consumer activity. The company not only retains its low-income consumer base (e.g., stable demand for groceries) but also attracts more middle-income and even high-income shoppers seeking to economize.

This counter-cyclical appeal and multi-tier customer coverage make Walmart more "defensive" when economic pressures mount.

During its Q2 earnings release, Walmart disclosed that it has taken various measures to maintain its low-price advantage. However, certain product categories remain challenging to fully absorb, with some goods seeing price increases over the summer as tariff-affected costs continue to rise.

Optimistically, there has been no significant change in customer spending at Walmart, and its U.S. stores have gained market share across all income demographics, with particularly strong growth among higher-income households.

Recent signals, such as the decline in the University of Michigan Consumer Sentiment Index and Home Depot's downward revision of its fiscal year 2025 outlook, indicate that U.S. consumer activity has been impacted by tariff policies, inflation, and other factors.

For the third quarter, by absorbing a significant portion of tariff costs to capture market share, Walmart is likely to remain one of the few retailers to achieve positive growth amidst economic headwinds. Even as the impact of tariffs gradually diminishes, Walmart is expected to continue leading the retail sector with consistent growth.

New CEO, Stronger Growth Prospects for Walmart?

Last week, Walmart announced that current CEO Doug McMillon will retire at the end of January next year, with John Furner, the current president of its U.S. operations, taking over as CEO in February. McMillon, 59, has been with Walmart for four decades, and under his eleven-year leadership, Walmart's stock price has quadrupled.

The change in Walmart's leadership did not cause the dramatic stock price fluctuations seen in some other companies. This is because incoming CEO Furner is a veteran involved in Walmart's transformation, having led merchandising, operations, and sourcing teams.

Crucially, Furner has pledged to steer Walmart into a "new era of retail driven by innovation and AI," a prospect eagerly anticipated by investors—as evidenced by the continuous expansion of its e-commerce business and market reactions following its e-commerce partnership with OpenAI.

Walmart notes that it anticipates another wave of significant, AI-driven transformation in business and retail, and Furner possesses the unique ability to guide the company through this period of change.

Bank of America stated that this management change underscores Walmart's confidence in its strong market position and current business momentum, adding that no substantial changes to the company's strategy are expected.

Walmart Stock: Resilient Against Economic Weakness and Market Downturns

Since late October, U.S. major stock indices have experienced a painful period, albeit not a "bloodbath," due to shifts in tech stock valuations and interest rate policy expectations.

The S&P 500 Index has fallen over 3% since November, and Nvidia's stock is down 10%, yet Walmart's stock has edged up 0.21%, outperforming Costco (-1.80%), Target (-3.32%), and Lowe's (-7.79%) during the same period.

According to TradingKey's stock scoring tool, Wall Street analysts' consensus price target for Walmart is $113.67, implying a 12% upside from the latest closing price of $101.39.

While concerns exist regarding Walmart's relatively high price-to-earnings (P/E) ratio, which stands at 40.08 compared to the industry average of 15.70, its "both offensive and defensive" stock remains attractive amid market volatility and economic downturns.

Analysis suggests that Walmart's resilience stems from prudent inventory management offsetting tariff impacts, the inimitable nature of its low-price business model, its adaptability to evolving consumer behaviors and digitalization, and strong cash flow supporting operational sustainability and dividend longevity.

Research indicates that Walmart's stock outperformed the S&P 500 during four major market downturns in the 1990s, 2000s, 2008, and 2020s, highlighting its appeal as a defensive stock during periods of market fragility.

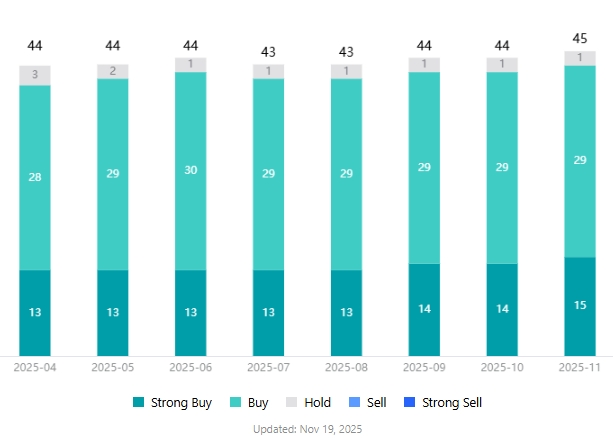

Therefore, in the current market environment, Walmart, which can maintain its pricing advantage, is likely to be more resilient to downturns. This is a significant reason why none of the 66 analysts covering Walmart's stock have issued a "sell" rating.

Walmart Analyst Ratings, Source: TradingKey

Recommended Articles