Tesla’s Megapack Leads the Surge in Energy Storage Stocks

TradingKey - Long an afterthought in the U.S. energy system, grid-scale battery storage is rapidly moving from the margins to the mainstream.

Driven by plunging costs, AI-era data center demand, and rising renewable penetration, storage is quickly becoming one of the core solutions not just for grid stability—but for America’s broader energy transition.

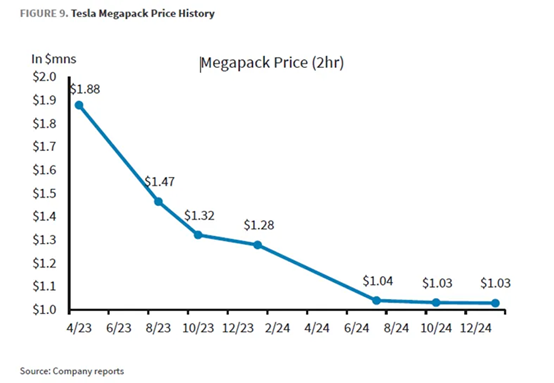

Cleanview data shows U.S. utility-scale battery capacity has grown nearly 15x since 2020. And the clearest near-term catalyst? Price. Since 2022, lithium-ion battery costs have dropped roughly 40%, vastly improving project economics and cutting the payback timeline for most installations.

Solar + Storage: The Fastest, Most Flexible Answer—For Now

Structural changes in electricity demand are playing a huge role here.

As AI, cloud computing, and high-performance workloads surge, data center power usage has pushed peak load curves higher and added real pressure on grid flexibility. But new firm generation hasn’t kept up.

Combined-cycle gas turbines (CCGTs) remain the transitional workhorse—but with typical construction cycles of 3 years or more, real output doesn’t come online until 2027 at the earliest.

Nuclear is further behind. While the Trump administration signed an executive order this May targeting 400 GW of U.S. nuclear capacity by 2050, the math gets tricky: with 4–6 years for permitting and another 6–8 years for construction, there’s little chance of meaningful new output before 2030.

The near-term answer is Hybrid solar + storage. These projects can be deployed in 12–18 months, scale modularly, and plug in where grid reinforcement lags. The combo is fast, flexible, and financeable—helping meet short-term supply gaps at a fraction of the timeline.

Since 2020, average electricity prices across the U.S. have climbed over 18%—due to inflation, supply tightness, and demand spikes. But adding baseload capacity isn’t fast enough to flatten those rates. Large-scale solar and battery deployments are becoming key tools in stabilizing supply and limiting pricing risk.

Moreover, as renewables are inherently intermittent and variable, battery storage is increasingly being used not just passively—but actively. Batteries are now playing a material role in load shifting, demand smoothing, frequency response, and real-time power balancing. As grid planners look to meet surging summer loads and drive flexible margins for new data centers, storage is no longer optional. It’s fast becoming a must-have.

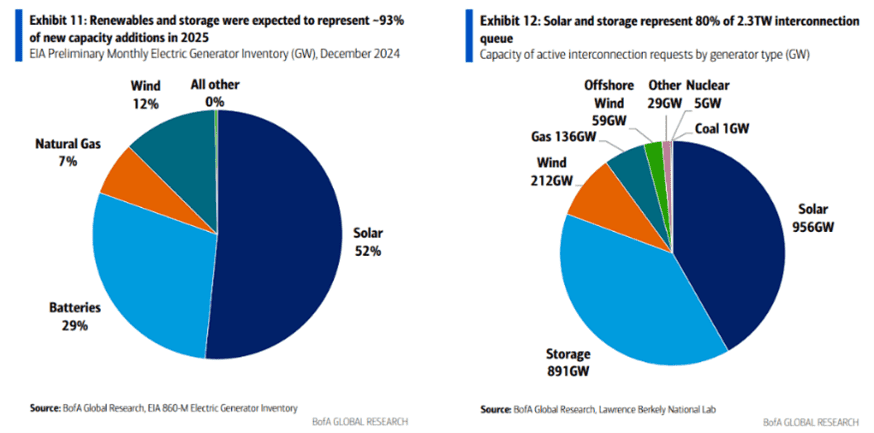

Bank of America’s grid interconnection queue data confirms this shift: as of now, there are 891 GW of battery storage projects awaiting grid connection—nearly on par with solar (956 GW), and well ahead of wind (212 GW) or gas (136 GW).

The signal is sharp: solar + storage is the new foundation of U.S. energy buildout.

Tesla Megapack: The Clear Front-Runner in Utility-Scale Deployment

No one has ridden the wave harder—or faster—than Tesla (TSLA).

In H1 2025 alone, Tesla deployed 20 GWh of energy storage—up 48% YoY. Q3 deployments jumped again, hitting 12.5 GWh and showing no signs of slowing.

Tesla’s Megapack is designed for the grid itself: a fully integrated, utility-scale system combining battery cells, power conversion systems (PCS), thermal management, and inverters—all in one modular container.

It’s built for speed, cost control, and plug-and-play scalability.

New factories are reinforcing that flexibility. Tesla’s new Shanghai energy storage facility has begun initial output, adding capacity beside its U.S.-based plants. Combined with local sourcing and improving cost curves for iron phosphate cathodes (LFP), Tesla is successfully pushing unit cost down—even as volumes ramp.

And the product is evolving.

On Thursday, according to the Wall Street Journal, Baird analysts highlighted Tesla’s new Megapack 4, which integrates directly with distribution infrastructure—bypassing the need for substation connection altogether. That could significantly expand Tesla’s addressable market, especially in underserved or remote zones.

Vistra: The Multi-Fuel Operator Gaining AI-Driven Market Share

Another major storage player navigating the AI era is Vistra (VST).

From its Moss Landing site in California—now one of the largest battery installations in the world—Vistra is combining large-scale batteries with highly responsive gas peakers to serve the kind of elasticity that cloud-scale clients increasingly demand.

Unlike traditional generators that only trade in wholesale markets, Vistra sells directly to end customers—from industrials to residential users—building a more stable revenue base. That retail-linked flexibility matters in today’s volatile load environment.

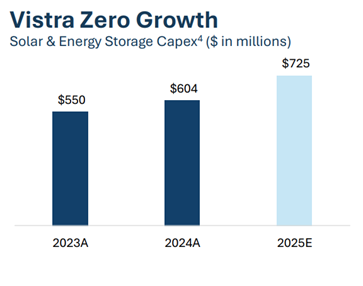

Early in Q3, the company announced a new $725 million investment in solar and battery projects for 2025—underscoring its intent to remain a controlling force in the U.S. clean energy transition.

GE Vernova: Building Storage into Grid-Aware Energy Systems

GE Vernova (GEV), meanwhile, is leaning into integrated energy solutions—combining gas turbines, battery systems, and digital grid platforms into unified deployments.

Rather than just selling equipment, GEV positions its offering as “intelligent operations”—using software to deliver automated peak shaving, voltage stabilization, and real-time network optimization for high-load clients like data centers.

That model—generation plus storage, wrapped in a control layer—is increasingly what hyperscale clients are asking for. In the long arc of AI-related energy demand, platforms like GEV’s could offer a defensible edge.

The Landscape: Technology, Platforms, and Supply Chains Now Moving in Sync

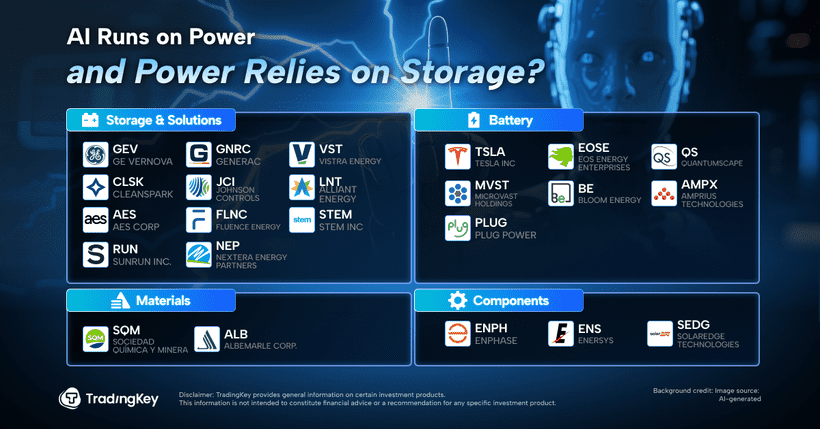

As batteries move from feature to foundation, companies are locking into strategic positions across three key verticals:

Battery Manufacturing & Hardware:

- Tesla (TSLA) – full-scale range from home (Powerwall) to grid (Megapack)

- Eos Energy (EOSE) – utility-grade zinc-based long-duration storage

- QuantumScape (QS) – commercializing solid-state lithium metal batteries

- Microvast (MVST) – diversifying into commercial and industrial formats

- Bloom Energy (BE) – deploying SOFC-based distributed energy systems

- Amprius Tech (AMPX) – silicon-anode batteries with high energy density

- Plug Power (PLUG) – hydrogen generation and storage infrastructure

Energy Management & Integration Platforms:

- GE Vernova (GEV) – integrated turbine + battery + software systems

- Vistra (VST) – fast-reacting gas + battery hybrids targeting hyperscalers

- CleanSpark (CLSK) – microgrid and localized storage infrastructure

- Generac (GNRC) – residential to mid-scale C&I storage (e.g. PWRcell)

- Johnson Controls (JCI) – grid-aware building systems with storage

- Alliant Energy (LNT) – utility-scale renewables and emerging storage

- AES (AES) – global leader in utility batteries and VPPs

- Fluence Energy (FLNC) – Siemens-AES joint venture, software + storage at scale

- Stem Inc. (STEM) – AI-powered energy scheduling via the Athena platform

- Sunrun (RUN) – solar + home battery bundle for energy independence

- NextEra Energy Partners (NEP) – multi-state grid-tied battery portfolios

Materials & Component Suppliers:

- SQM – key lithium production

- Albemarle (ALB) – one of the largest global lithium extractors

- Enphase (ENPH) – smart inverters + advanced home storage systems

- EnerSys (ENS) – large-format battery deployments for industrial use

- SolarEdge (SEDG) – solar+storage inverters and grid-managing devices

Recommended Articles