What to Expect From Microsoft Q4 FY2025 Earnings: The King of AI Monetization — A $4 Trillion Market Cap Within Reach?

TradingKey - Cloud giant Microsoft (MSFT.US) will report its fiscal fourth-quarter 2025 earnings (calendar Q2) after the U.S. market close on July 30. Wall Street is bullish, expecting strong results from Azure cloud services and AI-driven growth to propel Microsoft’s market capitalization toward the $4 trillion milestone.

According to Visible Alpha, analysts forecast:

- Revenue: $73.86 billion, up 14% YoY

- Net income: $25.27 billion, up 15% YoY

- EPS: $3.38, up from $2.95 in the same quarter last year

Like Meta, Microsoft has consistently outperformed expectations, indicating that analysts have repeatedly underestimated the impact of AI on its business.

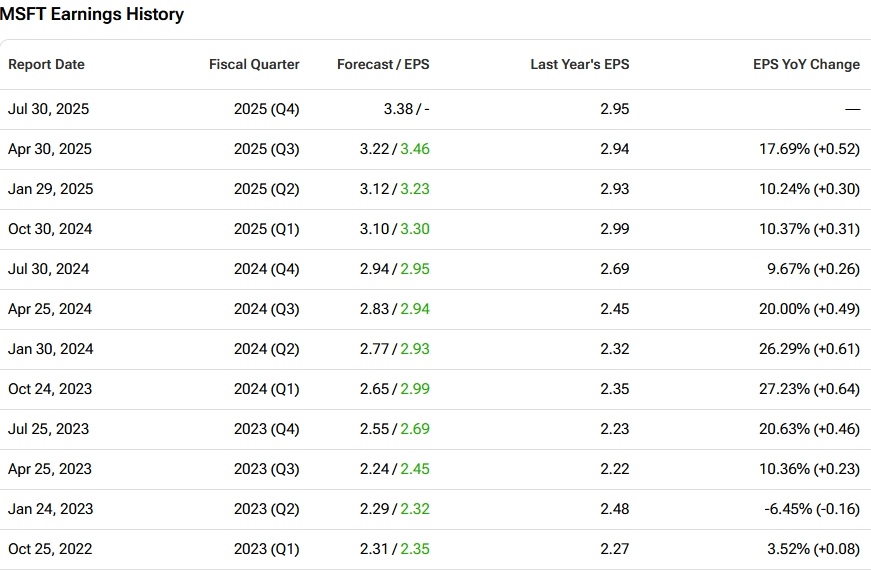

Tipranks data shows that Microsoft has beaten EPS forecasts for 11 consecutive quarters since Q1 FY2023, with nine straight quarters of year-over-year EPS growth — underscoring its execution strength and financial resilience.

Microsoft Earnings Per Share History, Source: Tipranks

Azure Poised for Double-Digit Growth

Microsoft’s three core business segments — and their Q3 revenue contributions — are:

- Intelligent Cloud (Azure, GitHub, etc.): 43%

- Productivity & Business Processes (Office, Microsoft 365, etc.): 38%

- More Personal Computing (Windows, Xbox, etc.): 19%

Analysts expect the Intelligent Cloud segment to grow 22% YoY, maintaining strong momentum after a 33% surge in Q3 — though below Microsoft’s earlier guidance of 34–35%.

BofA Securities believes Azure’s growth is driven by:

- Continued enterprise cloud migration

- Leadership in security and data analytics

- A total addressable market expanding at 35.5% annually

CEO Satya Nadella previously highlighted a four-layer acceleration in cloud demand:

- Migration of traditional workloads (e.g., Windows Server, SQL Server) to the cloud

- Rising demand for digital services like Cosmos DB and Fabric

- Healthy growth in non-AI compute and storage driving cloud-native expansion

- AI co-pilot effects, including infrastructure demand from OpenAI

TradingKey analyst Petar Petrov noted that Azure has been gaining market share from Amazon's AWS and Google Cloud, with both AI and non-AI cloud segments performing strongly.

Copilot: More Than Just a Plugin

In its second-largest segment, Productivity & Business Processes, Petrov expects low double-digit growth despite tariff and macro headwinds — driven by rising adoption of Copilot and higher revenue per user.

Nadella has said:

“AI-first copilots in every layer of the tech stack.”

Analysts argue that this statement is more profound than it appears: Copilot is not just a feature — it’s a new architectural layer for distributed semantic computing that can be monetized across platforms.

According to a Morgan Stanley CIO survey in Q2, IT budgets are expected to grow in 2025, with software spending up 3.6%, and Microsoft tools remaining central to core enterprise spending.

The Only Company That Has Truly Monetized AI at Scale

Some analysts now view Microsoft as the only global tech giant to turn AI into an industrial engine, with deep integration across infrastructure (Azure), Software (Copilot, Microsoft 365) and operations (Copilot Studio, GitHub Copilot).

No other company has achieved this level of vertical integration or revenue diversification in AI.

By combining Azure’s cloud scale, Copilot’s user penetration, and continuous infrastructure investment, Microsoft is converting AI adoption into multiple revenue streams — from enterprise subscriptions to usage-based AI pricing.

Morgan Stanley said that Microsoft’s AI innovation cycle is just beginning — the company has ample runway for growth.

Is Microsoft Overvalued?

Year-to-date in 2025, Microsoft shares are up 21.61%, significantly outperforming the S&P 500 (+8.32%). The stock has hit repeated all-time highs in July, raising concerns about stretched valuations.

Currently, Microsoft trades at a P/E ratio of 39, above Amazon’s 37 and Google’s 20.

Petar Petrov noted that while expectations are high, a sudden spike in the stock is unlikely — but downside risk is limited due to strong fundamentals.

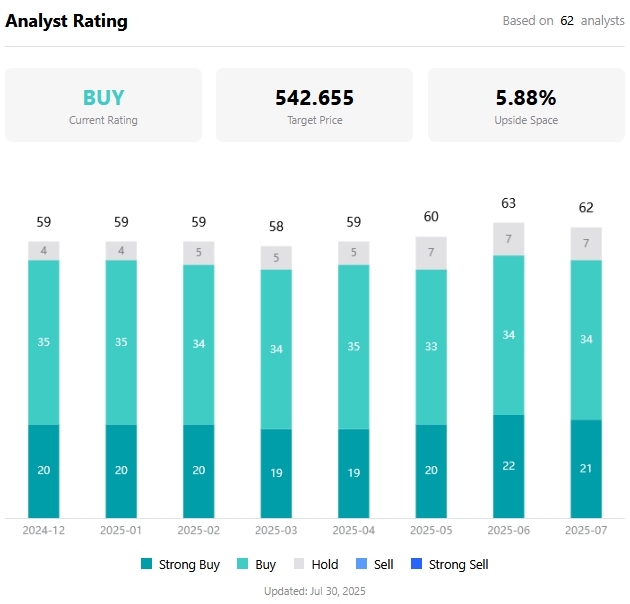

According to TradingKey, the average analyst price target is $542.66, implying 5.88% upside from current levels — putting Microsoft on track to reach a $4 trillion market cap.

Analyst Price Targets for Microsoft, Source: TradingKey

Notably, not a single analyst has issued a “Sell” rating on Microsoft stock — a rare consensus in today’s market.

Investors now expect more than just beats — they want proof that AI monetization is scalable and sustainable, not just a narrative.

In July, Microsoft announced its second major round of layoffs in 2025, cutting ~9,000 jobs — the largest since early 2023 — which UBS believes will boost future margins.

UBS raised its price target from $500 to $600, maintaining a Buy rating, citing Azure’s growth potential and cost discipline.

Citigroup increased its target from $605 to $613, naming Microsoft a top pick due to proven AI execution, high-quality business model, long-term pricing power and margin resilience.

Recommended Articles