Tesla Q2 Earnings Preview: A Pivotal Moment for Musk, EVs, and AI — Risk or Opportunity?

TradingKey - Tesla (TSLA), the world’s leading electric vehicle maker, will release its Q2 2025 earnings after U.S. markets close on Wednesday, July 23.

With headwinds from Elon Musk’s political activities, sluggish EV deliveries, and the Trump administration’s rollback of EV incentives, investors are bracing for Tesla to potentially report a third consecutive quarter of disappointing results.

What Markets Expect

Analysts forecast:

- Revenue of $22.79 billion, down 9% YoY

- Adjusted EPS of $0.43, down 20%

Tesla’s stock has fallen about 18% year-to-date in 2025, while the S&P 500 is up 7% and hitting new highs.

The company now sits at a critical juncture — with uncertainty around Musk’s leadership, vehicle demand, AI progress, and policy changes — leading to sharply divergent views on Wall Street.

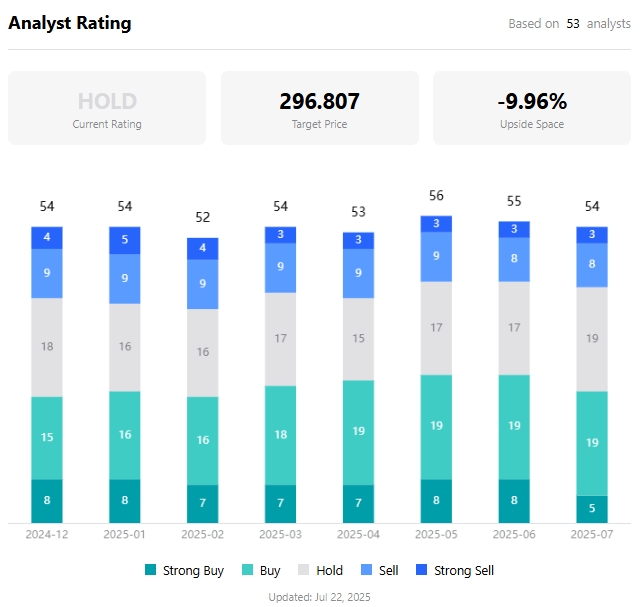

Target prices range from $115 to $500, reflecting deep disagreement over Tesla’s future.

Despite missing expectations in its last two quarters, Tesla’s stock still rallied — largely driven by Musk’s narrative around AI and autonomous vehicles. This time, investors will be watching closely to see if he can again use Robotaxi and AI ambitions to restore confidence.

Investing in Tesla = Investing in Elon Musk

More than any other public company, Tesla’s stock performance is tied to CEO Elon Musk’s personal actions.

For example, on June 5, when Musk publicly clashed with President Donald Trump, Tesla shares plunged 14%.

Earlier this year, Musk’s political involvement sparked backlash among consumers in Europe and North America, triggering calls for boycotts of Tesla vehicles and stock.

Although investor concerns eased slightly after Musk announced his return to full-time duties at Tesla, his recent plan to launch an “American Party ” has reignited fears of further distraction.

Last Saturday, Musk posted that he would resume working seven days a week and sleeping at the office — widely seen as an effort to rebuild trust with shareholders.

Weakness in the Auto Business

While Tesla’s AI and energy storage divisions have drawn attention in recent quarters, automotive sales remain its core revenue driver.

Tesla has reported year-over-year delivery declines in both Q1 and Q2 2025 :

- Q1 deliveries: 336,681 units (-13%)

- Q2 deliveries: 384,122 units (-13.5%)

After recording its first annual decline in vehicle deliveries since 2015 in 2024 (down 1.1% ), analysts expect another weak year in 2025, with deliveries projected to fall around 10% — due to Musk’s political profile, aging vehicle models, and intensifying competition.

JPMorgan warned that continued delivery weakness poses significant risks to Tesla’s full-year outlook and valuation. The firm assigned Tesla the lowest price target on Wall Street — $115.

Additionally, the Trump administration’s decision to eliminate EV tax credits and reduce regulatory credit incentives could further pressure profitability.

However, there are signs of hope. According to Wedbush’s latest report, Tesla’s China sales rose in June — the first increase in eight months. Analysts called China the “heart and lungs” of Tesla’s growth potential.

AI Still Holds Promise

Robotaxi remains a key focus for Tesla investors. Currently, Robotaxi operations are running in a limited capacity in Austin, Texas, with plans to expand to more cities.

While Musk continues to promote Robotaxi as a cornerstone of Tesla’s valuation, competitors like Waymo (Google’s parent Alphabet) currently hold a clear lead in commercial scale and operational maturity. Tesla’s Robotaxi program still faces technical hurdles and challenges to profitability.

To support its long-term valuation, Barclays analysts expect Musk to reiterate ambitious Robotaxi fleet expansion goals during the earnings call.

On the AI front, Tesla is leveraging cutting-edge technology from its xAI group across multiple businesses. Earlier this month, Tesla introduced the Grok AI assistant into its vehicles — a move seen as a step toward redefining human-car interaction and enhancing user experience.

Wide Divergence in Wall Street Outlook

Given the mix of weak fundamentals and optimism about Musk’s renewed focus, Wall Street’s price targets for Tesla vary dramatically:

- Wedbush: $500

- Morgan Stanley: $410

- Piper Sandler: $400

- Bernstein: $120

- JPMorgan: $115

According to TradingKey, the average analyst price target is $296.81 — implying roughly 10% downside from current levels.

Average Analyst Price Target for Tesla, Source: TradingKey

Recommended Articles