Micron’s AI Bet Pays Off

- Revenue reached $9.3 billion in Q3 2025, up 37% YoY, fueled by a 50% sequential rise in HBM sales.

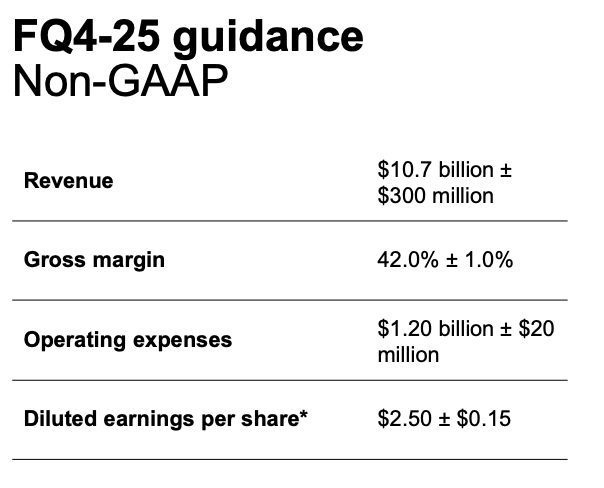

- Non-GAAP gross margin expanded to 39%, with Q4 guided at 42%, driven by premium pricing in AI-centric DRAM.

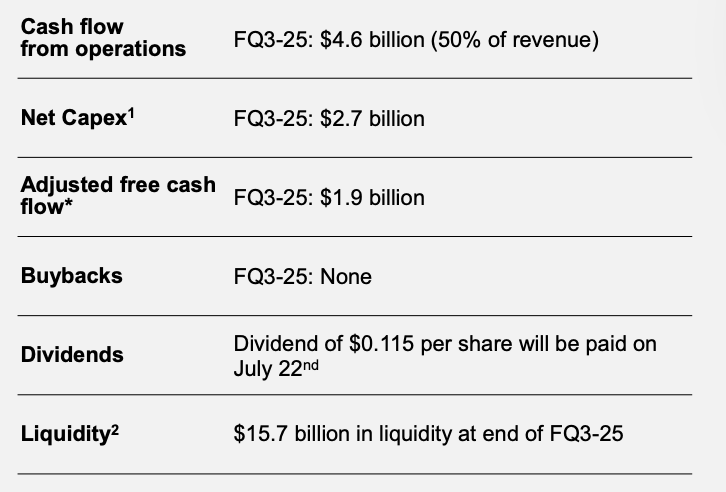

- Operating cash flow hit $4.6 billion, or 50% of revenue, with adjusted free cash flow margin at 21%.

- $14 billion FY25 capex focuses on HBM and advanced packaging, while net debt remains manageable with $12.2 billion in cash.

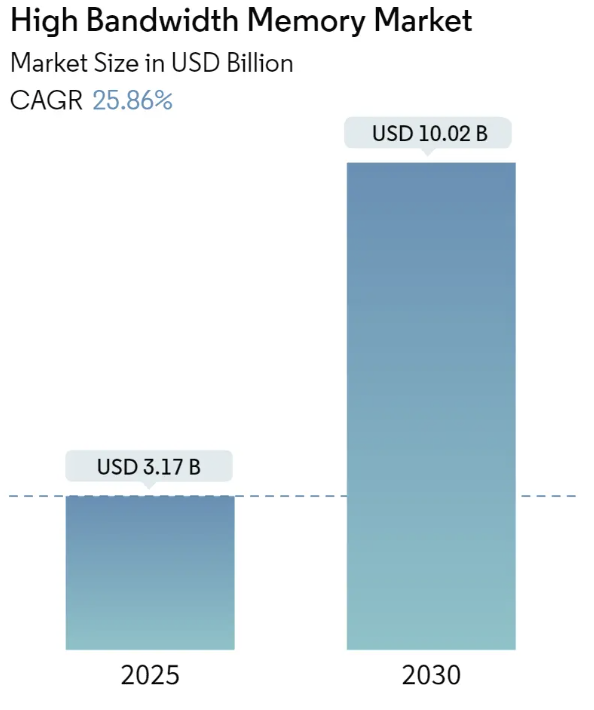

TradingKey - Q3 2025 was a turning point that most industry participants still don't comprehend. For decades, Micron (MU) lived and breathed a cyclical commodity-driven memory cycle, but recent trends suggest a structural shift towards becoming an AI infrastructure anchor. Revenue surged to a new high of $9.3 billion, a 37% year-over-year jump, driven by a nearly 50% sequential rise in high-bandwidth memory (HBM) revenues that power the generative AI explosion.

Source: Mordor Intelligence

Commentary from management, independently substantiated by the 10-Q and earnings deck, suggests that data center DRAM revenues have now consistently set new records, growing over double year-over-year, and consumer end-markets also bounced back on a sequential basis. This is not just an AI bubble tailwind, but this represents the earliest monetization of Micron's technological leadership in next-gen nodes, such as its 1-gamma DRAM, enabling 30% superior bit density and 20% lower power compared to older nodes.

Triangulating these figures with Micron’s historical record adjusted free cash flow of $1.95 billion and its 15% quarterly sequential revenue growth expectation to $10.7 billion during fiscal Q4, the narrative shifts from cyclical recovery to secular AI leverage. The earnings deck foresees HBM reaching parity with total DRAM share by end-calendar 2025 and thereby marking its transition from low-margin NAND exposure to high-margin, AI-driven DRAM.

Unlike commodity NAND, ASPs still fell high single digits sequentially; pricing power for HBM is revealed through such robust margins: non-GAAP gross margin expanded this quarter to 39% and forecast next quarter at 42%. This gross margin directionality, reverse-mapped with the capex discipline we can observe from the 10-Q ($2.66 billion net capex during Q3) and multi-billion-dollar Idaho and New York fabs on deck, tells us about a capital cycle perfectly aligned with an AI supercycle.

Designing a Moat: Technology Leadership and Control over the Value Chain

Underappreciated catalyst: Micron's transition from its historical commodity orientation toward a technologically defensible portfolio. The earnings deck details how Micron became the only volume producer of LP DRAM into data centers and took share in data center SSDs, becoming #2 worldwide.

Source: DRAM Market Size

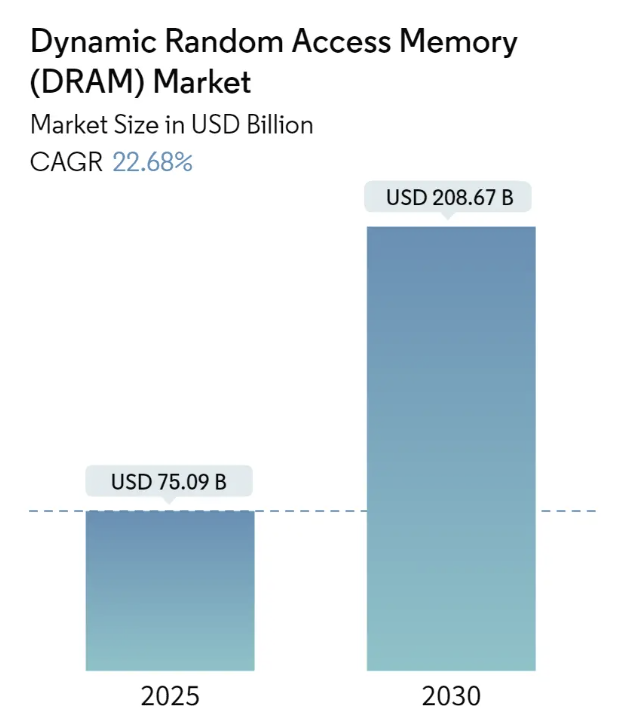

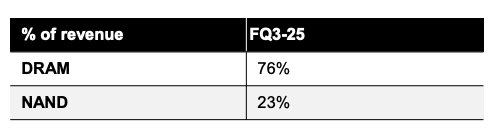

This is verified by third-party market share information mentioned in the earnings call and matching in revenue segmentation: DRAM accounted for 76% of sales this quarter, a mix shift that solidifies margins through cushioning commodity NAND volatility.

Source: Micron Financial Results FQ3 2025

Micron's node leadership is not a laughing matter. The 1-gamma DRAM ramp is also ahead of its earlier 1-beta schedule, a sign that EUV's adoption is worth its wait in volume and cost per bit. The plan to use this across its entire DRAM portfolio, from HBM for GPUs to LP DRAM for servers, creates economies of scale that competitors like SK Hynix and Samsung can't even remotely approximate, especially with Micron's vertically integrated HBM4 controller. Cross-referencing from the 10-Q, these nodes work their way through Micron's growing gross margins: cost reduction and favorable mix have sent operating income through the roof to $2.49 billion on a non-GAAP basis, more than double year-over-year.

Most notably, Micron’s geographic reshoring, sealed through its $200 billion U.S. investment strategy, is insulating supply chain disruptions historically crippling the memory market. This detailed capex plan, split between $150 billion spent on manufacturing and $50 billion on R&D, makes a play for securing supply security for homegrown AI initiatives, further supported through Idaho fabs and packaging facilities.

.png)

Source: Semiconductor Industry Association

This capital cycle limitation does matter: while the 10-Q shows debt load building towards $15 billion, there is $12.2 billion of cash on the books, net debt easily covered through robust operating cash flow of $4.61 billion this quarter. The long-term payoff is a supplier of memories less exposed to risk from geopolitics and more balanced with structural demand from AI.

Source: Micron Financial Results FQ3 2025

Breaking Through the Commodity Barrier: Profitability, Cash Flow, and AI Premium

The best validation for Micron’s shift in structure is the verification between its profitability growth and the timing of the capex cycle. Conventionally, participants in memory spent money at the least advantageous time, investing during oversupply and closing the ASP. However, 10-Q indicates Micron’s bit supply growth for non-HBM DRAM and NAND is intentionally less than industry growth demand, which is a sign that management is willing to forego low-margin commodity volume for the purpose of preserving pricing power for slots with high margin.

This is translating visibly. The earnings deck confirms that adjusted free cash flow margin hit 21% of revenue for Q3 and operating cash flow was $4.6 billion, 50% of revenue. With Q4-guided revenue at $10.7 billion and a 42% guide gross margin, Micron is already building memory products that not only generate a structural AI premium but deliver it sustainably. This is best explained when stress-testing HBM economics: HBM bit shipment grew roughly 50% sequentially, but ASPs for NAND fell in the high-single-digit percentage range. The contrast reveals that Micron’s pricing power from its premium is not in its commodity bits but in its HBM and LP DRAM.

Source: Micron Financial Results FQ3 2025

Triangulating this with its own FY25 capex plan of $14 billion, dedicated almost entirely to HBM scaling and advanced packaging, the capex-to-revenue ratio remains lean. While still sensitive to pricing volatility drags on free cash flow due to its sensitivity, positioning from a better-quality mix offsets this risk. Investors should note Micron does no buybacks this quarter but announced a minor dividend payout as evidence of management's preference for reinvesting over financial engineering. The company projects DRAM stocks going out of FY25 at tight levels, and therefore, the capital cycle is entirely suited to avoid losing out on the usual boom-bust destruction of shareholder value.

Valuation Update: Is Micron Still Undervalued?

The critical question for portfolio managers is whether this turnaround justifies a multiple expansion. The screenshot projects a forward P/E around 15x FY25 non-GAAP EPS, back-tested against peers like SK Hynix and Samsung, still worth Micron slightly above its AI leverage. The market does not recognize that adjusted EBITDA has spiked to $4.57 billion in the quarter, annualizing just shy of $18 billion. Fanning this back into a fair multiple and netting out net debt, fair value meets around $180 per share, corresponding to a good upside from today’s prices.

This is also evidence of free-cash-flow strength: Micron’s FCF trajectory, normalized for its fabs reinvestment, suggests FCF return will continue at high single-digit levels over the next two years, rare for a hardware component supplier. Though still, by market categorization, relegated to the commodity pot, its rebranding as an AI-associated memory backbone offers cause for re-rating. It’s also telling that the firm is forecasting record annual sales and profitability for fiscal 2025, and there’s no sign yet of oversupply, a rarity within an industry once prone to gyrating on pricing cycles.

The biggest risk, however, is execution on the HBM ramp and customer diversification. A single misstep on node yield or unforeseen changes in AI server demand can narrow down the premium pricing benefits. The balance sheet, however robust, is also more leveraged than in past cycles and inherits some risk from macro shocks. Tariff tensions flagged on the earnings deck are still a wild card but appear manageable given Micron’s robust U.S.-based capacity buildout.

Conclusion

Micron's quarter-to-quarter Q3 and strong Q4 guide is about more than cyclical recovery; it's a plausible pivot toward becoming a structural enabler of the AI data economy. Its moat has shifted from thin commodity cost leadership toward an integrated stack of next-gen nodes and high-end memory segments and selective capital allocation that ties its fate with the AI compute explosion. For justifiably dedicated investors, this is no Micron of the past. It's overdue for a re-rating with a fair value noticeably above current prices, but there's still a reminder needed about risk from HBM ramp-up execution.

Get started

Recommended Articles