Visa: The Payment Titan Conquering the Stablecoin Storm

Investment Thesis

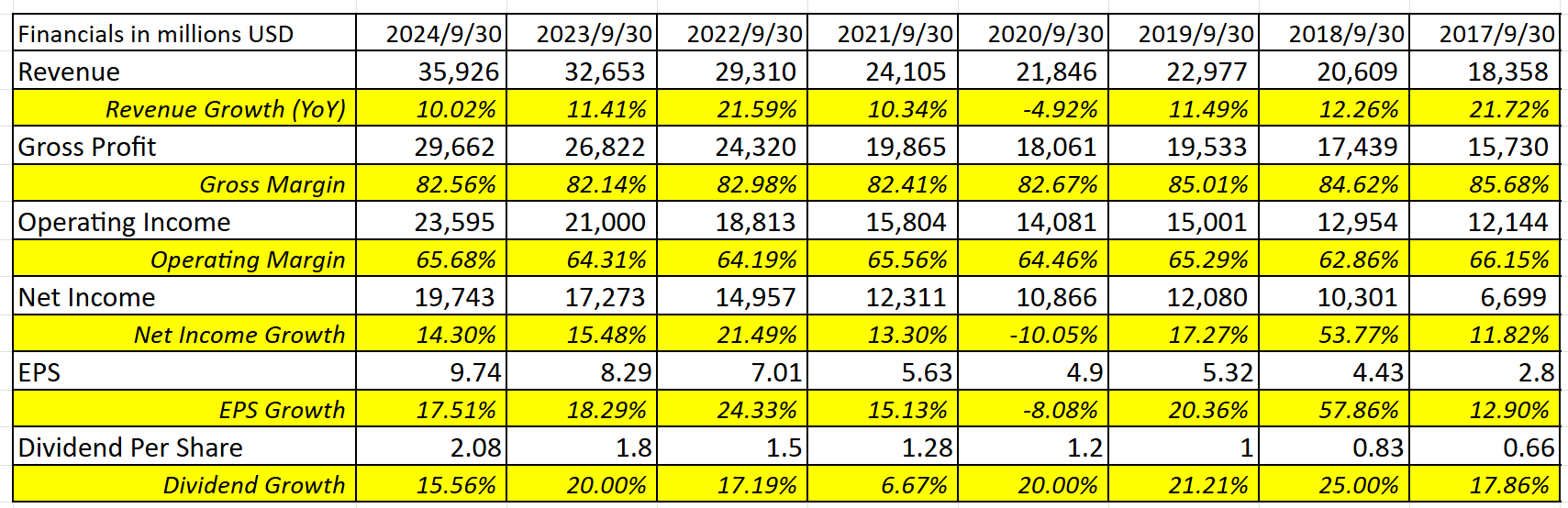

TradingKey - Visa, as a global leader in payment technology, leverages its robust VisaNet network and operations spanning over 200 countries, processing trillions of transactions annually, showcasing exceptional resilience and growth potential. In 2024, its earnings per share reached $9.74, up 17.51%, driven by steady increases in payment volume and cross-border transactions, alongside robust performance in value-added services and digital payments; despite competitive pressure from stablecoins like USDC and USDT, Visa transforms challenges into opportunities through piloting stablecoin settlements, optimizing cross-border payments, and integrating crypto ecosystems, with projected 2025 EPS of $11.55 and a target price of $347 (30x P/E). Its high profit margin (82.56% in 2024), stable cash flow (free cash flow yield of 3.4%-3.7%), and strategic moves (e.g., partnership with Coinbase) underpin its long-term value, though risks from stablecoin transaction diversion, regulatory pressures, and economic slowdowns warrant attention.

Source: TradingKey

Company Overview

Visa Inc., a global leader in payment technology, was founded in 1958 and is headquartered in San Francisco, USA. Its VisaNet global payment network connects consumers, merchants, financial institutions, and governments, providing secure and efficient electronic payment services for credit, debit, and prepaid cards. (For details, see the report: From Cash to Cards: Can Visa Keep Winning the Digital Payments Race?)

Operating in over 200 countries and regions, Visa processes billions of transactions annually. Its core strengths lie in advanced technical infrastructure and a vast global network, enabling near-real-time transaction authorization, settlement, and clearing with high security and reliability. Visa does not issue cards or provide loans but collaborates with banks, payment institutions, and tech companies to drive payment innovation through an open platform.

Visa’s Core Revenue Model

Visa's revenue model relies on its global payment network, driven by growth in transaction volume and frequency. Revenue sources include: service fees, charged to issuers based on total payment volume; data processing fees, based on transaction count for authorization, settlement, and clearing; international transaction fees, from cross-border or foreign currency transactions; and other revenue, such as licensing fees, technical support, and value-added services like Visa Direct. Customer incentives, tied to agreements with issuers, merchants, or partners, offset revenue to boost transaction volume and network usage, ensuring Visa's robust profitability in the global payment market.

Source: TradingKey, Visa

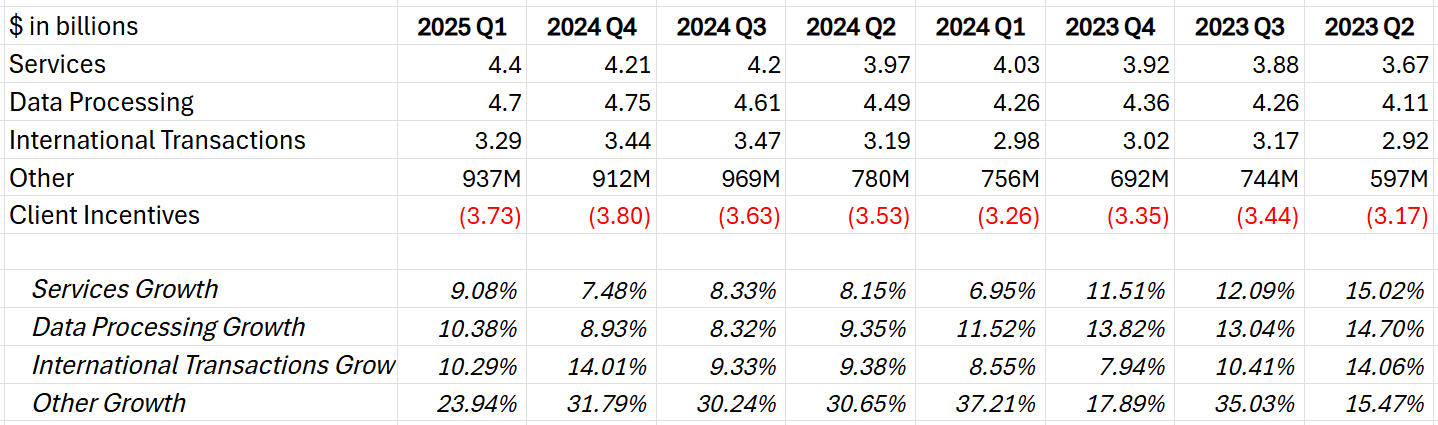

- Service Revenue

In the latest quarter, Visa's service revenue reached $4.4 billion, up 9% year-over-year, driven by an 8% increase in payment volume. Value-added services (VAS) revenue grew 22% to $2.6 billion, a significant portion of service revenue, mitigating payment volume fluctuations and enhancing revenue diversification. Visa's service revenue growth shows signs of rebound, with management optimistic about VAS, particularly in issuer solutions and consulting services, as a key growth driver. Demand for fraud protection and risk management services has risen due to increasing fraud and cybersecurity threats, expected to continue supporting long-term revenue growth.

- Data Processing Revenue

In the latest quarter, Visa’s data processing revenue hit $4.7 billion, up 10%, reflecting robust growth momentum. Specifically, processed transaction volume grew 9% to 60.7 billion transactions, with revenue growth slightly outpacing transaction volume, indicating that Visa has successfully boosted per-transaction revenue through enhanced security and risk management solutions, alongside optimized pricing strategies. Overall, data processing revenue, like service revenue, exhibits encouraging signs of renewed growth, a trend endorsed by management, who attribute future increases primarily to the strength of their pricing strategy.

- International Transaction Revenue

In the latest quarter, international transaction revenue reached $3.29 billion, up 10%, driven by strong growth in cross-border transaction volume, which rose 13%. Management expects cross-border volume to maintain steady growth, though currency fluctuations and specific transaction route impacts may persist, with relief anticipated to begin in May.

- Other Revenue

Other revenue totaled $937 million, up 24%, the fastest-growing category among the four, likely reflecting expansion into new businesses or services.

Source: TradingKey, Visa

Short-Term Impact of Stablecoin Development on Visa’s Stock

Recently, the impending U.S. stablecoin legislation (GENIUS Act) provides a clear regulatory framework for stablecoin issuance, allowing merchants to bypass traditional card payment systems and use stablecoins directly, causing a significant short-term impact on Visa's stock price. Amazon (AMZN), Walmart (WMT), Expedia (EXPE), and some airlines are exploring issuing proprietary stablecoins, while Stripe and Shopify have partnered to enable Shopify platform merchants to accept stablecoin payments. By issuing stablecoins, merchants divert cash and card transactions, saving substantial transaction fees, posing a challenge to traditional payment networks like Visa and potentially causing irreversible short-term negative impacts.

Mechanisms and Advantages of Stablecoins

Stablecoins are cryptocurrencies pegged to fiat currencies (e.g., the U.S. dollar), characterized by fast settlement, low fees, and high transparency. Leveraging blockchain technology, they enable peer-to-peer, decentralized value transfers with core advantages including:

- Low Transaction Costs: Stablecoin transaction fees are significantly lower than traditional credit card interchange fees, with USDC or Tether (USDT) transfers on blockchain networks costing just a few cents, or near zero on high-throughput networks like Solana or Polygon.

- Instant Settlement: Unlike credit card payments, which require days for clearing and settlement, stablecoins offer near-real-time fund transfers, typically completed in seconds to minutes.

- Cross-Border Payment Efficiency: Unconstrained by traditional banking system limitations (e.g., SWIFT delays and high fees), stablecoins enable low-cost, instant global payments.

- Decentralized Potential: Merchants can accept stablecoin payments directly, bypassing payment networks like Visa and bank intermediaries, reducing reliance on traditional infrastructure.

Potential Threats of Stablecoins to Visa

Stablecoins pose multifaceted challenges to Visa, particularly in the following key areas:

Risk of Transaction Volume Erosion: As major retailers like Walmart and Amazon explore issuing proprietary stablecoins, shifting some transactions to stablecoin payments could significantly reduce Visa’s transaction volume. In developing countries or regions with unstable local currencies, stablecoins’ low costs and ease of use attract unbanked users to transact via crypto wallets, bypassing Visa’s network. Visa’s long-term transaction growth has relied on the proliferation of digital payments, but the rise of stablecoins could undermine this foundation, especially in emerging markets.

Pressure on Cross-Border Payment Market Share: Visa’s cross-border payment business, a high-margin core driver, relies on elevated fees for revenue. However, stablecoins’ low-cost and instant settlement advantages excel in cross-border payments, potentially threatening Visa’s market share. As more businesses and individuals opt for stablecoins for cross-border transfers, Visa’s competitiveness in this lucrative segment could weaken.

Challenge from Enhanced Merchant Bargaining Power: Stablecoins empower merchants to accept digital currencies directly, strengthening their negotiating leverage. For instance, if Walmart issues a stablecoin and requires suppliers to accept it, Visa might be forced to lower transaction fees to retain market share, directly squeezing its revenue. Moreover, the decentralized nature of stablecoins could accelerate a “de-Visa-ization” trend, pushing merchants toward platforms like Coinbase Payments or Circle (USDC issuer) to build independent payment ecosystems, further eroding Visa’s industry standing.

Is Visa Facing a Doomsday Scenario?

Discussions about stablecoins potentially disrupting traditional payment systems are intensifying, but we believe this concern is overstated. Stablecoins do represent an innovative monetary channel, and with regulatory clarity emerging, industry investment in them is increasing. In the medium term, stablecoins have shown value potential in cross-border payments and specific use cases, but completely replacing mainstream networks like Visa remains unrealistic.

Firstly, even if a new payment network reduces merchant acceptance costs, it struggles to generate sufficient financial incentives to shift consumer payment habits and onboard them onto a new system. In other words, for stablecoins to gain widespread adoption, they need simultaneous buy-in from both merchants and consumers, a process that cannot happen overnight. Visa is not a traditional monetary channel but serves as an “authorization network,” with actual funds settled slowly via ACH or SWIFT. This distinction is nearly invisible to consumers—they only notice real-time reductions in their account balances or credit limits when using debit or credit cards. Despite slower backend settlement, Visa appears instant and efficient to consumers. In contrast, while stablecoins may offer faster settlement and lower merchant costs, they cannot significantly alter the consumer payment experience, making rapid replacement of Visa unlikely.

In addition, proprietary stablecoins face significant challenges in universality and interoperability, limiting their market adoption. For instance, a Walmart-issued stablecoin is unlikely to be accepted by Amazon, and an Expedia stablecoin would struggle to gain traction on Airbnb, reducing consumer incentive to use multiple stablecoins. Meanwhile, cost is not the sole factor in choosing a payment system. Building a successful payment network goes beyond channels and fees, requiring complex elements like rule-setting, security, dispute resolution, and continuous technological investment. For example, despite higher fees than debit cards and lower-cost alternatives like ACH transfers or RTP instant payments, credit cards dominate retail payments due to value-added services such as return protection, fraud prevention, and rewards programs—features that proprietary stablecoins currently cannot match. These advantages solidify the position of traditional networks like Visa, making them difficult to displace in the short term.

Visa’s Strategic Layout and Response

While we acknowledge the long-term possibility of bypassing Visa’s payment network, the company is not passively waiting but actively integrating into the stablecoin ecosystem to reinforce its leadership. Its response strategy spans multiple dimensions, reflecting forward-thinking planning:

Pilots and Expansion: Since 2023, Visa has piloted USDC for cross-border settlements, processing over $225 million in transactions, with plans to expand to more partners (e.g., Circle, BVNK), markets (e.g., Southeast Asia, Latin America), and blockchain networks (e.g., Solana, Polygon). Offering real-time settlement (within 10 seconds) and low fees (0.1%-0.5%), Visa effectively counters the decentralized threat of stablecoins, with projected transaction volume exceeding $1 billion by 2026, indicating significant growth potential.

Cross-Border Payment Innovation: By integrating USDC, Visa optimized its Visa Direct service, reducing cross-border settlement to seconds, handling $6 trillion in 2024. This 7x24-hour service covers 120 countries, collaborates with 60 financial institutions, and has processed $50 billion in stablecoin transactions. While positioning itself against Ripple and attracting e-commerce clients like Shopify, it faces fee competition pressures and reliance on external blockchains as challenges.

Card and Crypto Integration: Visa, in partnership with Bridge, Baanx, and Rain, launched stablecoin co-branded card programs, seamlessly blending stablecoins with traditional card payments to attract crypto users and counter competition from PayPal and Binance. Additionally, Visa collaborates with Coinbase, Binance, and Crypto.com, enabling users to buy USDC, USDT, and other stablecoins directly with Visa cards, further expanding its ecosystem reach.

Visa’s management is confident, viewing stablecoins as a vast opportunity to accelerate digital payment innovation. They position Visa’s global network as the critical bridge connecting the stablecoin ecosystem with traditional payment systems. Thus, we believe stablecoin development poses not a threat but a significant growth opportunity for Visa in the card payment solutions space.

Source: TradingKey, Visa

Earnings Forecast and Valuation Analysis

Despite potential competitive pressure from stablecoins, Visa’s strong business resilience and timely strategic adjustments can mitigate current market concerns to some extent. In the short term, we believe this competition will not materially impact Visa’s performance and may even provide a slight boost, though it could affect market sentiment toward the stock.

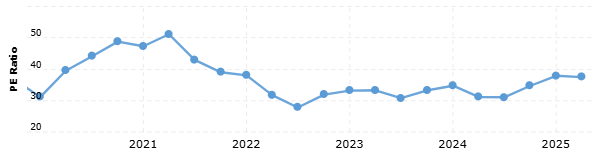

Based on 2024 earnings per share of $9.74, up 17.51%, driven by continued growth in global and cross-border payment volumes, as well as Visa’s expansion in value-added services, digital payments, and emerging markets, we project an EPS growth of 13%-15%. Optimistically, 2025 EPS could reach $11.55. With Visa’s high profit margin (82.56% in 2024), stable cash flow (free cash flow yield of 3.4%-3.7%), and historical P/E range (26.49-35x) reflecting a valuation premium, we consider a fair P/E of 30x reasonable. This translates to a target price of approximately $347 for Visa.

Source: macrotrends

Risks

- Stablecoin Competition: Stablecoins like USDC and USDT, with lower fees and faster settlement, may erode Visa’s market share in cross-border payments.

- Technological Disruption: Blockchain and decentralized finance (DeFi) platforms could bypass traditional payment networks, reducing Visa’s transaction volume.

- Economic Slowdown: Particularly in the U.S. and emerging markets, declining consumer spending could weaken transaction volume growth.

- Regulatory Pressure: Government-backed local payment systems (e.g., increasing UnionPay market share) introduce competition. Additionally, antitrust lawsuits create uncertainty, potentially impacting operations and profitability.

- Competitive Threats: Emerging “buy now, pay later” (BNPL) options threaten traditional card payments. The convenience and widespread adoption of mobile payments (e.g., Apple Pay, Google Pay) are eroding credit card market share.

Recommended Articles