[IN-DEPTH ANALYSIS] MercadoLibre: The Rise of Latin America's Digital Empire, Balancing Opportunities and Challenges

Investment Thesis

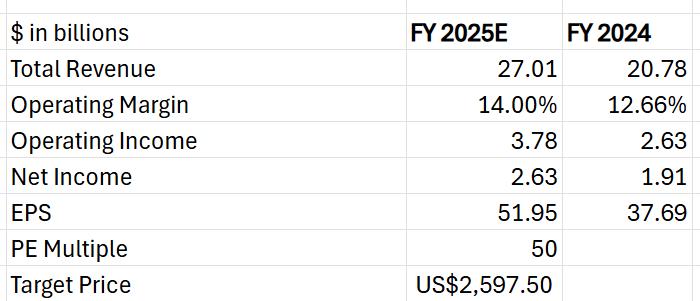

TradingKey - MercadoLibre is the leading e-commerce and fintech company in Latin America, deeply rooted in 19 countries and covering a young market of 670 million people. It leads the industry with its first-mover advantage and localized operation. The collaborative ecosystem of its e-commerce and Mercado Pago fintech business has driven the continuous increase in transaction volume and profit margin. The company predicts that the revenue CAGR from 2024 to 2034 will be 16%, but the economic recovery in Argentina, economies of scale in Brazil and Mexico, and high-margin fintech services may bring unexpected growth. The EPS for 2025 is expected to be $51.95. With a 50 times PE ratio, the target price is estimated to be $2,597.5. The valuation premium is supported by the low Internet penetration rate and the trend of digital transformation. Despite facing economic fluctuations, competition from Amazon and others, regulatory and logistics cost risks, MELI's unique model and market leadership position make it an excellent investment target in the digital wave in Latin America.

Source: TradingKey

Company Overview

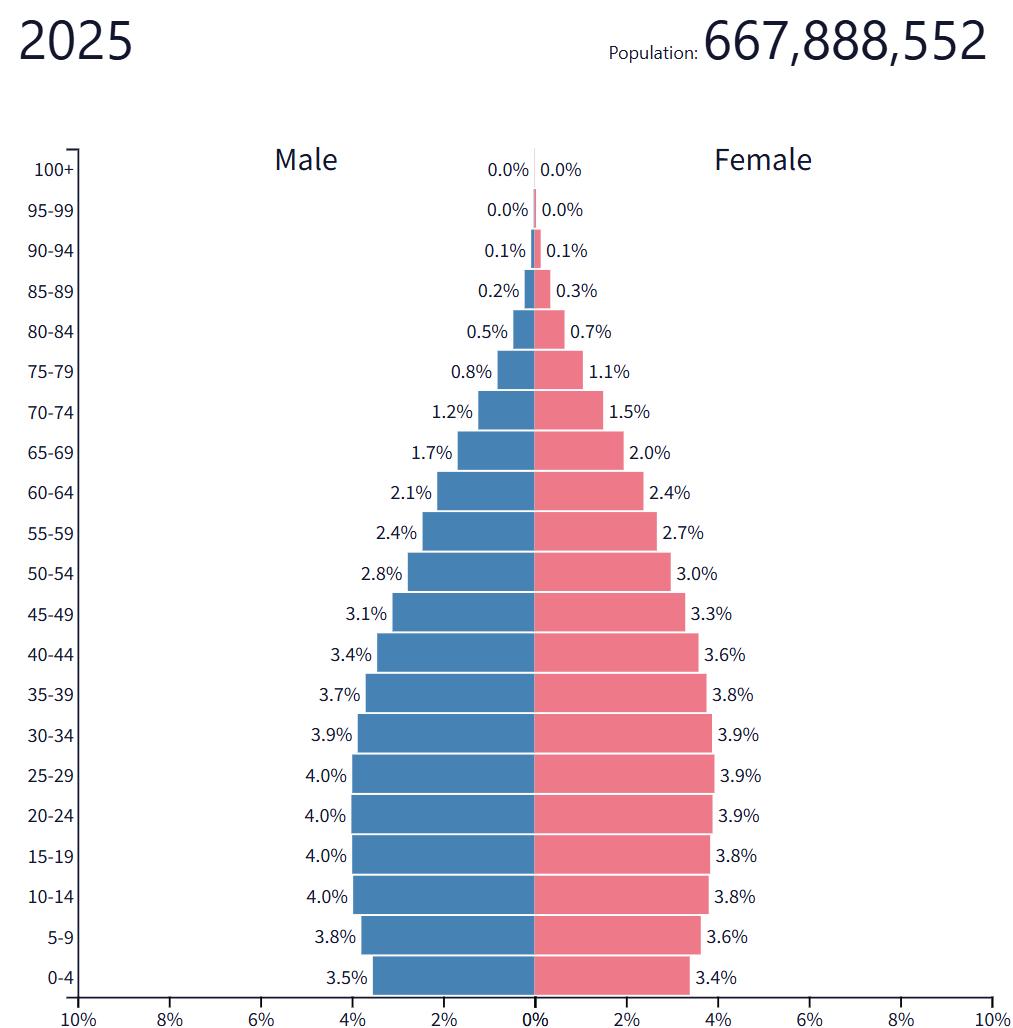

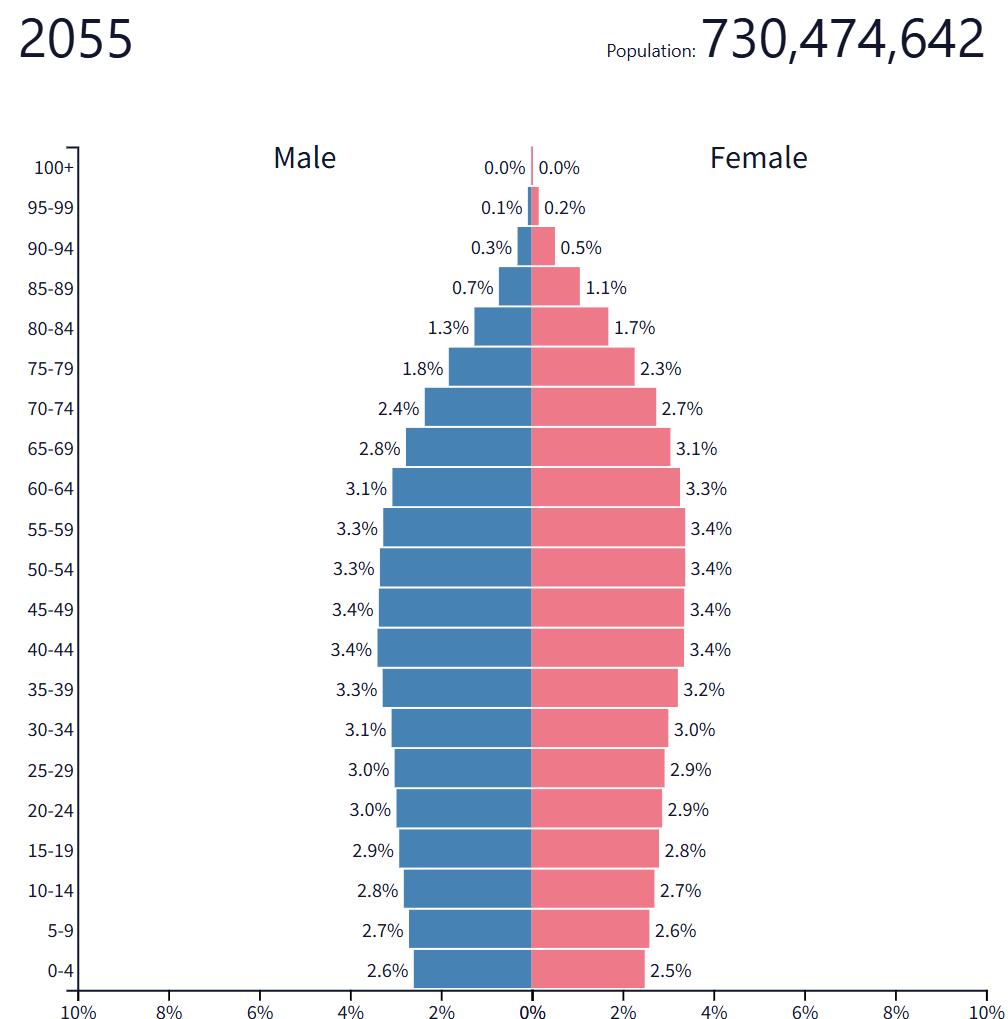

MercadoLibre (MELI) is a leader in e-commerce and fintech in Latin America. Founded in 1999, its business covers 19 countries including Brazil, Mexico and Argentina, comparable to the "Amazon of Latin America". The company has built a closed loop from e-commerce platforms to financial payment ecosystems, deeply integrating into the market of 670 million people in Latin America. The significant changes in the population structure in Latin America have driven the growth of its e-commerce business. The population structure in Latin America is showing a clear trend of being younger. This group is enthusiastic about digital consumption and prefers online shopping, which fundamentally benefits its e-commerce business.

The driving factors for business growth include: 1) Accelerated urbanization (more than 80% of the population lives in cities), improving logistics accessibility; 2) The expansion of the middle class (expected to account for 65% by 2030) and the enhancement of consumption capacity; 3) The penetration rate of smart phones has rapidly increased from 50%, promoting the use of mobile e-commerce. The company seizes this demographic trend, leveraging its operational advantages in the local area and the ecological closed loop of e-commerce and payment, continuously leading the market with huge growth potential.

Source: PopulationPyramid

Industry Overview

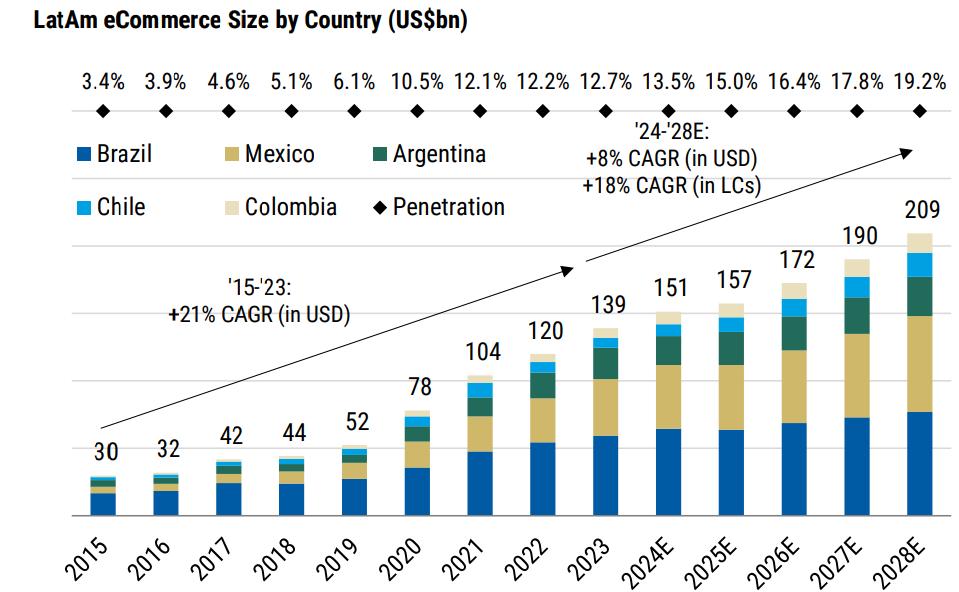

The e-commerce market in Latin America has shown a significant growth momentum in recent years, although its e-commerce penetration rate remains relatively low. In 2015, the e-commerce market size in Latin America was only 30 billion US dollars. By 2023, it had increased to 139 billion US dollars, with an average annual compound growth rate (CAGR) as high as 21%. This rapid growth is mainly attributed to the increase in Internet penetration rates in major countries such as Brazil, Mexico and Argentina, the rapid development of mobile payment and the gradual change in consumers' shopping habits. As these driving factors continue to deepen, the e-commerce penetration rate is expected to steadily increase, gradually approaching 20% by 2028 from the current level. Although there is still a considerable gap compared with mature markets, this also means that the potential of the e-commerce market in Latin America has not been fully unleashed. In the future, the rapid growth of some markets (such as Argentina) will further drive the expansion of e-commerce scale, and the e-commerce business in Latin America is expected to continue to maintain a steady growth trend.

Source: Euromonitor, Morgan Stanley Research

Who is competing with MercadoLibre?

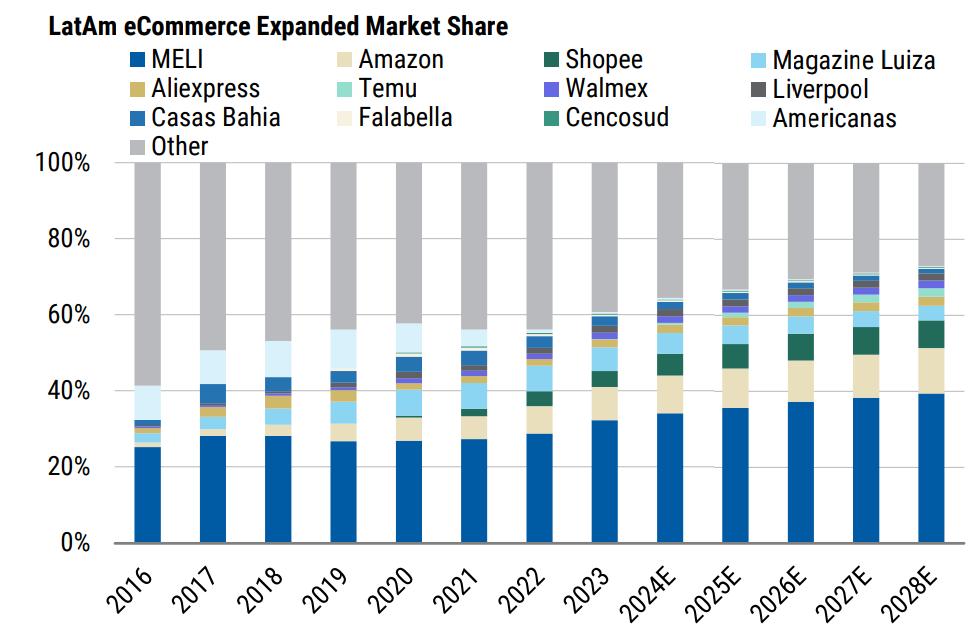

At present, MercadoLibre's main competitors in the Latin American e-commerce market are Amazon, Shopee, AliExpress and local retailers (such as Americanas, Magazine Luiza, Falabella). As its most direct competitor in Latin America, Amazon has been exerting pressure on MercadoLibre with its strong brand influence and logistics capabilities, especially in the Mexican market, in an attempt to narrow the gap. As a Southeast Asian e-commerce giant, Shopee has entered the Latin American market in recent years, especially making certain progress in Brazil. However, due to high operating costs, it later reduced its business in Chile, Colombia and Mexico, and only retained the Brazilian market. Like the recent upstart Temu, AliExpress attempts to attract price-sensitive consumers with low-priced products. However, local users have a relatively low evaluation of its localized services, and its logistics efficiency is also inferior to that of MercadoLibre. In addition, although other local retailers are also active in the e-commerce field, their overall scale and influence are relatively small.

Source: Euromonitor, Morgan Stanley Research

Why can MercadoLibre remain the leader?

The advantage of MercadoLibre lies in its ability to launch solutions that meet local needs based on its long-term and profound understanding of the Latin American market. By establishing a comprehensive ecosystem including e-commerce, fintech and logistics sectors, it can seize the long-term growth opportunities in the Latin American region. Despite the frequent emergence of competitors, benefits to its investment strategy of deeply cultivating the local market, the construction of an integrated ecosystem, and its efforts in logistics and fintech, it can effectively cope with competition and maintain its dominant position in the market.

The business model of MercadoLibre

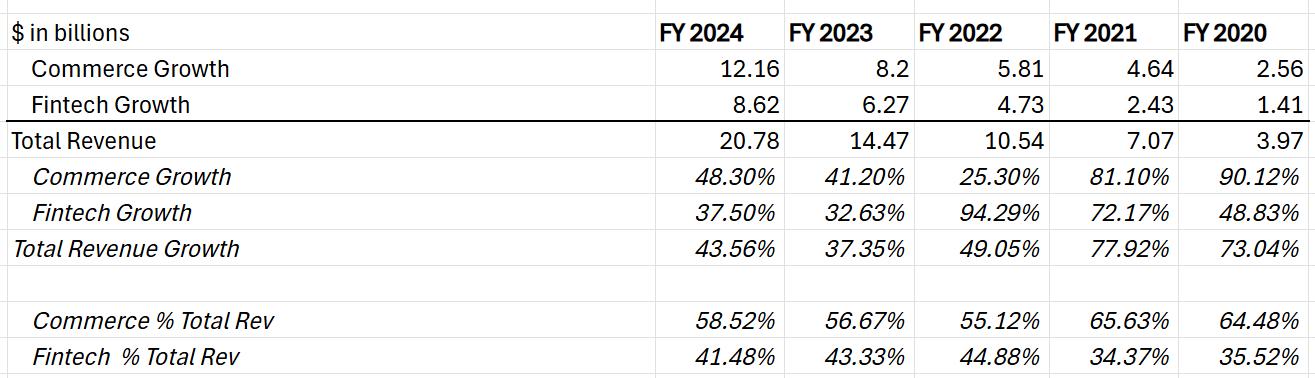

MercadoLibre's revenue sources mainly come from two parts: 1) e-commerce business and 2) fintech services, such as digital payment, credit services, etc.

Source: MercadoLibre, TradingKey

Cornerstone business: E-commerce business

MercadoLibre's e-commerce business mainly consists of two major sections: Commerce Services and Commerce Products Sales. Commerce services are at the core of its e-commerce revenue, similar to Amazon's 3P (third party) business, covering transaction commissions, advertising fees, logistics fees, etc. As a platform, MercadoLibre mainly matches transactions and does not involve the risks of overstocking or unsold goods. Therefore, its revenue is stable and its gross profit margin is relatively high. In contrast, the sale of commercial products is similar to Amazon's 1P (Self-operated) business, with MercadoLibre directly selling goods as the seller, involving costs such as procurement and inventory management, and having a relatively low gross profit margin. In 2024, MercadoLibre's e-commerce business will have a 3P (third party) share of approximately 80% and a 1P (first party) share of about 20%. Currently, the company is more inclined to develop a high-margin 3P model to optimize its profit structure.

The pandemic has significantly accelerated the growth of e-commerce penetration in Latin America. MercadoLibre (MELI), the industry leader, seized this opportunity and continued to expand its market share. Despite the uneven economic recovery in Latin American countries and the widespread challenges of inflation and currency devaluation, which have led to a slowdown in growth rates, MercadoLibre's business has shown a stabilizing trend in the past two years. This is mainly attributed to the steady growth of its gross merchandise volume (GMV) and the continuous optimization of the Take Rate. Compared with the main competitors whose Take Rate only remains at the high single digits to the low teens level, MercadoLibre's Take Rate is far ahead, demonstrating strong market competitiveness. This is mainly because 1) MercadoLibre has been deeply rooted in core markets such as Brazil, Argentina and Mexico. With a profound understanding of the needs of local consumers and sellers, it has established a strong brand influence and pricing power. 2) The company has established an efficient logistics system, with a same-day or next-day delivery rate approaching 50% and a 48-hour delivery rate as high as 80%. This outstanding logistics capability not only enhances the user experience but also increases sellers' reliance on the platform. 3) The company has gradually shifted to the third-party seller (3P) model. By providing value-added services such as advertising and financing, it creates more revenue opportunities for sellers and effectively boosts the overall Take Rate at the same time. 4) Most importantly, MercadoLibre has built a one-stop service ecosystem covering e-commerce platforms, fintech, logistics and advertising. This comprehensive service model has significantly enhanced seller stickiness and attracted 67 million active buyers at the same time, further consolidating its market position.

Source: MercadoLibre, TradingKey

Growth engine: Fintech business

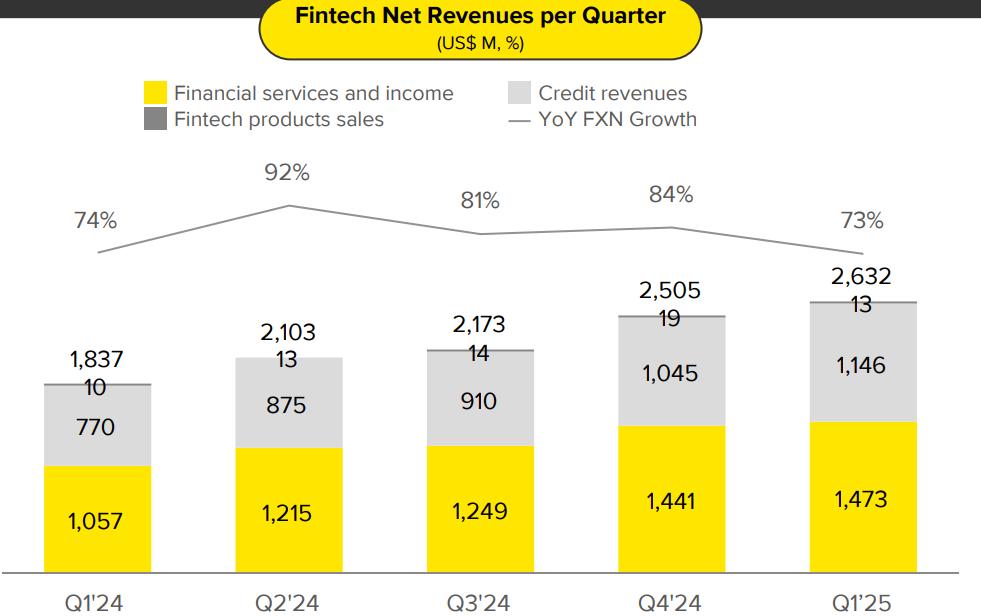

MercadoLibre's fintech business is mainly operated through its subsidiary Mercado Pago, and the revenue proportion of this segment has been increasing year by year. The core income of this department mainly comes from two aspects: One is financial service income, including payment processing fees, transaction handling fees, etc. The second is credit business income, covering consumer credit, merchant credit and credit card products, etc.

Source: MercadoLibre

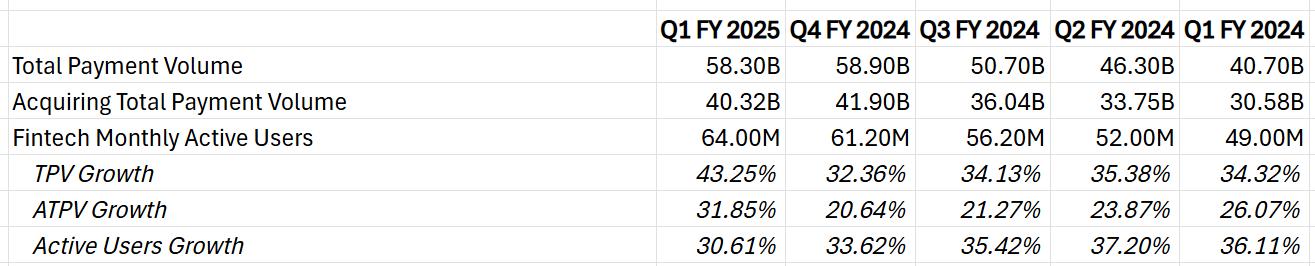

Financial services revenue accounts for a large proportion of the revenue of the fintech sector, among which payment processing business is the main driving force. In the first quarter of 2025, the total payment volume (TPV) reached 58.3 billion US dollars, increasing by 43% year-on-year, demonstrating a strong growth momentum. Out-of-platform payments have become the main growth engine. Due to the fact that the penetration rate of digital payments in Latin America is lower than the average level of developed regions (the market penetration rate of digital payments in Latin America is approximately 60%, while that in developed regions is about 90%), there is considerable growth space and the growth rate is particularly significant. The proportion of off-platform payments in TPV has been continuously increasing, and the growth rate has improved quarter by quarter. Mercado Pago provides transaction services for merchants on the non-Mercadolibre platform through tools such as QR codes and POS terminals. Not only has it grown rapidly, but the take rate of related services is also relatively high. This indicates that Mercado Pago is gradually transforming from an e-commerce payment tool to a general payment platform, covering a wider range of payment scenarios. Meanwhile, the brand influence of Mercado Pago in core markets such as Brazil, Argentina and Mexico has continued to increase, and the user base has significantly expanded. In the first quarter of 2025, the monthly active users of the fintech sector reached a record high of 64 million, with a year-on-year growth of over 30%, further consolidating its market position.

Source: MercadoLibre, TradingKey

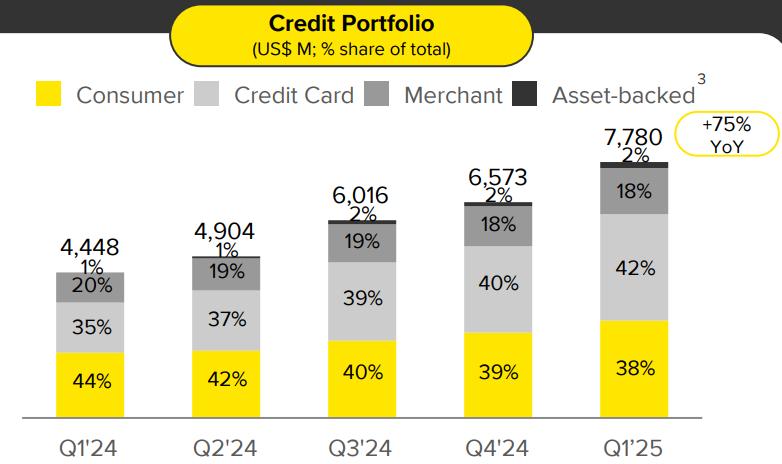

MercadoLibre's credit business has been a key area of development for the company in recent years, covering working capital loans for merchants and consumer loans for consumers, with a particularly strong growth momentum. In the first quarter of 2025, the scale of its loan portfolio had approached 8 billion US dollars, among which the credit card business contributed 42% of the share. In recent years, the company has continuously increased its investment in credit card products, which may stem from two reasons: Firstly, the popularity of digital payment in Latin America has significantly enhanced consumers' demand for flexible credit products; Secondly, the credit card business usually has a higher profit margin, bringing considerable profits to the company. From the perspective of risk management, MercadoLibre's credit portfolio has performed well overall, with the 15-90 day non-performing loan ratio (NPL) remaining stable at 8.2%. In particular, the first payment defaults of credit card loans in the Brazilian region have hit a record low, reflecting the continuous improvement of credit quality. The stable non-performing loan ratio and the relatively low initial default rate have effectively reduced the pressure of bad debt provisions, providing support for the growth of the company's net income. However, although the non-performing loan ratio remains stable, the level of 8.2% is still relatively high compared to mature markets, which to some extent reflects the potential risks brought about by the relatively high economic volatility in the Latin American region.

Source: MercadoLibre

Financial Analysis and Valuation

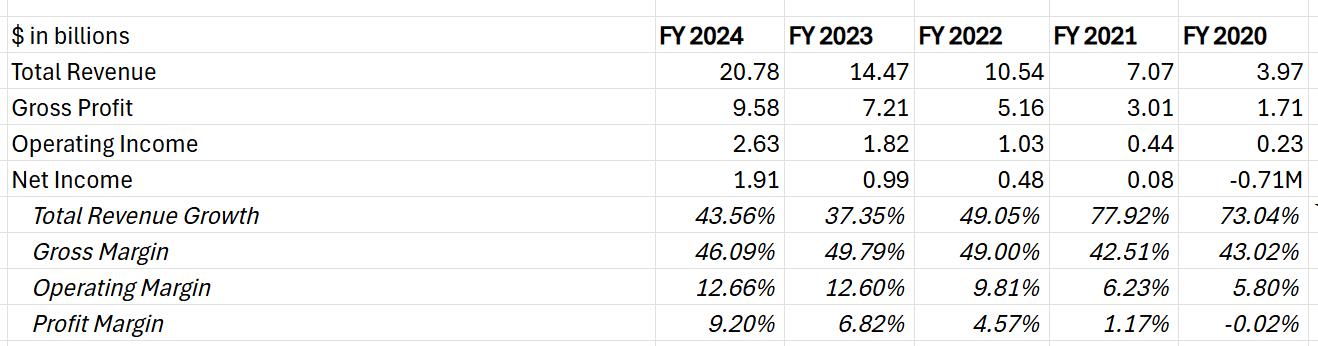

In recent years, MercadoLibre's gross profit margin, operating profit margin and net profit margin have all achieved significant improvements, demonstrating the company's strong operational capabilities and growth potential. Its main driving force is similar to Amazon's strategic path. MercadoLibre optimizes operational processes and effectively reduces costs by making significant investments in logistics and fulfillment infrastructure. The wide adoption of automation technology and digital applications has further enhanced operational efficiency, enabling companies to handle the growing transaction volume at a lower marginal cost. Furthermore, the synergy between the e-commerce platform and the fintech business (Mercado Pago) has been continuously enhanced. Combined with the economic growth in the Latin American region and the increase in consumer spending, it provides strong support for the continuous improvement of the company's key profit margin indicators.

Source: MercadoLibre, TradingKey

The company expects a compound annual growth rate (CAGR) of 16% in revenue from 2024 to 2034, with the revenue growth rate projected to reach 24% in 2025 and gradually slow down to 10% in 2034. However, this prediction might be overly conservative. Argentina's economy may be at the starting point of a new round of sustainable growth cycle. MercadoLibre, with its competitive edge in the country, is expected to continue driving the growth of transaction volume and gross merchandise volume (GMV). In addition, the company's continuous investment in the Brazilian and Mexican markets and the optimization of its logistics network have achieved significant economies of scale. Mercado Pago further increased the high-margin revenue stream by expanding payment, credit and potential banking services (such as applying for a banking license in Argentina), and gradually reduced its reliance on the low-margin retail business. Based on these factors, it is expected that the company's operating profit margin will further increase to 14% in 2025.

MercadoLibre has built a unique business model through the deep synergy of e-commerce and fintech, providing a solid foundation for its valuation premium. The e-commerce platform provides Mercado Pago with a huge traffic entry point, while the convenient payment and credit solutions have significantly improved the conversion rate of e-commerce transactions, forming a positive cycle. The relatively low Internet penetration rate, digital payment penetration rate and the accelerating trend of digital transformation in Latin America offer huge potential for the company's growth in the fintech sector. This unique business model, combined with the structural opportunities in the regional market, has enabled MercadoLibre to gain an advantageous position in the competition and provided strong support for the continuous expansion of its valuation. Based on the expected earnings per share (EPS) of $51.95 for 2025 and a price-earnings ratio (PE) of 50 times, the target share price for 2025 is $2,597.5.

Source: MercadoLibre, TradingKey

Risk

Despite the optimistic outlook, MercadoLibre may face multiple risks in 2025. Economic uncertainties in the Latin American region, such as high inflation and exchange rate fluctuations in Argentina, may weaken e-commerce demand and increase the risk of credit default. The competitive environment is becoming increasingly fierce. The expansion of international giants such as Amazon and Shopee, as well as local fintech enterprises, may erode market share. Furthermore, Mercado Pago's application for a banking license may face strict regulatory reviews, and the increase in compliance costs may become a hidden concern. If high logistics investment fails to achieve the expected return, it may put pressure on the profit margin. These risks may all pose challenges to the company's growth trajectory and valuation.

Recommended Articles