Salesforce Is Building Digital Labor

- Agentforce reached 3,000 paying customers in 90 days, contributing to $900 million in AI and Data Cloud ARR (+120% YoY).

- Salesforce generated $13.1 billion in FY25 operating cash flow (+28% YoY) and achieved a 33% non-GAAP operating margin.

- Valuation remains low at 6.33x EV/sales and 18x forward P/E, despite $60B RPO and AI-led monetization tailwinds.

- FY26 revenue is guided at $41.2 billion with a 34% margin, supporting a fair value estimate of $310–$345 per share.

TradingKey - Salesforce (CRM) is no longer simply a CRM giant; it's now the first enterprise AI-native platform designed for the digital labor era. While the market still values CRM as a mature SaaS provider, Salesforce is undergoing a complete-stack transformation that not only positions it as a principal beneficiary of AI but also as the orchestrator of enterprise AI productivity. The anchor of transformation is Agentforce, Salesforce's fast-growing AI-driven agent layer, combined with its Data Cloud and Customer 360 suite.

What differentiates this moment is the speed and scope of Salesforce's transformation. In FY25 Q4 alone, Agentforce achieved 3,000 paying customers in 90 days from general availability, a $900 million AI & Data Cloud ARR with 120% YoY growth. These are not pilot deployments and therefore include ramped-up integrations across Singapore Airlines, Pandora, and Pfizer. Meanwhile, Salesforce continues to deliver Rule-of-40 level performance: $13.1 billion operating cash flow (+28% YoY), 33% non-GAAP margins, and more than $60 billion in remaining performance obligations (RPO). In an AI gold rush with startups and traditional vendors alike, Salesforce alone possesses the single, unified "apps + data + agents" vision.

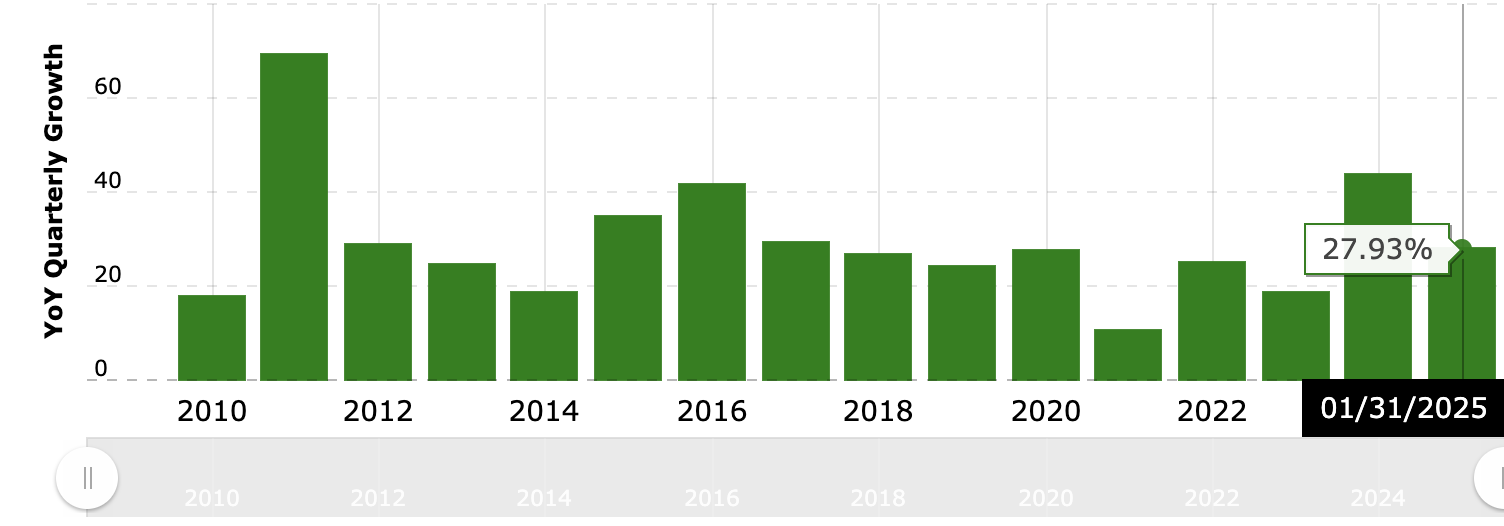

Source: MacroTrends, Salesforce Cash Flow from Operating Activities

This is not a pivot; it's a structural transformation. And with an 18x forward multiple and <6x EV/sales, the market is ignoring the monetization trajectory and operating leverage inherent in this model. For those who will re-rate Salesforce as an AI infrastructure layer, rather than SaaS, the reward is material.

One Unified Enterprise Operating System

Salesforce's business model is now fundamentally different from even two years back. Still central is the Customer 360 suite of Sales, Service, Marketing, Commerce, and Platform Clouds. But overlaid across the top is an AI operating system for the enterprise with a focus on data: Data Cloud consumes more than 50 trillion records (2x YoY growth), and Agentforce converts them into automated processes, digital labor, and optimization functions for the enterprise.

The strategic driver in this case is integration. While AWS and Azure ask clients to cobble together AI tooling, Salesforce offers a single-codebase platform with native agentic capabilities on every cloud. For example, Pfizer is deploying Agentforce across 20,000 sales reps, and Lennar is leveraging it to power 24/7 digital channels with margin optimization across product verticals. Agentforce is being rewritten into Tableau Next, Slack, and MuleSoft with insights, integration, and collaboration unified as agentic workflows.

Salesforce also streamlined the go-to-market rhythm for this vision. In Q4, more than 50% of Agentforce deals included partners, and 70% of activations were from the ecosystem, ranging from Accenture to AWS. Vertical clouds such as Financial Services, Life Sciences, and Public Sector contributed $5.7 billion in ARR (+20% YoY), with almost 75% of the top 100 deals featuring industry-specific agentic deployments.

This end-to-end modularity, enterprise applications, data infrastructure, and self-governing agents, positions Salesforce in a unique space to shape and claim the enterprise AI productivity stack and not simply market licenses for their software.

Riding the Competitive Tides of the AI Tempest

The AI race spurred increased competition in infrastructure, data, and applications. But Salesforce competes in a structurally differentiated space. Its major competitors, Microsoft Dynamics, Oracle, SAP, and ServiceNow, do not have the depth of integrated data or the breadth of in-app embedded AI agents.

Microsoft Copilot and Azure OpenAI integrations are strong but are complicated to configure and provide disjointed flows. Oracle possesses rich vertical stacks without a consumer-grade agent UI. SAP is overhauling around Joule, but execution is disjointed. ServiceNow is strong in ITSM but does not have the scope to tackle horizontal corporate functions with a singular AI approach.

Salesforce, however, is not only putting LLMs in dashboards; it's developing digital labor that carries out the work independently across entire integrated systems. The distinction lies in the latter. OpenTable achieved a 50% increase in query resolution over legacy bots, with Agentforce resolving 73% of requests in only 3 weeks. Internally, Salesforce achieved 84% self-resolution on its help portal across 380K service requests, with only 2% needing human escalation.

Additionally, the pricing leverage for Salesforce is the fact that it can bundle budgets for data, analytics, sales, and customer support into a single AI-native platform. More than 400 deals exceeding $1 million in Q4, and all the top 10 deals featured AI and Data Cloud, affirming that Salesforce is not getting disintermediated by best-of-breed AI startups but capturing their value proposition and up-servicing it through a trusted platform framework.

Growth Flywheels and Operational Efficiency

Salesforce's growth is powered by three intersecting flywheels: agentic monetization, partner-led growth, and data consumption. The AI and Data Cloud ARR ($900 million, +120% YoY) is still early compared to the $38 billion topline, which suggests a lot of upside. With each Agentforce deployment, Data Cloud usage grows, further solidifying platform dependency. Close to 25% of the overall ingested records now are from external sources through Zero Copy partnerships, which shows the stickiness of the ecosystem.

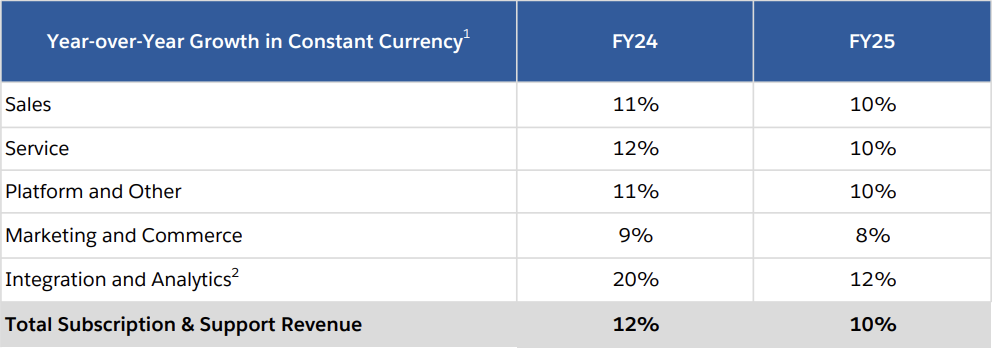

Financially, Salesforce is operating with remarkable discipline. FY25 revenue reached $37.9 billion (+9% YoY), 10% constant currency growth in subscription/support revenue, and the operating margin widened 250 bps to 33%. With an FY26 margin goal of 34% as well as a $14.5 billion cash flow guide, Salesforce is demonstrating faith in margin compounding even as it accelerates AI investment.

Source: CRM Financial Update Q4 FY25

CapEx is kept low compared to hyperscalers because Salesforce intelligently uses AWS, Google, and Alibaba as compute substrates and negotiates favorable prices. The capital-light deployment of AI grants Salesforce the ability to maintain a high return for incremental capital invested.

Also, productivity is increasing without an inflated headcount. AE capacity is up in Q4 with 7% YoY productivity growth led by Agentforce-driven quoting automation and prospect interaction. This indicates Salesforce is deriving operating leverage not only from AI-driven pricing boosts but also from internal application of its own technology, following the lead of Amazon’s AWS self-dogfooding flywheel.

.png)

Source: CRM Financial Update Q4 FY25

Valuation Disconnect and Re-Rating Potential

In spite of beating on margin, cash flow, and execution, Salesforce is trading at a relative discount. At current valuations, CRM is ~6.33x EV/sales and ~18x forward P/E, which compares to peers such as Microsoft (10x EV/sales, 30x P/E) and ServiceNow (15x EV/sales, 42x P/E). However, CRM's margins are on par (33% vs. 32% for NOW), and its AI-native platform arguably presents more TAM optionality.

With FY26 revenue of $41.2 billion and a 34% operating margin, over $14 billion in OCF can be generated by Salesforce. Using a DCF with 10% WACC, 5% terminal growth, and reasonable FCF reinvestment, a base case valuation of $310–$345 per share is obtained, which suggests ~34–70% upside from the current prices.

.png)

Source: Salesforce Q1 FY26 Earnings Call

Most notably, this multiple does not account for Agentforce monetization at scale. If Data Cloud and Agentforce hit $5 billion+ ARR by FY28 (a 50–60% CAGR), the intrinsic value of such a segment alone would support a richer multiple. The market is currently valuing Salesforce as a mature SaaS play, not accounting for the reality that it's essentially becoming the enterprise's AI operating system with usage-based upside.

Risks: Execution, Substitution, and Market Saturation

The greatest danger to Salesforce is not demand, but overreach. If Agentforce does not deliver genuine ROI at scale, or deployment is made complicated by integrations, companies might fall back to straightforward AI bolt-ons from the likes of Microsoft or standalone players. Also, the moat surrounding LLM is diminishing; open-source options and infrastructure commoditization might erode Agentforce's pricing advantages. We also have the issue of saturation. With large enterprise CRM penetration so strong, net-new growth is very much reliant on cross-selling of the Data Cloud and AI. If customers perceive them as incremental rather than transformative, growth can slow down.

Lastly, COO and CFO departures bring with them the risk of leadership transitions. But all such risks are manageable. Salesforce's established installed base, close partner ties, and successful AI monetization provide insulation. The ultimate test is whether it can continue to maintain its AI-first credibility without overpromising delivery timelines or overestimating deployment complexity.

Conclusion

Salesforce is becoming the enterprise AI operating layer, not only providing productivity tools but also autonomous labor at scale. With agentic monetization increasing, embedded infrastructure leverage, and high-margin growth, the stock is fundamentally mispriced. CRM is not only SaaS; it is now an enterprise AI infrastructure.

Recommended Articles