[IN-DEPTH ANALYSIS] Mattel (MAT): Gen Z’s Barbie Rejection Meets Tariff Barriers

Key Points

- Mattel's core brand Barbie faces a double crisis of Gen Z rejection and geopolitical tariff pressures.

- Lagging digital transformation has led to lost market share to Lego and Pop Mart, while supply chain relocation has increased costs by 15%.

- With a 2025 net profit margin likely below 5% and a comparable high P/E, we are quite bearish on Q3 inventory risks, targeting a 15-20% downside in valuation.

Source: TradingKey

Fading Barbie Dolls and the Balance Sheet Blues

While Wall Street cheers the $1.4 billion box office of the Barbie movie, Mattel’s(MAT.O) Barbie dolls are undergoing an unprecedented identity crisis. Once as icons of America’s golden age of consumerism, these plastic dolls are now facing a double squeeze: rejection by U.S. Gen Z and geopolitical tariff pressures.

Mattel’s proud IP is gradually shrinking into a niche market traffic portal. Its three major brands, Barbie, Hot Wheels, and Fisher-Price, contribute 62% of revenue. However, the core Barbie toy line has seen a 14% YoY decline in growth, while Fisher-Price’s infant toy profit margin has dropped below 5%. The 28% revenue from film/TV production and IP licensing royalties is insufficient to cover production costs. With its core business growth lagging the industry average by 5 percentage points, Mattel’s struggles highlight a stark reality: Gen Z consumers are fleeing the seemingly shining world of plastic toy IPs.

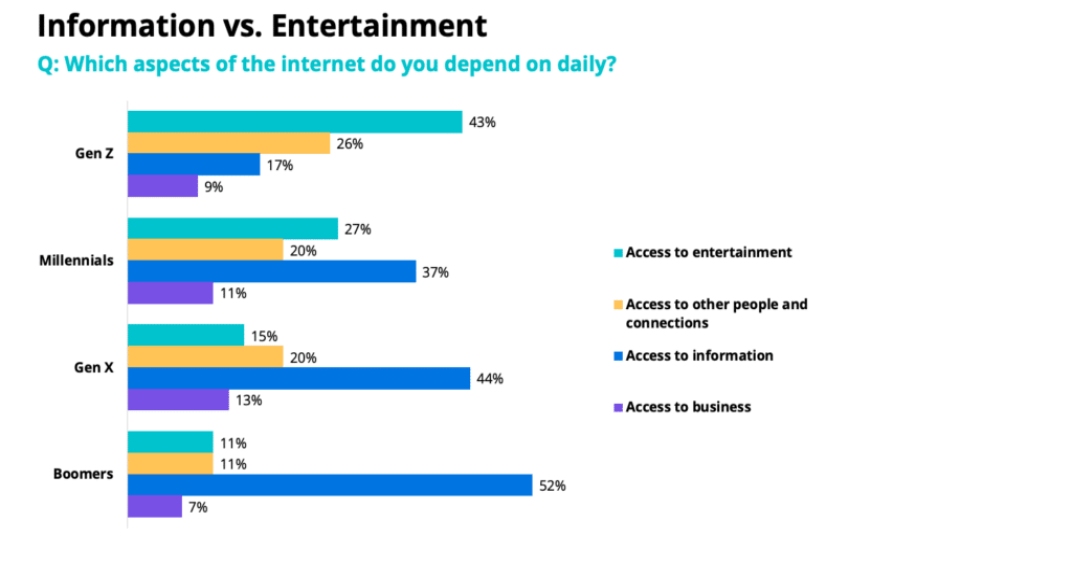

Gen Z’s Rebellion in the Digital Age

Gen Z (born 1997–2012), often called “digital natives,” has grown up in internet-driven digital culture. Compared to millennials and Gen X, they rely more heavily on the internet for entertainment (not just information). Since the pandemic period, their dependence on video streaming has surged, fueling global subscription booms for platforms such as TikTok and Netflix.

Source: Marketing

Despite Gen Z’s annual $400 billion spending power growing rapidly, Mattel has been stuck in $5.4 billion revenue for recent five years. The physical form of Barbie dolls struggles to meet Gen Z’s demand for instant emotional connection, while attempts at “simulated robotic Barbies” have backfired due to the “uncanny valley” effect. Those robot dolls ended up looking so creepy that they were only good for Halloween costumes. Over the past years, Mattel's digital toy business has been way behind its competitors. Lego and Pop Mart are killing it in that area, but for Mattel, digital toys only make up 10% of their earnings.

Mattel thought they could copy Disney's playbook by bringing Barbie and Hot Wheels into the metaverse. They wanted to tie their toys to movies and games, just like Disney does. While film adaptation boosted IP revenue to 24%, it still trails Disney’s 35%. The Barbie movie briefly revived 2023 sales, but weak follow-up streaming content and a lack of a series of “character universe” caused both physical toy sales and IP licensing revenue to decline again.

Source: Refinitiv

Facing poor returns from digital transformation, Mattel has shifted focus to IP licensing and data assets. But with Disney’s century-long IP moat and competitors like Pop Mart’s Labubu and Lego’s Monkie Kid, Mattel remains trapped by its reliance on physical toys. As Gen Y mothers get older, the Barbie brand’s value may fade, leaving Mattel facing not just transition but potential refinancing pressure.

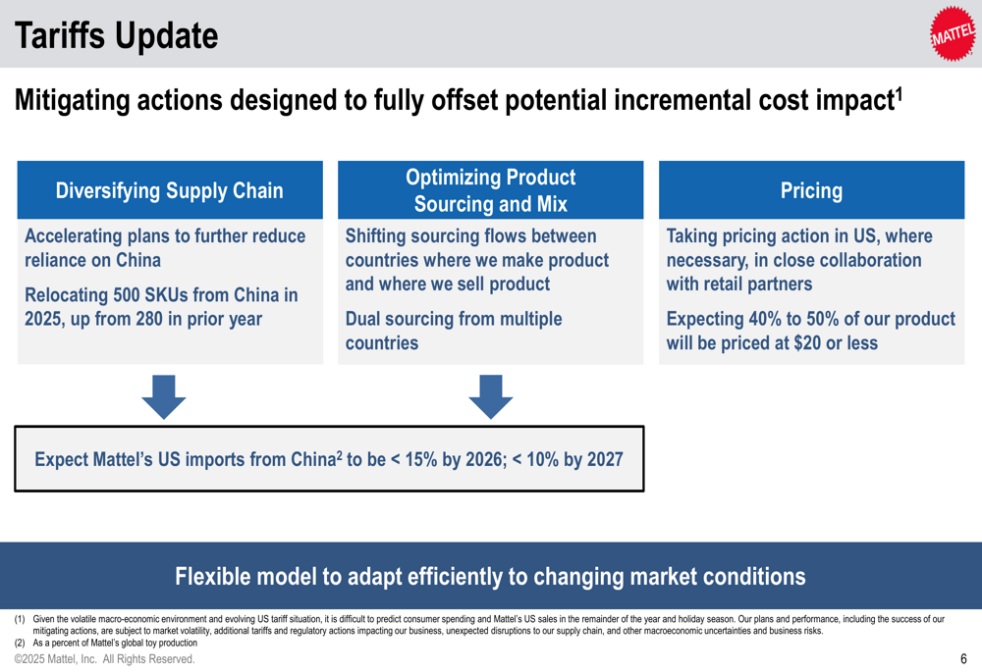

Tariff Matrix and Supply Chain Shocks

Trump’s tariff policies have created a ”short-term loss, long-term pain” situation for Mattel. With high price sensitivity among U.S. toy consumers, passing tariffs on to retail prices could crush sales. NPD Research Group estimates that a full 25% tariff pass-through would raise Barbie’s price to $24.80, nearing the psychological spending limit for middle-class families and risking more than 20% sales drop.

With 65% of production still in China, Mattel’s entire supply chain from raw material procurement to mold development and packaging has been based in the Pearl River Delta in China for two decades. Customs data shows a 32% YoY surge in emergency shipments from China in 2025 Q1, pushing North American inventory to over 4 months. While Mattel’s 2025 Q1 gross margin of 34.5% looks good, net profit still fell by double digits. This “borrowing from the future” strategy, shipping early to avoid tariffs only makes the risk of inventory write-downs in Q2 earnings worse.

Source: Mattel

To speed up production shifts, Mattel’s 2025 Capex has surged 40%, thus turning free cash flow negative. Emergency orders from China have boosted short-term shipments, but global supply chain relocation has raised costs by over 15%. As Mattel struggles in the tariff mess, competitors like Lego are locking in 58% gross margins on AR interactive building blocks through localized European production, effectively capturing the high-end market with digital products.

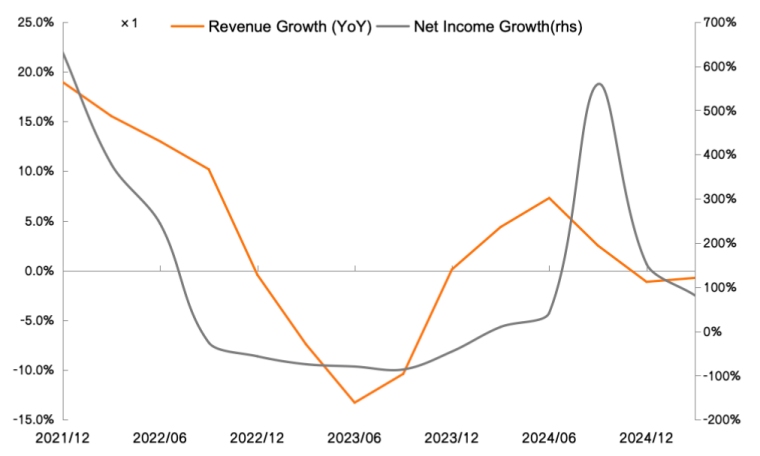

Financials and Valuation

Mattel’s latest 2025 earnings show slowing revenue growth and EBIT margins close to zero, hit by tariff-induced supply chain costs and weak North American demand. Low IP licensing and few high-margin orders, coupled with delayed Southeast Asian production make near-term profit recovery very hard.

Looking ahead two years, Mattel faces dual challenges. Management has withdrawn earnings guidance in Q1, warning of concentrated tariff impacts in Q3. Trump’s reciprocal tariff policies will cut China-sourced products from over 50% shipments to below 10% by 2027. Market share is being taken by emerging brands (e.g., Pop Mart), with gross margins expected to keep falling and EPS likely to turn out negative later this year.

With toy tariffs likely to persist, we expect Mattel’s 2025 net profit margin may fall below 5%, while its forward P/E of 16x remains above the industry average (14x). We are kind of bearish on catalysts like Q3 inventory write-downs or poor IP monetization, with a target valuation of 14x, meaning the stock could drop 15–20% from the current $19/share.

Recommended Articles