Lululemon Athletica: Growth Abroad Masks U.S. Saturation

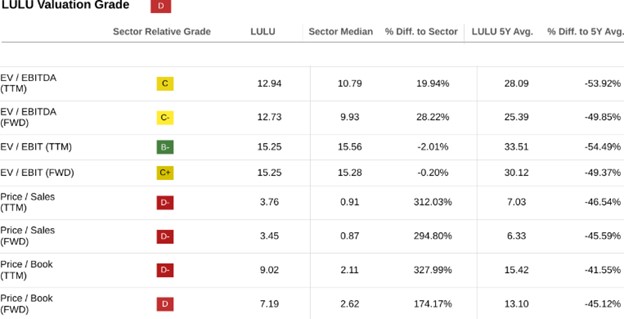

- LULU trades at 3.41x EV/Sales vs. 1.19x sector median and 21.49x P/E vs. 16.9x, pricing in unsustainable growth momentum.

- FY2024 international revenue rose 34%, while U.S. comps stagnated, highlighting early signs of domestic market saturation.

- Revenue growth guided at 5–7% YoY, far below historical CAGR, while EPS growth is projected to rise just 2–3% to ~$15.

- Inventory up 9% YoY vs. 10% revenue growth, risking markdown pressure and margin compression if demand weakens.

TradingKey - Lululemon Athletica's (LULU) phenomenal growth to global supremacy in performance apparel has always been fueled by a virtually flawless implementation of brand positioning, margin control, and consumer intimacy. But with its stock at $321 and valuation multiples far over sector standards, including a forward EV/Sales of 3.41 (vs. a sector median of 1.19) as well as a P/E non-GAAP of 21.49 (vs. 16.90), the market appears to be factoring in unbroken growth. However, such a premium can increasingly be hard to sustain in light of signs of North American saturation as well as increasing inventory levels.

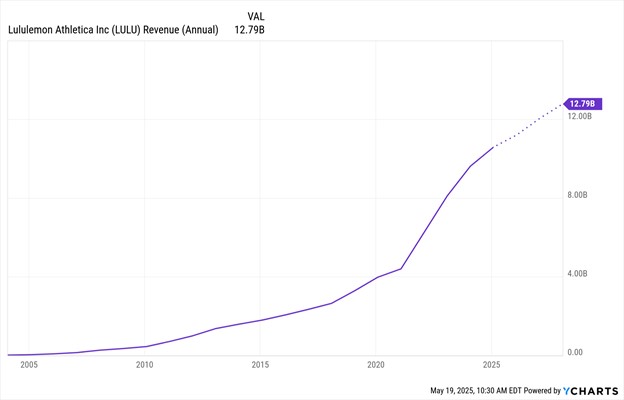

Lululemon's FY2024 was healthy-looking at first glance: net revenue reached $10.6 billion (+10% YoY), operating margin was up to 23.7%, and diluted EPS was up to $14.64. But once we penetrate behind the top-line metrics, the story becomes more nuanced. Global expansion, driven by China (up 41%), hid a more ominous stagnation of U.S. comparable sales. While the tale of global growth is a compelling one, weighted revenue still resides in the Americas, which means that this stagnation poses a substantial threat to compounding in the future.

Additionally, inventory grew 9% YoY, outpacing revenue growth, indicating that demand forecasting could be getting less accurate. This disconnect, in conjunction with a 6–7% topline growth expectation for 2025 (significantly lower than history's CAGR), suggests the double-digit growth expectations in the market might be misguided. The stock's high valuation appears to be more supported by legacy execution than by prospective fundamentals, which represents a nuanced but dangerous threat to allocators looking to buy growth at any cost.

Source: Q4-2024 Deck

Athleisure as a Platform: The Anatomy of the Lululemon Model

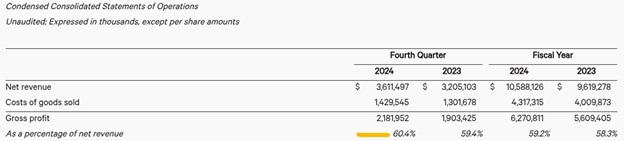

Lululemon is more than a brand. It's a vertically integrated, experience-centric retail machine. It's centered around full-price selling under a tightly managed DTC approach, facilitated by proprietary fabrics, in-segment design, and an experiential store network. The company's “Made to Feel" philosophy extends beyond performance apparel. It designs emotional connection. This integration drives pricing power, with FY2024's gross margins of 59.2% and Q4's 60.4%, among global retail's highest.

Unlike those who depend upon wholesaler channels, Lululemon’s moat is supported by ecosystem control. More than 60% of revenues pass through stores, with approximately 40% from e-commerce, supporting omnichannel equilibrium. The growth of the Essential Membership base, currently at 28 million, up 65% YoY, provides a loyalty-based flywheel, supporting retention and lifetime value. Moreover, product innovation is a structural competency, not an add-on. The introduction of the ShowZero polo and the new range of footwear for men exemplifies how technical differentiation drives category growth.

Yet, though the pipeline of offerings seems strong, with 36 innovations introduced as part of the FURTHER ultramarathon initiative, there has to be a concern over scalability. Do high-touch, ambassador-induced means of operating extend to new markets such as Mexico and China without eroding brand equity? Lululemon’s business prospers in high-end, brand-sensitive markets. Global expansion can stress the brand's positioning, particularly in trying to maintain high price points in lower-income markets.

However, its go-to-market system in integration is still a strength. Lululemon keeps design, marketing, and merchandise planning in harmony to enable quick iteration cycles and protection of margins. But with execution so inextricably tied to brand closeness and experiential retail, the company might not have scale efficiencies in areas that are leverageable as in a platform retailer. It's not a software flywheel. It's a people one. In short, Lululemon's vertical integration drives high-end pricing and loyalty, but its reliance on carefully crafted experiences can constrain scale in more price-sensitive markets.

Source: Q4-2024 Deck

A Two-Speed Company: Dominance Overseas, Saturation in Domestic Markets

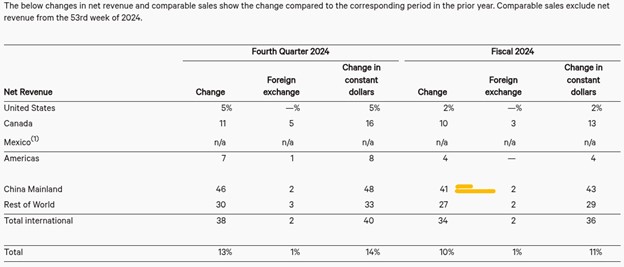

What they quietly hide in the figures, though, is that Lululemon's story is now essentially a tale of two geographies. International revenue in 2024 skyrocketed by 34%, whereas the Americas rose by only 4%. More pointedly, same-store sales in North America remained flat, as international markets rose by +22%. This contrast should serve as a flashing yellow light for any investor counting on reacceleration in North America to sustain current multiples.

China proved to be a key growth engine, adding a remarkable 41% growth in revenue. Milestones such as crossing $1B in net sales and conducting community events in more than 40 cities point toward a solid brand foundation. Nevertheless, China is a minefield for Western brands to execute in terms of geopolitics, supply chain tension, and shifts in consumer preference that still lurk as hidden threats. Moreover, revenue from the rest of the world increased by 27%, which suggests that Lululemon remains in the early innings worldwide, though scale will only come in time, considering the company’s capital-intensive retailer rollout approach.

In contrast, the U.S. narrative is less encouraging. The Power of Three ×2 initiative aimed to achieve $12.5B in revenue in 2026, but with only $1.1–1.3B in incremental revenue in FY2025, which could shortchange the company absent a substantive U.S. reacceleration. Store growth in America is slowing, with only 10–15 net additions in FY2025 out of a total of 40–45. The transition from franchise to company-owned models in Mexico suggests localization becoming a requirement rather than an elective.

Lululemon's differentiated model continues to resonate internationally, but it's starting to exhibit signs of category maturity in its home base. If other high-end brands are enjoying post-COVID bounce-backs, Lululemon is starting to exhibit category maturity in its native land. Unless new drivers of demand emerge, such as AI-personalized retail, next-generation digital experiences, or game-changing apparel technology, the U.S. ceiling might already be in view. Overall, Lululemon's international growth acceleration is robust, but saturation in its home country presents a structural threat likely to constrain valuation multiples.

Source: Ycharts

Margin of Excellence or Masked Risk? A Forensic Reading of Financial Quality

Lululemon's profitability ratios seem great on the surface. Q4 operating margin of 28.9%, TTM EV/EBITDA multiple of 12.94, and FCF yield over 5% in a trailing context. However, forensic indications raise several concerns over earnings quality as well as sustainability. For instance, valuation multiples such as P/S (FWD) of 3.45, as well as P/Book of 9.02, are significantly higher than sector comparables, indicating investors are factoring in not only sustained growth but also impeccable execution.

However, closer observation presents a declining growth picture. FY2025 revenue growth is guided to rise only 5–7%, with EPS in a range of $14.95 to $15.15, a low-single-digit increase from FY2024's $14.64. This dampens the comp history tale, given forward PEGs of 2.10 (compared to a 1.65 average median for its sector). The 9% growth in inventory YoY also warrants attention. Should continued growth in gross margins depend on selling at full price, any deceleration in demand forecasting could set up markdown cycles, pushing down earnings.

The capital-light position represents strength, with $2.0B of cash and no debt. However, returns on capital can start to plateau if store openings continue in lower-ROI international markets. Margins are high but not defensible in a structural manner. While product innovation and pricing generate gross margin, digital ecosystem growth needs to make long-term SG&A leverage more possible.

Ultimately, Lululemon's valuation hinges upon a vulnerable trinity: international velocity, product cadence, and margin resiliency. But as comps level in the U.S., high multiples get increasingly difficult to justify. If growth becomes more of a straight line than an exponential curve, re-rating can happen very quickly, especially in a more unforgiving equity arena.

Finally, even with margin leadership, slowing growth and valuation compression concerns imply Lululemon's premium grows more dependent on performance.

Source: SeekingAlpha

Stretching the Valuation Band: Does It Leave Room to Expand?

Lululemon's valuation today reflects that the market still views it as a growth compounder. Yet, various indicators suggest imminent re-rating. The stock is trading at a forward P/E of 21.49, which stands 43.99% higher than the sector median, and an EV/Sales (FWD) of 3.41, which stands at 186.59% higher than peers. More importantly, both levels are approximately 45-50% lower than Lululemon’s 5-year average, suggesting that the stock has already partially derated from peak optimism.

This derating process isn’t complete yet. The Street might still benchmark to legacy KPIs, such as >20% top-line growth, while FY2025 guidance indicates a mid-single-digit pace. With a top-line CAGR assumption of 7% and constant margins, a fair multiple could contract towards a sector-matched PEG of 1.6–1.7x. That should place a fair forward P/E in a 17–18x zone, which estimates a valuation of $255–$270, or a mere 15–20% from today's price.

A bull argument can make the case that high ROIC, no leverage, and global tailwinds deserve a premium multiple. Even with optimistic scenarios (10% top-line CAGR, stable 24% EBIT margins), however, fair value levels seem to top out at around $360, with limited upside versus execution risk.

Therefore, Lululemon more closely resembles a quality compounder in valuation limbo, not overvalued to short, yet sufficiently richly priced to start a new long absent a sharp pick-up in U.S. demand or category-breaking expansion (e.g., digital wearables, AI-personalized clothing). Until such drivers surface, its risk/reward tilts neutral-to-downside.

Source: Precedence Research

Takeaway:

The valuation premium of Lululemon grows more out of alignment with decelerating fundamentals, suggesting 15-20% downside potential absent new growth drivers.

Lululemon continues to be a class-of-society brand with a defensible franchise and excellent execution, but its valuation currently better represents past success than future opportunity. With U.S. sales plateaued and growth migrating overseas, the firm stands to re-rate in the market unless it can develop new growth channels or revive at-home traction. For institutional investors, the upside from current levels seems limited absent a structural narrative reset.

Recommended Articles