Palantir’s AI Empire Emerges

- Revenue soared 39% YoY, with U.S. commercial growth hitting 71%, confirming Palantir's shift to core enterprise AI infrastructure.

- Fully GAAP profitable, with $214M net income and 42% free cash flow margin, proving capital-efficient scalability at enterprise depth.

- AIP’s AI agents and ontology layer deliver real-time orchestration, surpassing legacy SaaS and commoditized LLM infrastructure approaches.

- Valuation remains rich, but optionality from defense contracts and AI-native enterprise stickiness may justify a structural re-rating ahead.

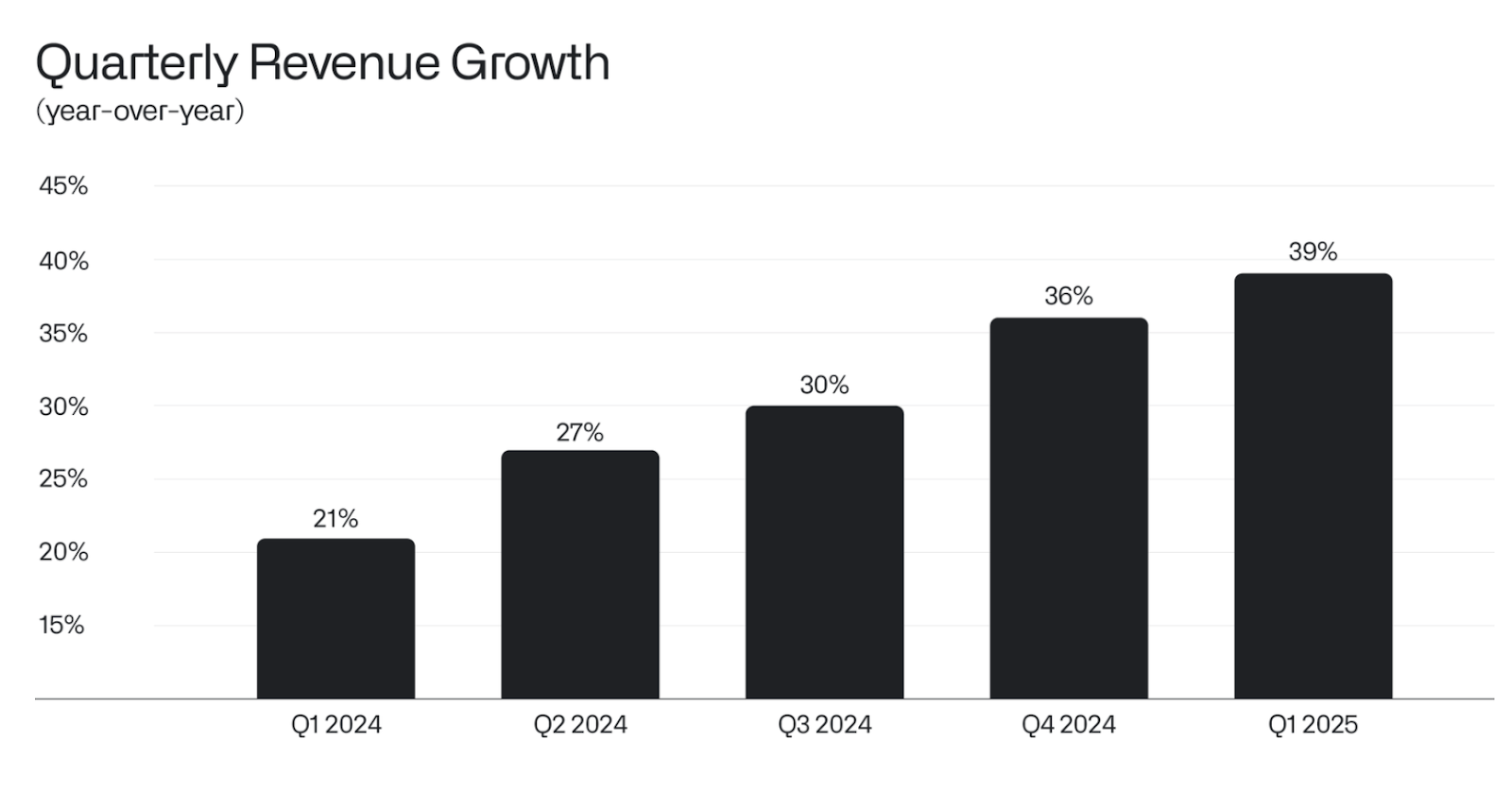

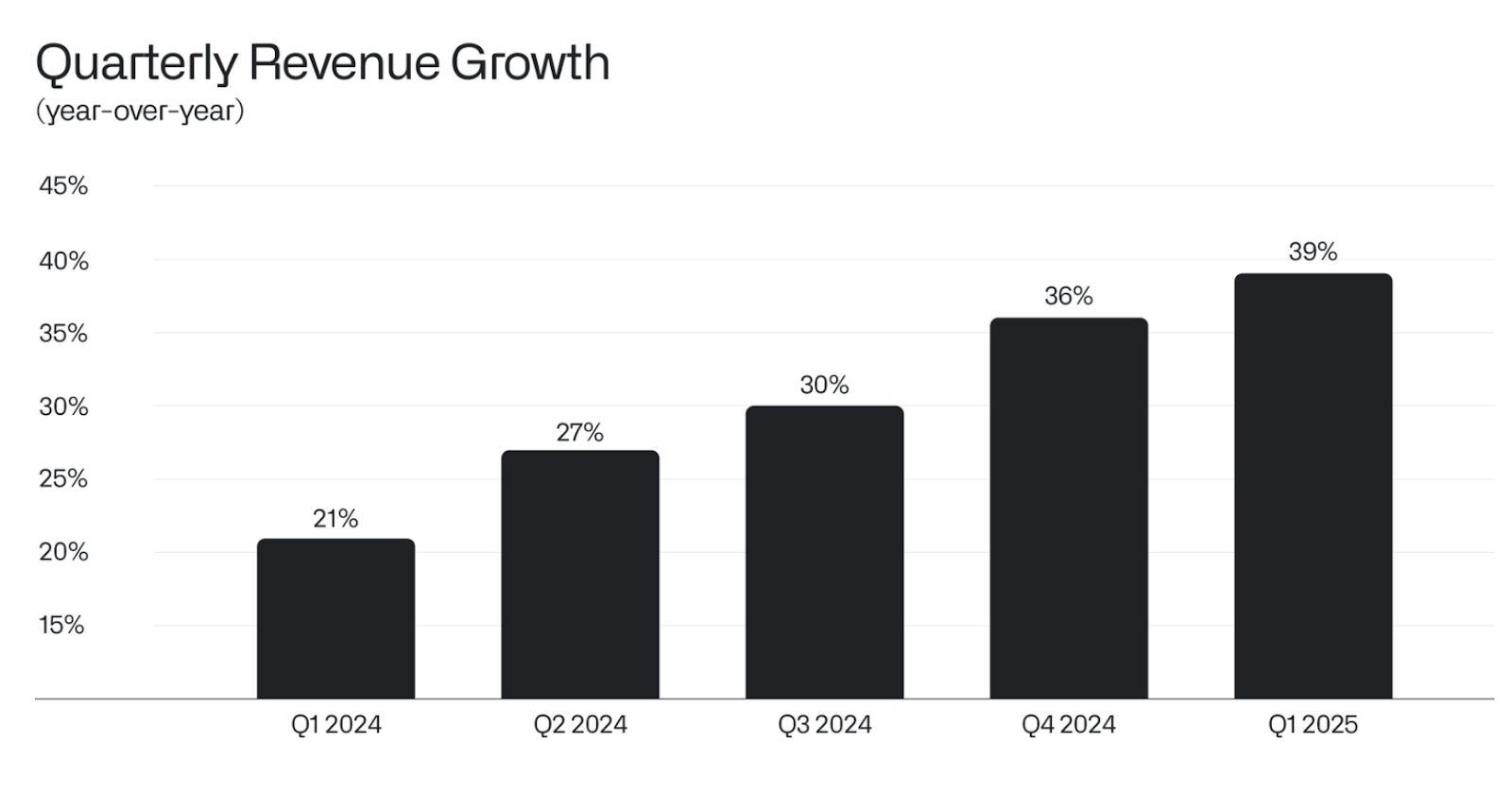

TradingKey - In a model-building-obsessed market, Palantir Technologies (PLTR) has taken a radically distinct path, one that’s proving not only sustainable but also dominant. What was once seen as just a military-focused outsider in the belly of Silicon Valley now appears visionary: the company’s unflinching alignment with U.S. national security and institutional scale enterprise customers. With Q1 2025 revenue jumping 39% year-over-year to $884 million, and U.S. commercial expansion growing 71%, Palantir isn’t merely building software anymore, it’s rethinking the template for AI-native enterprise infrastructure.

Source: Q1 Business Update

What makes it so contrarian is the way Palantir’s story contradicts SaaS orthodoxy. While incumbents bolt AI to existing workflows and the hyperscalers pursue developer adoption, Palantir’s foundation does the opposite: anchored by AIP and the ontology engine, the platform targets the operationalization of AI in the edge of production. Worth noting here is that its Rule of 40 score stood at a breathtaking 83% in Q1, nearly double the sector’s gold standard.

More notably, the organization is achieving this inflection while being fully GAAP profitable, posting $214 million in net income and $370 million in free cash flow in Q1 alone. Palantir’s comeback isn’t a hype cycle bounce, it’s a capital-efficient revolution built on deployment velocity, decision-critical process flows, and a cultural advantage that the competition cannot replicate or purchase.

Palantir's revenue model grows more bifurcated between government and commercial markets but has a stable underlying value engine, its ontology layer. This element becomes the glue that binds enterprise workflows and LLMs together to drive so-called enterprise autonomy. AIP's AI agents are not copilots; rather, these are orchestration engines that perform business logic and operational workflows in areas like logistics, underwriting, and intelligence.

Source: Q1 Business Update

The Orchestrator Advantage: Why Palantir Plays a Different AI Game

While other vendors follow the tailwinds in the domain of generative AI, Palantir harvests the benefit of a decade-long lead in end-to-end AI infrastructure. Snowflake and Databricks may have their grip in the data warehousing and pipeline domain, but these are still relatively agnostic to the operational decision stack. Salesforce (CRM) and ServiceNow (NOW) have all the breadth but still have their roots firmly in CRM and ITSM flows respectively, far removed from the mission-critical AI implementations Palantir is undertaking.

Even the hyperscalers, despite their foundation model capabilities, are lacking in what Palantir describes as “AI demand orchestration.” The DeepSeek moment has revealed the fast-commoditizing nature of LLM supply as performance becomes homogenized in open-source and proprietary models alike. Orchestration now becomes the point: how to make these models work in dynamic enterprise settings in an efficient and quantified way. This is exactly the arena in which Palantir excels and in which competition does not have the architectural foundation to keep up.

Palantir also has a unique cultural benefit in that its go-to-market strategy isn’t designed for scale or speed but for influence within the top levels of an organization. Its “top-down missionary” approach enables Palantir to circumvent bureaucratic resistance by embedding itself in a customer’s transformation journey. As Alex Karp commented, “Two years ago, we’d get a CIO or CMO. Now we get the whole stack, CEO, board, operations”, all working with Palantir.

The company's distinct positioning comes also from regulation asymmetry. In national defense, the long procurement times and high costs of switching make Palantir all but unbeatable. Its Maven Smart System has assumed status as the default AI mission environment for NATO, and its U.S. defense contracts keep expanding within combatant commands. This feeds a strong twin flywheel: defense-grade credibility fueling commercial adoption that in turn finances more intense investment in military-grade AI.

Profit in Motion: Palantir’s Growth Engine Is Built to Scale

Palantir's Q1 financials represent a rare combination of explosive top-line expansion and widening margin profile, qualities that are not often found together to this magnitude. Year-over-year revenue climbed 39% to $884 million, while adjusted operating income jumped to $391 million, or 44% of revenue. Operating cash was $310 million, and free cash flow margins stood at 42%, emphasizing the high-quality earnings.

Source: Shareholders Letter

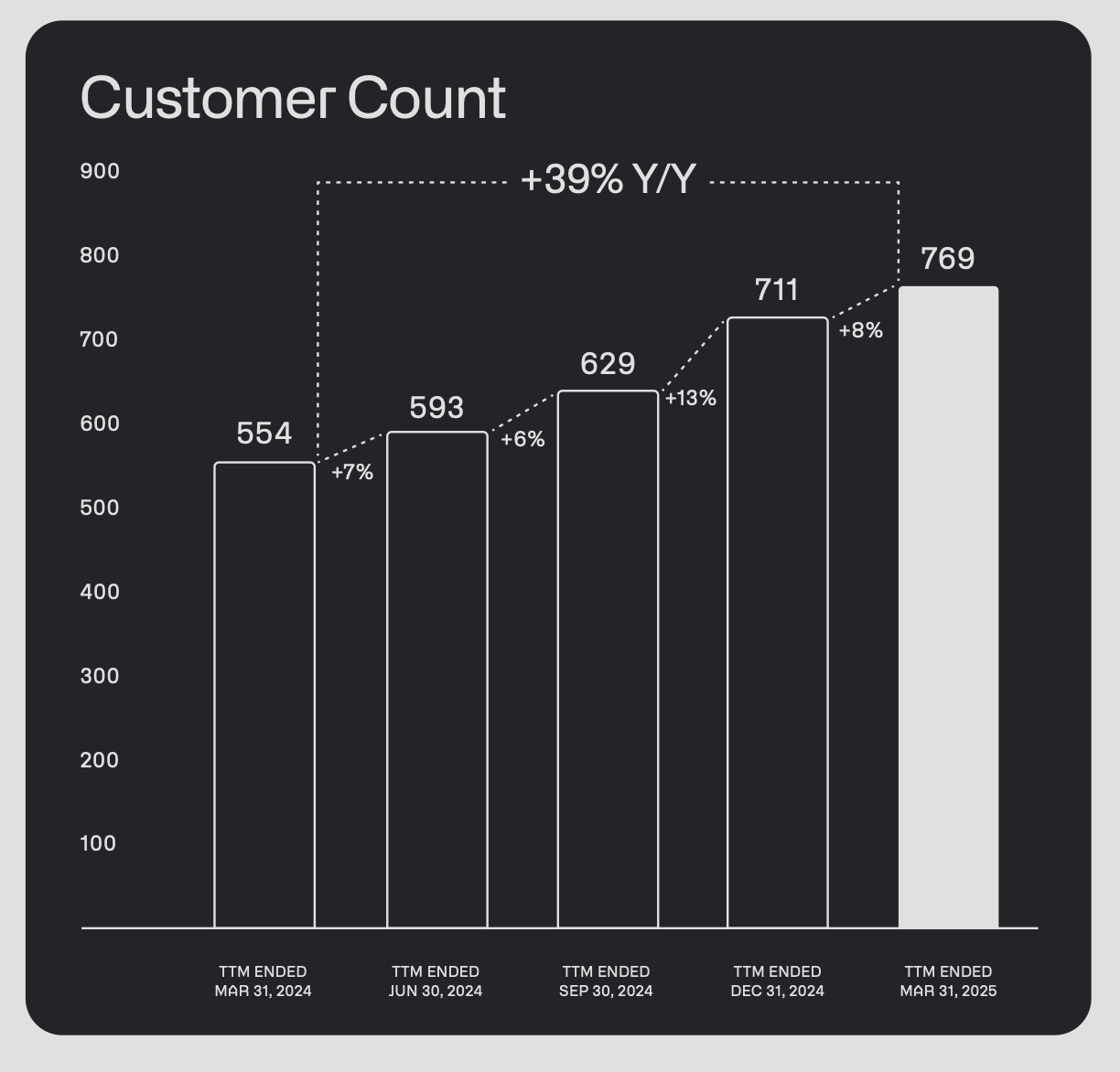

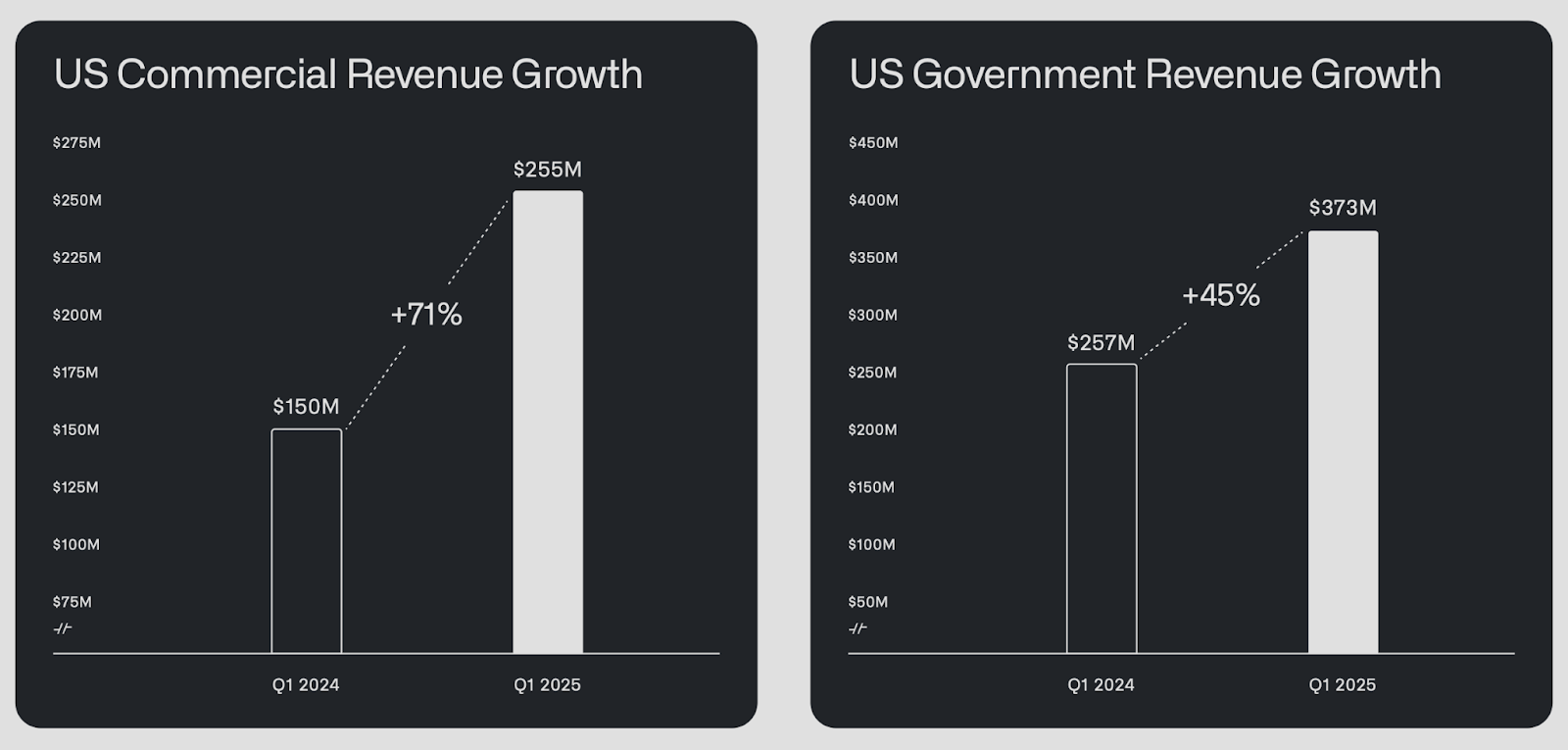

What makes this even more compelling is the consistency across segments. U.S. government revenue was up 45% year-over-year to $373 million and U.S. commercial also surpassed a 71% increase, now representing 29% of total revenues. Infomarkets to note include: customer count up 39% YoY to 769 but top 20 customers spending 26% more, showing solid net dollar retention of 124%, up 400 bp sequentially.

The Rule of 40 score, industry standard for both expansion and profitability, increased to 83%, solidifying Palantir's elite standing. Notably, this was done without sacrificing investment in products. R&D was strong, as was investment in areas of AIP expansion as well as speeding up agent-based work flows that now support use cases as diverse as defense logistics to real-time healthcare decision-making.

CapEx remains low, which maintains the ability to flex capital. The company finished the quarter with $5.4 billion in cash and equivalents, and little dependence on share-based compensation dilution, much reduced compared to the levels in 2021. Operating leverage gets better as Palantir transitions out of intensive bootcamp implementations and towards high-velocity enterprise conversions. Profitability is no longer a guarantee, it’s part of the operating DNA of the organization.

Valuation: Costly but Maybe Not Sufficient

On the surface, Palantir's valuation seems steep. With a forward P/E of ~64x and EV/sales closer to 18x, it commands a premium to the vast majority of its software peers. However, the market is starting to recognize that conventional metrics do not capture the reality. It's not a CRM vendor struggling to eke out incremental churn reduction, it's an AI infrastructure leader that's monetizing production-grade LLM flows in defense and enterprise.

Look at this: Datadog is trading at ~17x EV/sales without Palantir’s free cash flow resilience and AI stack breadth. Snowflake is trading at 21x EV/sales but is yet to monetize GenAI. Even Nvidia, Palantir’s hardware enablement up the chain, trades at ~32x forward earnings without Palantir’s institutional workflow integration.

When comparing Palantir's 83% Rule of 40 and 42% free cash flow margin to the larger SaaS group's averages, its premium becomes reasonable, if not cheap. Using a blended approach of 25x FCF on FY2025e $1.7B FCF and a PEG multiple on 36% top-line growth, Palantir's fair value equates to $32-$36/share. This represents minor upside to levels today but much more in the event that AIP uptake triggers sustainable re-acceleeration.

Most importantly, the framework for valuing must incorporate second-order effects as well. Monetization of ontology, AI agent ecosystem stickiness, and the potential for defense platform compounding (for example, TITAN and Maven exportability) all represent optionality not reflected in traditional DCF or comps models. As the firm transitions to “default operating system” as opposed to “freak show” status in AI deployment, its multiple may re-rate structurally rather than cyclically.

Source: Q1 Business Update

Threats: European Drag, Adoption Friction and Political Volatility

Palantir's executional strength and strategic focus cover up a few risks that need to be monitored. Europe continues to be the sore spot. Q1 commercial revenue internationally was down 5% year-on-year due to structural inertia and AI skepticism. Though the U.S. and allied markets more than make up for currently, Palantir's ultimate TAM realization is subject to geopolitical alignment that cannot happen in the near term.

Secondly, the same qualities that render Palantir distinctive, its cultural idiosyncrasies and top-down sales approach, naturally impede speed. The organization owns up to earlier “ineptitudes in sales and go-to-market,” but even today there remains intensive bootcamping and customization for institutional onboarding of AIP. It scales to mid-market or lower-tier firms but not easily.

Finally, the company's close alignment to U.S. defense policy, which serves as a moat, also subjects it to administrative volatility. In the event that defense spending becomes more constrained or that there's more public scrutiny, contract renewal periods may prove more perilous. With that said, recent DOD officials' testimony and adoption by NATO indicate Palantir's system becoming deeply ingrained as a dependency, moderating but not erasing the exposure.

Conclusion

Palantir's Q1 2025 results confirm its evolution from a mysterious software outlier to a core participant in enterprise AI infrastructure. With unprecedented ontology capabilities, driving monetization in both public and private sectors, and a cult-like internal organization designed for wartime execution, Palantir isn't just riding the AI wave, it's controlling its flow. This is not a cheap stock but perhaps an underpriced system. Institutional investors in search of asymmetric exposure to working AI, defense-grade applications, and capital-light expansion should look through headline multiples.

The underlying tale is that of structural entrenchment rather than speculative mania. In today's context in which AI model commoditization meets real-world deployment complexity, Palantir might be the only software company that's prepared to bridge the gap between abstraction and action, at a global scale.

Recommended Articles