Tesla 2026: Deep Tech Breakthroughs Finally Move the Needle on Earnings

TradingKey - The expectation of weak EV deliveries in Q4 2025 caused Tesla's stock price to open with a slump on the first trading day of 2026. A nine-day losing streak, reflected in its daily K-line chart, also caused Tesla's annual gains to underperform the S&P 500 index.

However, if 2025 was a turbulent year for Tesla, characterized by speculative valuation promises, then with the realization of commercial commitments such as the mass production of Cybercab and Optimus, 2026 could be a year for Tesla to consolidate its technological advancements and return to fundamentals.

Tesla's EV Leader Advantage Erodes

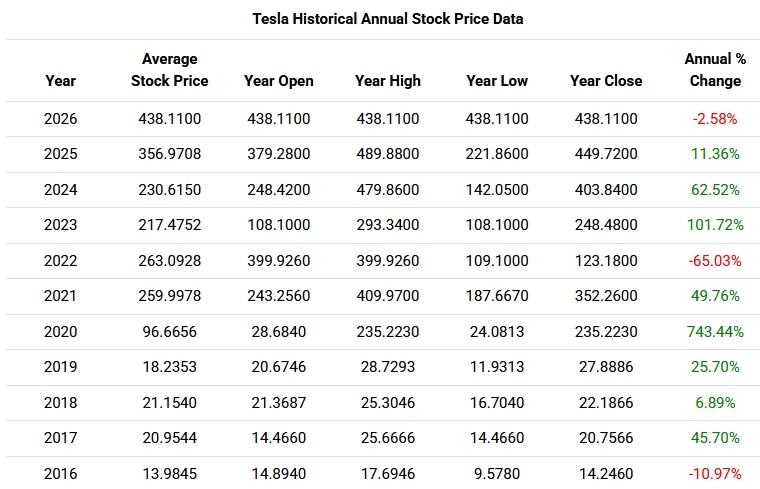

Reviewing the market performance of this electric vehicle manufacturer in recent years, despite complex influencing factors, Tesla's stock price has generally shown a positive correlation with its EV delivery volume. Tesla's stock price surge first occurred in 2020, when high demand for electric vehicles drove the EV leader to achieve profitability for several consecutive quarters, with its annual stock price gain exceeding an astonishing 740%.

Tesla Stock Price Annual Growth Over the Past 10 Years, Source: Macro Trend

Tesla's market capitalization naturally rose significantly, and it was officially included in the S&P 500 index at the end of 2020, at which point its weighting was second only to Apple , Microsoft , Amazon and Facebook ( Meta formerly).

However, the growth challenges in its EV business have put tremendous pressure on Tesla. The latest delivery report shows that Tesla's vehicle deliveries in Q4 2025 were 418,227 units, falling short of the anticipated 440,907 units.

Although Tesla uncharacteristically released a summary of analyst forecasts to temper market expectations, and analysts subsequently made more cautious adjustments, this figure still fell below the company's own targets and market consensus.

This also marked the second consecutive year of decline in Tesla's annual deliveries, with last year's 8.6% decrease significantly exceeding the 1.1% drop in 2024, and falling far short of the annual growth rates of up to approximately 90% seen in previous years.

The slump in Tesla's EV business is not indicative of an overall industry trend; BYD's new energy vehicle deliveries still grew by approximately 8% year-on-year in 2025, and BYD successfully dethroned Tesla to become the 'global EV king' with 2.26 million deliveries.

Year | Tesla Annual Vehicle Deliveries | Annual Growth Rate |

2025 | 1,636,129 | -8.6% |

2024 | 1,789,226 | -1.1% |

2023 | 1,808,581 | 37.7% |

2022 | 1,313,851 | 40.3% |

2021 | 936,222 | 87.4% |

2020 | 499,535 | 35.9% |

2019 | 367,656 | 49.8% |

2018 | 245,491 | 137.9% |

2017 | 103,091 | 35.3% |

2016 | 76,243 | 50.6% |

2015 | 50,517 | 60.0% |

2014 | 31,655 | 40.8% |

Tesla Annual EV Deliveries, Sources: Tesla

Tesla in 2026: Concentrated Realization of Technological Endeavors

Against a backdrop of intensifying competition and reduced policy incentives, continued reliance on its electric vehicle business alone would not benefit Tesla's future. Fortunately, with Tesla's business scope expanding into robotics, AI, and energy storage, its current valuation can no longer be solely assessed based on its status as an electric vehicle manufacturer.

Tesla CEO Elon Musk stated last year that 80% of Tesla's future long-term value would come from the humanoid robot Optimus, rather than its traditional automotive business.

The market harbors mixed feelings about Musk's valuation vision. Optimists believe that Musk possesses the ability to lead Tesla in achieving technological breakthroughs and finding commercialization paths in AI and robotics, a sentiment reflected in Tesla's rebound during the second half of last year.

Cautionary voices, however, contend that Musk consistently over-promises and that the company's PE ratio, exceeding 300 times, already incorporates expectations for these new growth areas, leaving limited room for further valuation expansion.

Analysts at Zacks Investment Research stated that the past two years have been a transition period for Tesla, with traditional EV business slowing. Attention should now shift to the future and the next wave. 2026 is poised to be a breakthrough year for Tesla.

As 2026 approaches, long-standing concerns about Tesla's growth narrative persist. However, with Elon Musk's focus returning to Tesla after securing his 'trillion-dollar compensation package,' this year is set to be a 'year of commercial promise fulfillment' for the company.

Musk anticipates that Tesla will have a widespread Robotaxi fleet by 2026, marking a significant milestone for the company that year. Furthermore, he foreshadowed the near-term release of the Optimus V3 robot and also mentioned SpaceX's ability to achieve full reusability for Starship.

Tesla's autonomous driving sector is expected to see positive advancements in three areas this year.

Firstly, the market is monitoring the expansion of the Model Y Robotaxi fleet, which currently operates only in Austin and the San Francisco Bay Area. While Tesla did not fully deliver on its promise to operate Robotaxis in at least eight major metropolitan areas, including Las Vegas, Phoenix, and Dallas, by the end of 2025, the market remains confident in the Robotaxi fleet's expansion for 2026.

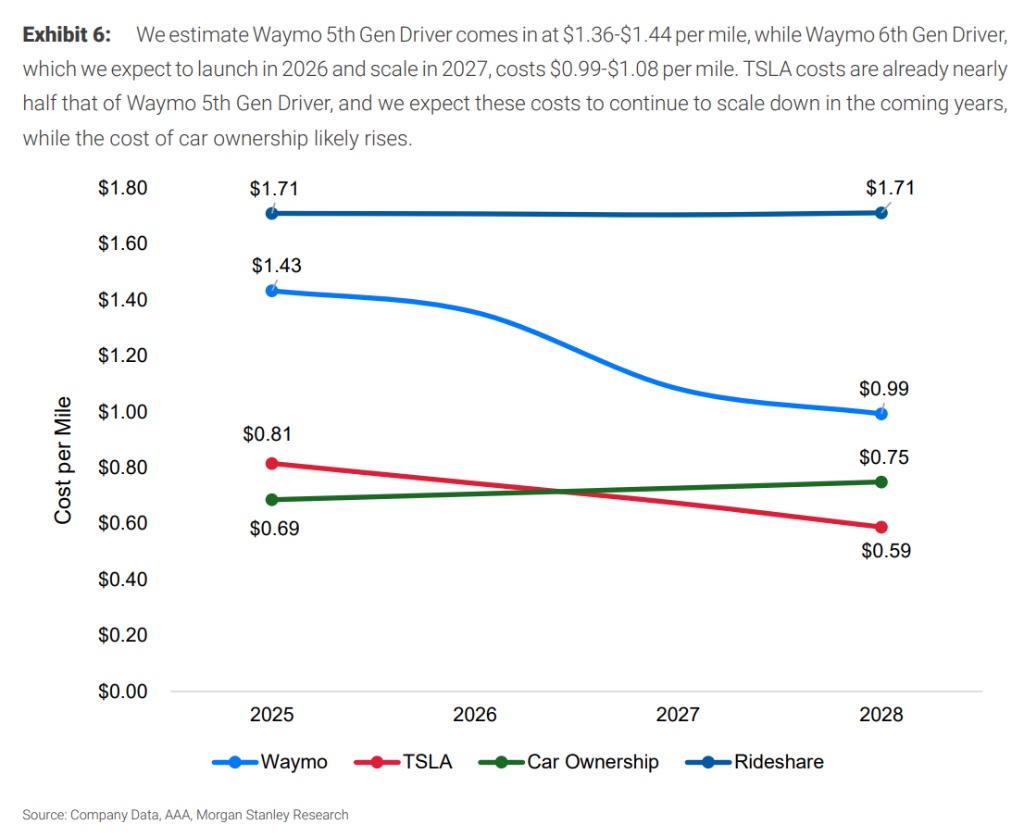

Morgan Stanley projects that Tesla will significantly increase its Robotaxi fleet this year, expanding from the current 50-150 vehicles to 1,000. While this expanded fleet size may still be smaller than the 2,500 vehicles operated by Google's Waymo as of year-end, Morgan Stanley forecasts an opportunity for it to soar to 1 million vehicles by 2035.

According to Morgan Stanley's predictive model, under an optimistic scenario, the Compound Annual Growth Rate (CAGR) for autonomous taxi mileage in the U.S. will reach 116% from 2025 to 2032. Waymo and Tesla are key players in this robust growth market. Waymo exhibits superior safety performance, while Tesla holds an overwhelming cost advantage.

Tesla, utilizing a pure vision system, currently has costs close to that of private car ownership in the U.S., costing $0.81 per mile, which is over 40% lower than Waymo, which uses a multi-sensor system.

Cost Comparison of Waymo and Tesla Robotaxi, Source: Morgan Stanley

Morningstar analysis suggests that the slow rollout of Tesla's Robotaxi service reflects the company's strong emphasis on safety, aiming to ensure effectiveness upon market entry. This may indicate that, after addressing any safety shortcomings, Tesla Robotaxi's cost advantage is poised to become more aggressive as it scales up.

Furthermore, Waymo's malfunction during the San Francisco power outage last December disappointed many regarding Tesla's main competitor and brought the technological route debate between Waymo and Tesla to the forefront. Tesla AI noted that FSD is trained on billions of real-world data points, including power outage scenarios.

Wedbush analyst Dan Ives believes that Robotaxi services will accelerate their rollout nationwide this year, especially considering the mass production of Cybercab. Tesla's ride-hailing service is projected to expand to over 30 U.S. cities by 2026.

This leads to the second area of progress: the mass production of the Robotaxi Cybercab model. The Cybercab features a steering-wheel-and-pedal-free design, positioned as a Level 4 fully autonomous and unsupervised vehicle for all scenarios. One could say that the Model Y is an outdated workhorse, whereas the Cybercab is the ultimate vehicle truly designed for autonomous driving.

Musk recently revealed that they are testing the Cybercab production system, with true mass production set to begin in April. However, neither Musk nor Wall Street institutions have provided a definitive timeline for when Cybercab will commence operations and generate revenue.

Regardless, a prevailing sentiment on Wall Street is that the arrival of Cybercab will make 2026 the year of Robotaxi for Tesla. Cathie Wood of Ark Invest predicts that by 2029, Cybercab will generate $756 billion in annual revenue for Tesla, with 88% of Tesla's enterprise value stemming from Robotaxi, and the EV business accounting for only 9%.

Furthermore, news has emerged regarding the large-scale mass production of the Tesla Semi electric semi-truck in 2026, with its revenue-generating prospects becoming clearer this year.

Logistics company DHL recently stated that Tesla's semi-trucks have exceeded expectations in efficiently completing freight tasks and has decided to integrate them into its North American fleet. DHL plans to significantly expand its Tesla semi-truck fleet in the second half of 2026, synchronizing with Tesla's production capacity ramp-up.

Thirdly, the technological core of Tesla's Robotaxi is the FSD (Full Self-Driving) system, trained on an end-to-end large model. FSD's international expansion is expected to accelerate this year. Currently, only 12% of Tesla owners pay for the FSD software, indicating significant room for growth in this adoption rate.

In addition to continuing to expand adoption in the U.S., Musk anticipates that FSD services will launch their first Middle Eastern market operation in the UAE in January and will also receive regulatory approval in China, the world's largest EV market, this quarter.

System test results in the Dutch market are also paving the way for unlocking a massive market for FSD deployment across the 27 EU member states.

Regarding robotics, Optimus V3 is set to debut as early as March, with mass production commencing before the end of this year. Furthermore, Tesla is preparing to expand its Gigafactory in Texas, constructing a new facility dedicated to Optimus production, with an annual capacity of 10 million units, projected to begin operations in 2027.

The Optimus robot is currently in the development and pilot production phases, primarily for internal testing within Tesla factories and is not yet available for external sales. Under an optimistic scenario, some believe that small-scale external deliveries of Optimus could begin as early as the second half of this year, though its contribution to Tesla's financial reports would be very limited.

If Tesla achieves smooth and substantial progress in areas such as Robotaxi, FSD, and robotics, compared to 2025, Tesla's valuation in 2026 is expected to return to its fundamentals. This is not only because 'dreams come true,' but also because Tesla's financial reports may see tangible gains.

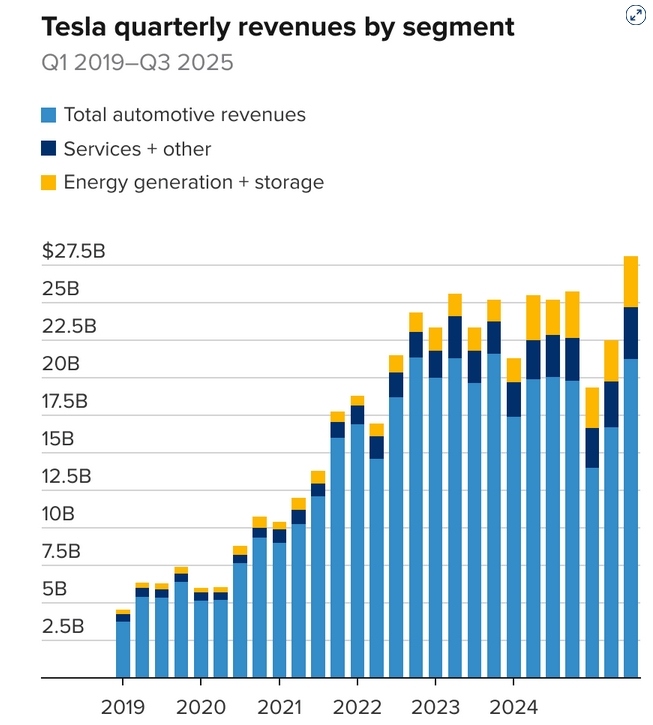

Tesla's electric vehicle business consistently remains the primary revenue driver. Service revenue, including FSD subscriptions, and energy storage revenue accounted for 12.4% and 12.2% of total revenue, respectively, in the third quarter of last year, indicating relatively limited contributions.

Tesla Revenue Breakdown, Sources: Tesla, CNBC

As of Q3 2025, Tesla's net margin has recorded single-digit percentages for seven consecutive quarters. Should higher-margin non-automotive businesses accelerate commercialization, profit margins are expected to stabilize and recover.

The energy storage business might be Tesla's most underestimated segment, or merely a fringe business occasionally mentioned in financial reports. In reality, Tesla's energy storage deployments have maintained high double-digit growth for six consecutive years, serving as a buffer against risks in the automotive market.

Beyond aligning Tesla with the global energy transition, Megapack battery energy storage systems also play a crucial role in AI data center demand and grid stability. In Musk's vision, future expansions of Tesla Energy could also create synergies with the construction of space data centers.

Year | Tesla Energy Storage Deployment | Annual Growth Rate |

2026 | Forecast: 64 GWh | Forecast: 37% |

2025 | 46.7 GWh | 49% |

2024 | 31.35 GWh | 113% |

2023 | 14.72 GWh | 125% |

2022 | 6.54 GWh | 64% |

2021 | 3.99 GWh | 32% |

2020 | 3.02 GWh | 83% |

2019 | 1.65 GWh |

Tesla Energy Deployment, Source: Tesla, Compiled by TradingKey

Musk's Grand Claims

Elon Musk, CEO of Tesla, has consistently been one of the most controversial chief executives in American business, with the market holding a love-hate relationship with his commercial promises and grand visions.

In reality, none of the numerous goals Musk pledged for 2025 have been met, including Robotaxi coverage for half of the US population by the end of last year, the removal of human safety drivers, and the achievement of Artificial General Intelligence (AGI).

Musk's Grand Promises | Actualized? |

Robotaxi to cover half of US population by end of 2025 | No |

Austin Robotaxi to remove safety drivers by end of 2025 | No |

xAI to achieve AGI in 2025 | No |

Flying Roadster prototype to be showcased by end of 2025 | No |

SpaceX to reach Mars in 2025 | No |

US Department of Efficiency to cut $2 trillion in spending | No |

Source: Compiled by TradingKey

As a most straightforward example, the coast-to-coast autonomous driving across the US, repeatedly mentioned by Musk in 2016 and promised for 2017, was only achieved in 2026.

On January 2nd, Tesla's Head of AI confirmed that a Tesla user named David Moss completed the world's first fully autonomous coast-to-coast drive across the US using Tesla's FSD V14. This marks the evolution of FSD software from effective assisted driving to true autonomous driving.

According to Musk's 2026 outlook, Tesla will scale up production this year of three exciting new products: the dedicated Robotaxi Cybercab, the Optimus robot, and the Semi truck. While realizing mass production might be more realistic than achieving service coverage targets, risks such as production delays or not meeting market expectations remain considerable.

Some netizens have summarized that 2026 will be the largest new product launch year in Tesla's history, featuring not only Optimus, Cybercab, and Semi, but also Megapack 3 and new residential solar panels.

Optimus Robot | Mass production in 2026, targeting 1 million units annually; initial commercialization by year-end |

Dedicated Robotaxi Cybercab | Mass production in April 2026; Forbes: Sharing high-margin recurring revenue as early as mid-to-late 2026 |

Electric Semi Truck | Mass production in 2026, targeting 50,000 units annually |

Megapack 3 & Megablock Energy Storage Systems | Mass production in 2026, Megapack 3 annual production capacity up to 50GWh; deliveries in the second half of the year |

Resumption of Residential Solar Panel Business | Delivery in Q1 2026 |

Source: Compiled by TradingKey

Tesla's 2026 outlook states, "See y'all in 2026 - the best is yet to come." Analysts at investment firm Canaccord Genuity also commented that 2026 will be a banner year for Tesla, marked by the launch of numerous innovative products.

From the completion of its end-to-end large models and FSD software driving the shift from "selling hardware" to "selling AI," to the commercialization convergence of Cybercab and Robotaxi, the practical application of Optimus in production lines, and the expansion of energy storage deployment, and further to technological integration with SpaceX, Musk's previous independent investments are now transitioning into a comprehensive system-wide harvest.

Recommended Articles