Palantir: Why PLTR Is So Notorious, Its Stock Performance, and If It's a Buy

TradingKey - Our conclusion is that Palantir (PLTR) stock still offers value for holding. Given the valuation pullback and continued stable and positive earnings, we recommend investors buy on dips. Short-term volatility stems from a cooling of the AI concept and a correction in high valuations, but this pullback actually enhances the long-term investment value.

What Kind of Company is Palantir?

Palantir Technologies (NYSE: PLTR) is a U.S. data analytics and enterprise AI platform company. Founded in 2003 and headquartered in Denver, Colorado, it went public on the New York Stock Exchange (NYSE) through a Direct Public Offering (DPO) on September 30, 2020.

The company was co-founded by Peter Thiel, Alex Karp, and others, initially serving U.S. government intelligence agencies such as the CIA, FBI, NSA, and Department of Defense, before gradually expanding into commercial enterprises.

Palantir's core competitive advantage lies in its three flagship platforms: Foundry (an enterprise data operating system), Gotham (a government and defense intelligence analytics platform), and AIP (AI Platform, a large model enterprise platform).

These three platforms constitute Palantir's true business moat. They offer a complete end-to-end data intelligence infrastructure, providing services from data ingestion, cleaning, integration, and governance to model building, AI inference, and decision execution, particularly in highly complex, massive, and heterogeneous data environments.

These capabilities have enabled Palantir's commercial reach to rapidly extend across manufacturing, energy, financial services, aerospace, biopharmaceuticals, and global supply chain enterprises.

Unlike traditional software vendors, Palantir's value is not in single-point tools, but in its structured data capabilities and decision engines.

The company provides a "deployable AI operating system" that enables enterprises to conduct scenario planning, outcome prediction, and automated execution in highly uncertain environments. This is why it is regarded by the market as a "leading enterprise AI infrastructure company."

Why is Palantir so Controversial?

Palantir's controversies have accompanied the company almost since its inception, stemming directly from its product structure and client base.

Palantir's Gotham system has long been utilized by U.S. intelligence agencies, defense systems, and immigration enforcement departments. These agencies' digitalization needs often involve highly sensitive applications such as tracking individual behavior, integrating cross-departmental databases, and analyzing identity relationships.

There are widespread concerns that such technology could be expanded for use in environments lacking transparency, particularly in counter-terrorism, immigration enforcement, and domestic surveillance, worries that have never dissipated.

Criticism surrounding Palantir also arises from another dimension: the company's clear stance on international political issues, especially its long-term technical support for Israel. Key systems, including border defense, military simulations, and battlefield data integration, directly utilize the Palantir platform.

During periods of heightened Middle East conflict, such collaborations are rapidly amplified, consequently impacting the company's reputation in certain markets. Unlike other companies that typically maintain "political neutrality," Palantir appears to actively take sides, making it more susceptible to labeling.

Furthermore, the company's culture makes it more prone to public resistance. Management consistently emphasizes value narratives such as "national interest," "civilizational survival," and "technological moat of the free world." Such expressions are uncommon in the tech industry, instead aligning more closely with military contractors.

Consequently, in public discourse, Palantir is often perceived as having strong ideological leanings.

How Has Palantir's Stock Performed?

On September 30, 2020, Palantir made its debut on the NYSE via a Direct Public Offering (DPO).

The NYSE announced a reference price of $7.25 per share for Palantir. On its listing day, the stock opened at $10.37, briefly surging by as much as 57%, before closing at $9.50, a 31.03% gain. Subsequently, Palantir's stock traded uneventfully around the $10 mark.

In November 2021, Palantir's first earnings report projected 2020 revenue between $1.07 billion and $1.072 billion, a 44% year-over-year increase, with adjusted operating profit between $130 million and $136 million. It also forecast 2021 revenue to exceed $1.394 billion.

Following this inaugural earnings report, Palantir's stock price tripled by the end of January 2021.

Palantir incurred virtually no customer acquisition costs, and its client base was stable and growing rapidly. In 2019, its top 20 clients generated an average of $495 million in revenue, accounting for 67% of total turnover. While this indicated business stability, it also suggested that the company was unlikely to become a high-growth stock in the short term.

Consequently, this impressive rally did not last. After hitting new highs, investors recognized that Palantir remained a consistently loss-making company, leading to a swift suppression of its stock price.

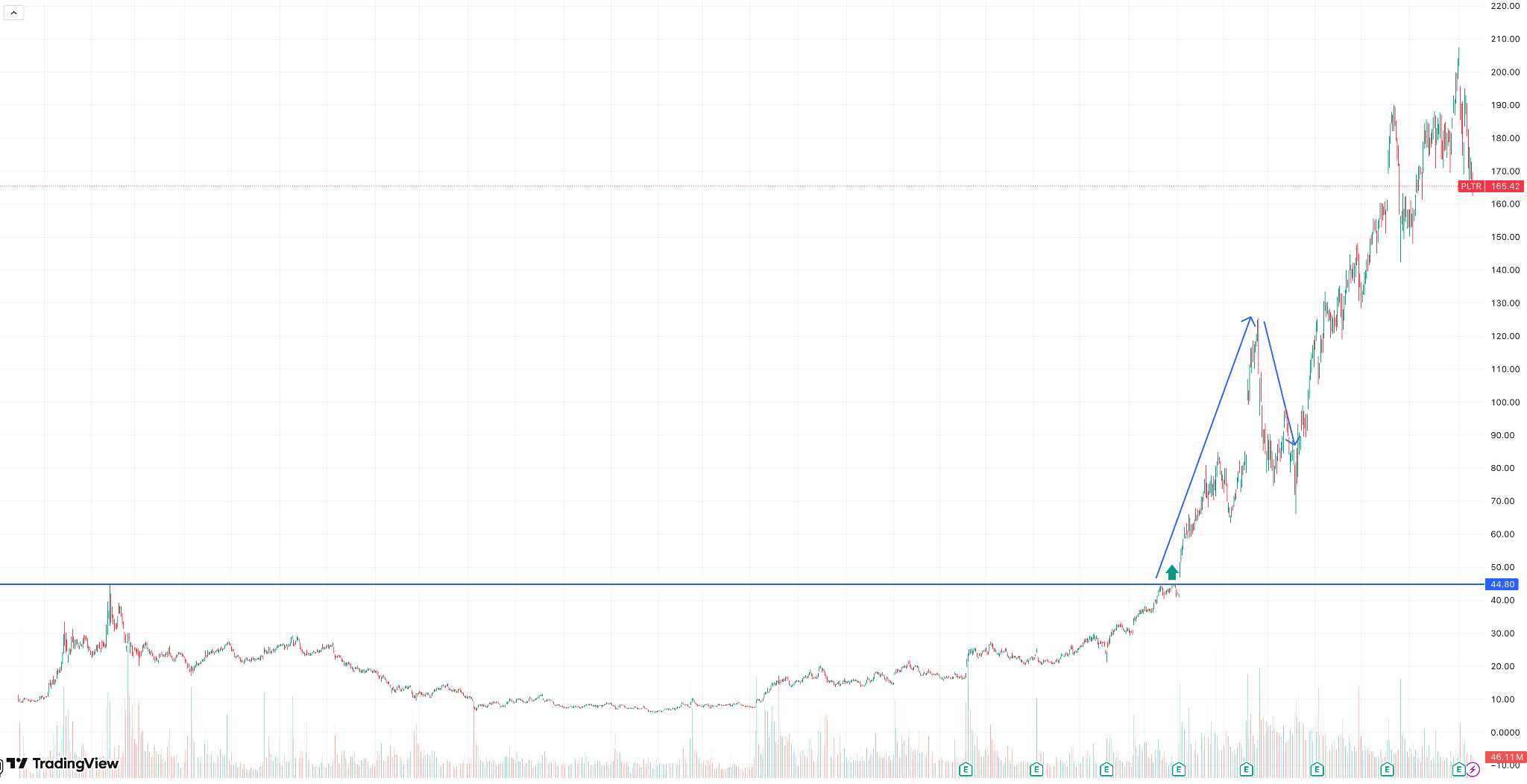

【Palantir Stock Chart (Daily), Source: TradingView】

After the sell-off, Palantir's stock continued to trade sideways in a range, seemingly ignored by investors.

However, with the release of its Q4 2022 earnings report, which indicated Palantir had turned profitable in Q4 2022, the market gradually began to re-evaluate the company. Given its relatively low stock price, this ignited investor enthusiasm, leading to a surge of over 23% on the first trading day after the earnings announcement.

【Palantir Stock Chart (Daily), Source: TradingView】

Driven by its improved performance, Palantir's stock price continued to break new highs.

Even between February and April 2025, when the stock nearly halved from its peak due to tariff concerns, the market quickly realized that systemic risks did not impact the individual stock's underlying logic, as Palantir's core business was largely unaffected by tariffs.

Consequently, as market panic eased and supported by its strong business fundamentals, Palantir's stock rapidly recovered its losses and continued to achieve new highs.

Why Did Palantir's Stock Recently Plummet?

The recent significant decline in Palantir's stock price can be attributed to three main factors:

1. "Sell-the-News" Effect

Benefitting from robust artificial intelligence demand, Palantir projected stronger-than-expected revenue for the fourth quarter.

However, Palantir's stock had already surged dramatically in 2025, climbing 28-fold from its lowest point, implying extremely high future expectations priced into the stock.

When the company's earnings and guidance, while positive, were largely anticipated, some investors opted to take profits. This profit-taking behavior, especially in a high-valuation environment, means any amplification of future uncertainties (such as security concerns or institutional short-selling) can trigger a cascading sell-off.

2. High Valuation Bubble

While the company's Q3 actual results and guidance were not poor, Palantir's stock price previously reflected extremely high expectations for sustained compound growth. When the market begins to question the durability of such high valuations, the stock price can overshoot fundamentals, leading to a faster downward revision.

This year, Palantir's stock has more than doubled, outperforming Nvidia, the world's most valuable company by market cap, and the benchmark S&P 500 Index (SP500). Concurrently, concerns about an "AI bubble" have intensified.

3. Spreading Panic Sentiment

On November 4, 2025, renowned hedge fund manager Michael Burry, who had recently spoken of a bubble, disclosed his decision to purchase put options on Palantir (PLTR) and Nvidia (NVDA).

Palantir is categorized by the market as one of the "AI + Big Tech" leading stocks. Should industry sentiment diverge significantly or turn fearful (e.g., capital withdrawing from highly valued tech stocks), individual stock pullbacks tend to be amplified.

Furthermore, technical breakdowns (such as falling below the 50-day moving average) can trigger quantitative stop-loss orders, further exacerbating the decline.

Palantir's Future Outlook

As of November 20, 2025, Palantir's stock price had fallen from a high of $207.52 to $155.75, representing a decline of 24%, significantly exceeding the Nasdaq index's decline.

【Palantir Stock Chart (Daily), Source: TradingView】

We anticipate that current market panic has not yet fully dissipated, suggesting Palantir may see further lows in the near term. Investors may consider accumulating on dips; after the AI bubble sentiment clears, Palantir's stock is expected to stabilize and strengthen in the long run.

Is Palantir Stock Still Worth Buying?

Our conclusion is that Palantir stock still holds value. Given the valuation pullback and consistently improving performance, we recommend investors buy on dips. While short-term volatility stems from cooling AI sentiment and valuation corrections, this pullback actually enhances the long-term attractiveness of the stock. Here are our three key points:

Strong Endorsement from Nvidia

As a core global AI infrastructure provider, Nvidia's ecosystem is driving AI applications into deeper enterprise-level scenarios. Palantir's AI Platform benefits from its collaboration with Nvidia, enhancing its scalability for enterprise deployments by transforming corporate data into actionable intelligence.

Crucially, the Nvidia (NVDA) ecosystem's backing for Palantir reinforces capital market confidence in its AI capabilities.

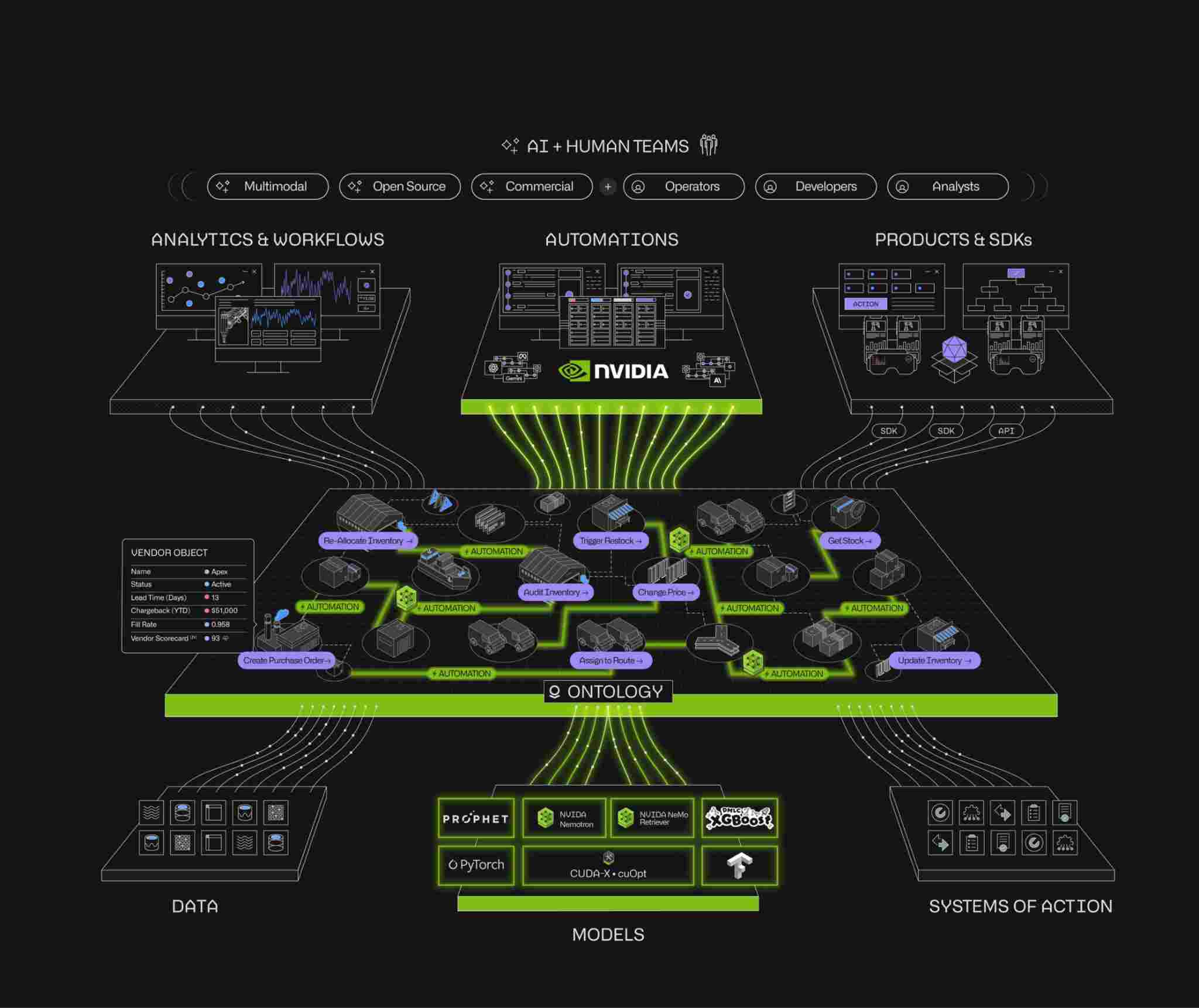

【NVDA Fully Automated Supply Chain Blueprint, Source: Palantir Q3 2025 Investor Presentation】

As AI enters the "practical application" phase, Palantir, as an industry-level AI platform provider, is poised to become a core "software outlet" for Nvidia's computing power.

Valuation Retreats to Reasonable Levels

Following the overheated sentiment in the AI sector, Palantir (PLTR)'s valuation pullback fundamentally represents a market re-evaluation of high valuations.

During this adjustment, Palantir's valuation metrics have receded. The current valuation more closely aligns with its revenue growth rate, profitability, and cash flow performance.

For medium- to long-term investors, this valuation correction provides a more attractive entry point, enabling a better risk-reward ratio before AI commercialization deepens.

Stable Financial Health

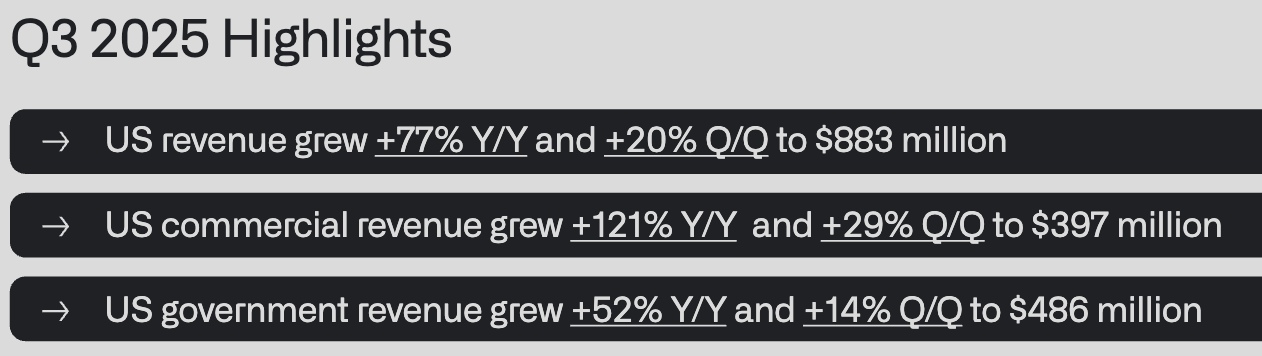

Palantir's Q3 earnings report instilled confidence in many investors, with multiple metrics surpassing analyst expectations and no significant weaknesses from any perspective. Sustained growth in revenue and customer base strengthens Palantir's fundamentals.

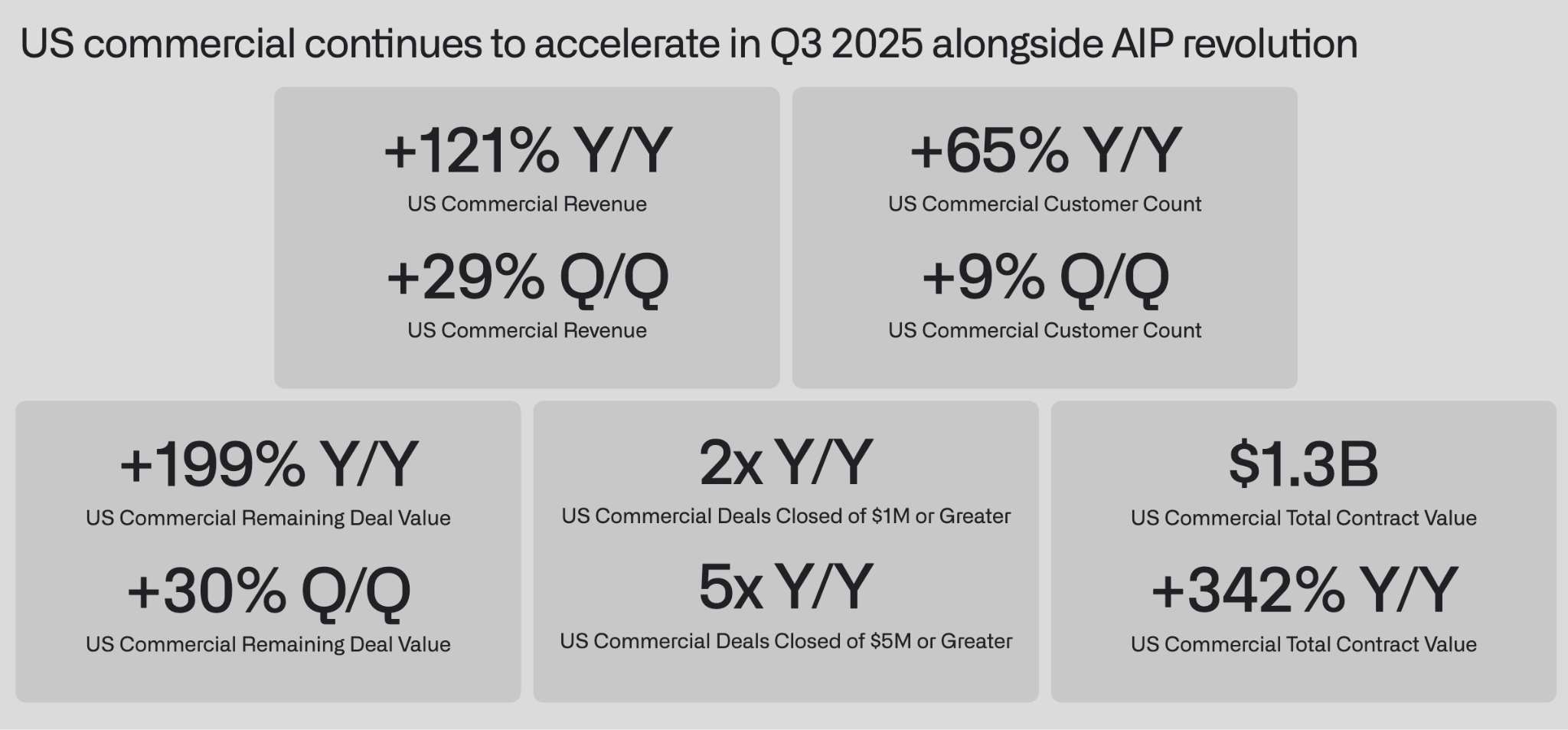

【Source: Palantir Q3 2025 Investor Presentation】

【Source: Palantir Q3 2025 Investor Presentation】

It is important to note that Palantir's earnings report signaled a shift: it is no longer solely reliant on government contracts but is progressively becoming a core provider of enterprise AI applications. Palantir's Q3 earnings report indicated an acceleration in its U.S. commercial partnerships during Q3 2025, alongside an accelerating AIP revolution.

According to the Q3 2025 Investor Presentation, Palantir's growth rate in the U.S. commercial market is significantly faster than its overall business growth. This indicates rapidly increasing enterprise customer demand for a "deployable AI application platform" driven by AIP.

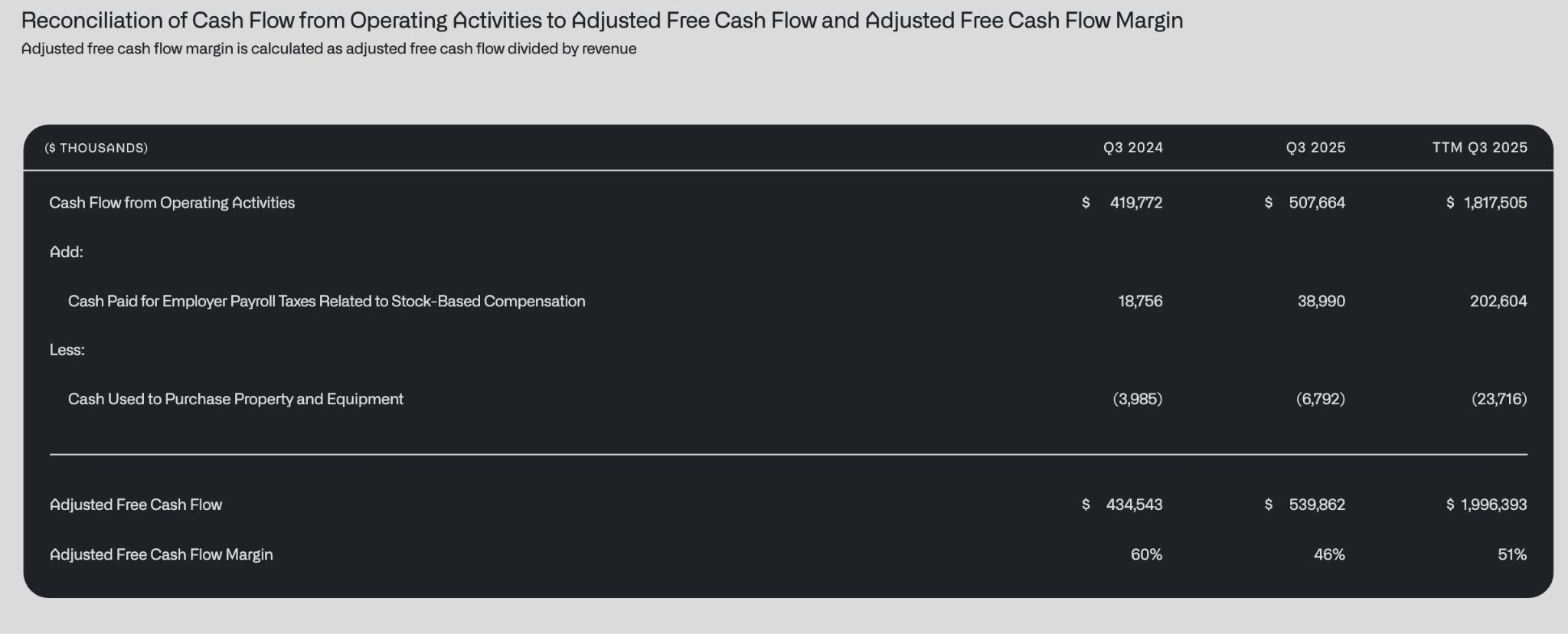

【Palantir's Year-over-Year Cash Flow Status, Source: Palantir Q3 2025 Investor Presentation】

Furthermore, Palantir maintains a consistently healthy cash flow environment, a notable distinction from many other tech companies. This underscores Palantir's financial resilience.

Conclusion

In summary, Palantir's stock short-term volatility primarily stems from market sentiment and valuation concerns, rather than a deterioration in the company's fundamentals.

As capital markets begin to reprice highly valued tech stocks, Palantir remains strategically positioned at the core of the global AI infrastructure ecosystem, leveraging its unique advantages in defense-grade data systems and enterprise AI platforms.

Driven by an strengthening Nvidia ecosystem, accelerating penetration of enterprise AI demand, and rapid growth in commercial contracts, Palantir is poised for robust growth in the coming years. Should market sentiment recover and AI applications move into deeper implementation phases, Palantir's value will likely be re-evaluated upward.

The valuation correction has not undermined its growth thesis; instead, it offers a more attractive entry point for medium- to long-term investors. Therefore, we believe Palantir remains worthy of long-term attention and opportunistic accumulation.

Recommended Articles