Market No Longer Buys the “Future Story” — Dell Punished for Missing Earnings by Just 10 Cents

TradingKey - Dell Technologies(DELL.US) reported its second-quarter results for fiscal 2026 on Thursday, delivering broadly beat-and-raise performance:

- Revenue reached $29.8 billion, up 19% year-over-year — a record high.

- Non-GAAP EPS came in at $2.32, above consensus.

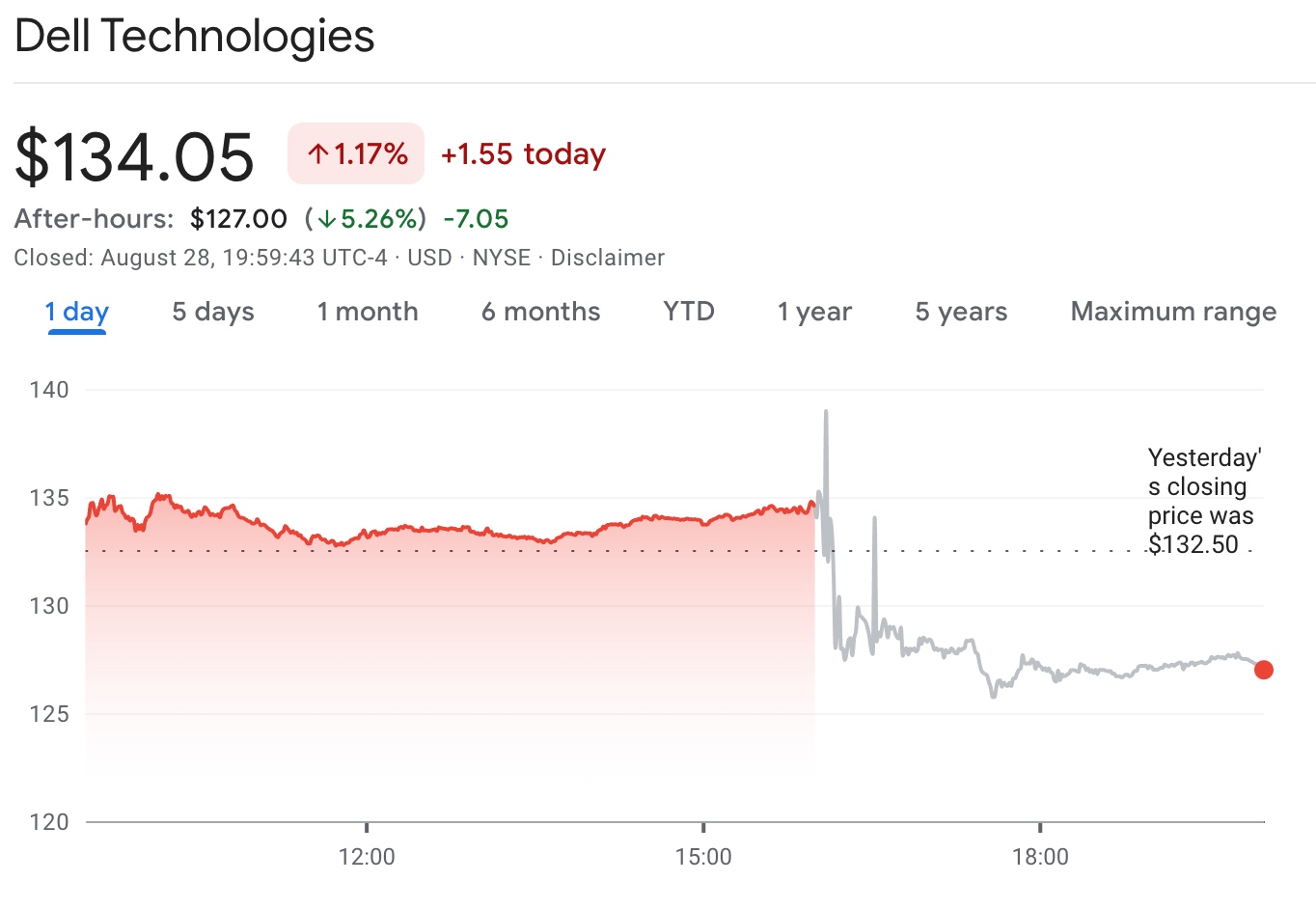

The company also raised full-year revenue and earnings guidance, signaling confidence in its business outlook. Yet, shares plunged over 5% in after-hours trading, reflecting growing investor concerns over short-term profitability and the sustainability of growth.

[Source: Google Finance]

The Core Issue: A Mismatch Between “Growth” and “Profit”

Despite Dell’s forecast that AI server sales will reach $20 billion in fiscal 2026 — doubling from the prior year — AI server orders in Q2 plummeted from $12.1 billion last quarter to just $5.6 billion.

More troubling, the Infrastructure Solutions Group (ISG) — which includes servers and storage — reported an operating margin of just 8.8%, well below the expected 10.3%. The company’s overall non-GAAP gross margin was 18.7%, also below the forecast of 19.6%.

These figures highlight the high-cost, low-margin reality of the AI server business, which remains heavily dependent on expensive components from upstream suppliers like NVIDIA.

Additionally, Dell’s Q3 EPS guidance of $2.45 fell 10 cents short of the expected $2.55, fueling investor pessimism about near-term earnings. The company explained that profits would be more heavily weighted toward Q4.

Meanwhile, traditional PC business remains weak:

- Client Solutions Group (CSG) revenue grew only 1%

- Commercial PC demand is sluggish

- Consumer PC sales declined 7%, dragging down overall performance

Although Dell has $11.7 billion in backlog orders for AI infrastructure and is expanding into enterprise and sovereign AI clients, the market is increasingly focused on whether the company can deliver on profitability amid heavy capital investment and intensifying competition.

Bottom Line:

Dell delivered strong revenue and an optimistic outlook — but in today’s market, that’s not enough. Investors are no longer satisfied with future promises. They want profitability now — and when even a small earnings miss occurs, the penalty is swift.

Recommended Articles