une CPI Report Less Optimistic Than It Appears? Wall Street Warns: Soft Demand Masks Tariff Impact

TradingKey - The U.S. June CPI report, released on Tuesday, July 15, showed a moderate rise in inflation, broadly in line with expectations. While the headline figures appear stable, underlying details suggest that Trump’s tariff-driven inflation is starting to show — but is being partially masked by soft consumer demand.

June CPI Highlights

- Year-over-year CPI rose to 2.7%, up from 2.4% in May, and above the 2.6% consensus forecast, marking the highest since February.

- Month-over-month CPI increased by 0.3%, up from 0.1% in May, and in line with estimates.

Core CPI (excluding food and energy):

- YoY rose to 2.9%, from 2.8%

- MoM increased to 0.2%, below the expected 0.3% — marking the fifth consecutive month of core CPI underperforming forecasts

Market Reaction: Initial Optimism, But Caution Ahead

Markets initially reacted positively, with the S&P 500 and Nasdaq both opening higher — as the core CPI miss suggested that tariff-driven inflation has not yet fully materialized

Wall Street Journal ’s Nick Timiraos noted that the report gives both Trump and Fed Chair Jerome Powell ammunition for their positions. Whether tariff-driven inflation is yet to peak or companies are delaying cost pass-through due to demand concerns, the June CPI offered no clear winner.

Tariff Impact Is Real — Just Not Yet Broad

JPMorgan analysts pointed out that import-heavy categories — including electronics, furniture, and recreational goods — are showing clear signs of price pressure from tariffs, and the trend is expected to intensify.

The bank added that weakness in sectors like autos and travel may be temporary, and that these categories could soon align with broader inflationary trends.

Bloomberg noted that tariff-impacted categories — such as toys (+1.8%, highest since April 2021) , furniture (+1%, highest since January 2022) , and appliances and apparel — are already showing strong price gains, indicating that companies are beginning to pass on higher import costs to consumers.

UBS added that core goods prices — excluding autos — rose at the fastest monthly rate in three years, and unless a recession hits or tariffs are rolled back, UBS expects CPI to remain elevated through the end of 2027, not returning to the 2.3% level seen in April 2025.

But Demand Is Cooling

Despite rising import costs, several signs point to weaker consumer demand — limiting the overall inflationary impact.

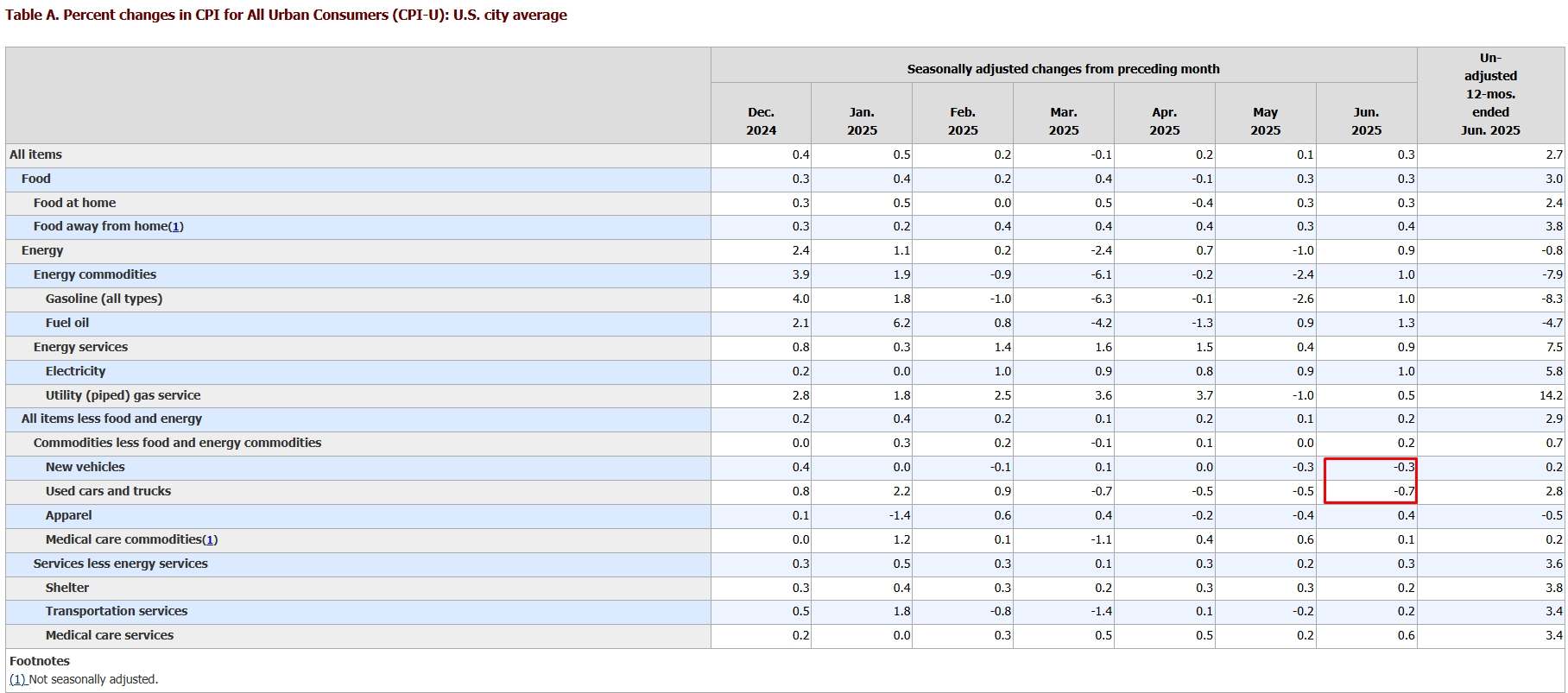

New car prices fell 0.3% MoM, while used vehicle prices dropped 0.7% MoM. Airfare prices also fell 3.5% YoY, indicating continued softness in travel demand.

U.S. June CPI Breakdown, Source: BLS

Scott Anderson, Chief U.S. Economist at Renaissance Macro Research, noted that while inflation is moving in the wrong direction, it is still not strong enough to derail the Fed’s rate cut plans — though it may keep policymakers on hold at the July meeting.

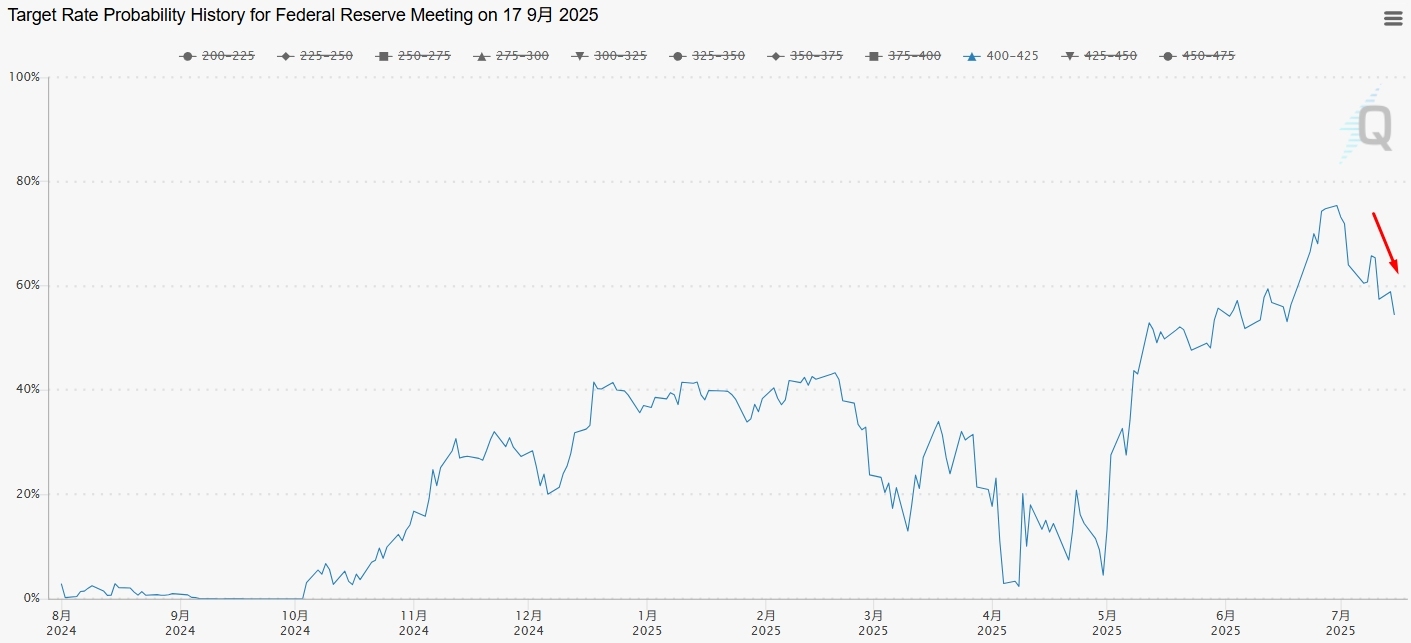

Market expectations for a September rate cut have declined, from 75% at the start of July to around 55% as of the CPI release.

Probability of September 2025 Rate Cut,Source: CME

Cracks in the Labor Market?

At the same time, signs of weakening labor demand are emerging.

The Wall Street Journal reported that job growth is slowing in industries reliant on undocumented workers, and recent immigrants appear less likely to participate in the U.S. Department of Labor’s household survey.

While U.S. consumers are still spending and employers are still hiring, the report raised a key question: How long can this last?

With inflation rising and demand softening, the resilience of the U.S. economy is once again under scrutiny.

Recommended Articles