Why I'd Rather Own Micron Stock Than Sandisk

Key Points

Micron and Sandisk have both delivered monster returns over the last year.

Sandisk has a narrower focus and seems more prone to a pullback after the cycle peaks.

Micron owns its own fabs, which could give it a long-term advantage.

- 10 stocks we like better than Micron Technology ›

Memory chip stocks have been scorching hot in recent months, driven by a massive shortage amid AI demand.

Two of the biggest winners have been Micron (NASDAQ: MU) and Sandisk (NASDAQ: SNDK). Micron is one of the three large, diversified memory companies, along with the Korean giants Samsung and SK Hynix, while Sandisk was spun off from Western Digital last year and specializes in NAND flash memory.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

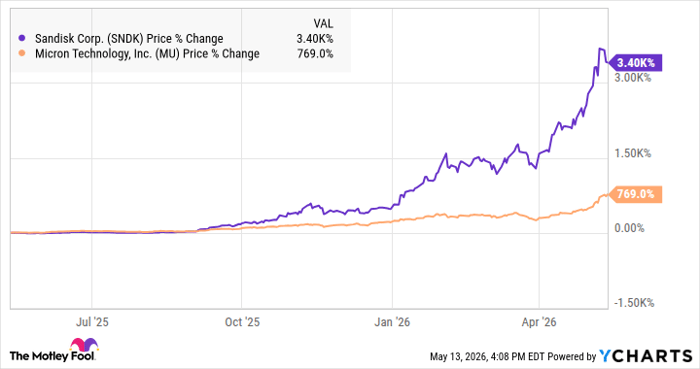

As you can see from the chart below, both stocks have exploded over the last year, though Sandisk has been the clear winner with a whopping 3,400% gain during that period.

SNDK data by YCharts

Those gains have been driven by soaring prices for memory, and as a result, these companies are getting a lot of attention from investors.

While Sandisk's performance over the last year has been remarkable, of the two of them, I'd rather own Micron. Here are a few reasons why.

Image source: Getty Images.

The downcycle will likely be harder on Sandisk than Micron

The memory chip sector is notoriously volatile as it's prone to inventory gluts and shortages, and associated swings in price. The AI boom has brought unprecedented growth to the industry, which likely means that there will be a downside to the cycle at some point, though that could still be years away.

Sandisk is a pure-play NAND stock, and NAND has historically been more cyclical than DRAM, the other major memory category. Sandisk's lack of product diversity also makes it more exposed to any changes in the market or signs of a peak.

Micron is a diversified supplier with DRAM, NAND, and a surging business in high-bandwidth memory (HBM), which is essential for modern AI applications.

Micron also has a history of cyclicality, but its more diversified product range should make it less sensitive to the downturn than Sandisk.

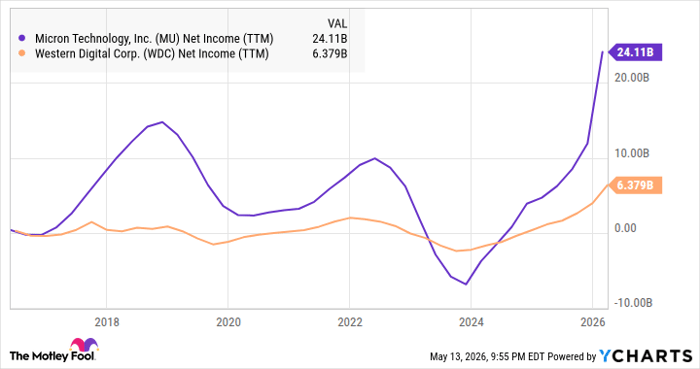

Additionally, Micron has a history of better managing downturns than Sandisk or Western Digital. Sandisk was unprofitable as recently as a year ago, while Micron has only had one significant period of losses over the last decade, relative to its size, compared to three for Western Digital, as the chart below shows.

MU Net Income (TTM) data by YCharts

Micron has its own fabs

Micron is an integrated device manufacturer (IDM), meaning it both designs chips and manufactures them, like Intel, Samsung, and others.

Owning fabs isn't necessarily an advantage. They are capital-intensive, for example, but during a period of massive expansion in the industry, they do seem like a structural advantage. Micron recently broke ground on a $100 billion semiconductor "megafab" in upstate New York, which should allow it to capitalize on the long-term tailwinds in AI, as chip demand is likely to be significantly higher than it was before, even with cyclical forces, due to the need to refresh chips in data centers.

Micron's fabs also seem like an asset during a time when chip manufacturing has become a strategic national interest for the U.S., and the company received billions from the CHIPS Act because of that.

Sandisk, on the other hand, is considered a "semi-fabless" company as it has a joint venture with Kioxia, formerly known as Toshiba, which manufactures its chips, though that arrangement gives it less direct control over manufacturing than Micron has.

A matter of time horizon

Choosing between the two of these stocks is a personal choice to some extent. Sandisk could certainly beat Micron in the short-term, as it has over the last year. It seems to have more leverage to benefit from the memory shortage, and it's growing faster.

However, over the longer term, like five years from now, I think Micron has the edge here. I'm not interested in trying to predict the top in the memory cycle, which seems like a fool's errand, and I'm more than satisfied with Micron's performance over the last year, even if it hasn't been as explosive as Sandisk.

I think Micron is the better long-term stock to own here.

Should you buy stock in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $472,744!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,353,500!*

Now, it’s worth noting Stock Advisor’s total average return is 991% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 14, 2026.

Jeremy Bowman has positions in Micron Technology. The Motley Fool has positions in and recommends Intel, Micron Technology, and Western Digital. The Motley Fool has a disclosure policy.

Recommended Articles