Strategy Sells Coins to Survive. CEO Says It Is to Better Hold Bitcoin?

TradingKey - MicroStrategy, the world's largest corporate holder of Bitcoin, recently released its first-quarter earnings report, showing a massive net loss of $12.54 billion and a diluted loss per share of $38.25, far exceeding market expectations of $18.98.

The losses were almost entirely attributed to $14.46 billion in unrealized losses on Bitcoin; during the first quarter, Bitcoin plummeted from approximately $87,000 to the $65,000 range, with the paper losses dealing a severe blow to the income statement.

Meanwhile, Executive Chairman Michael Saylor signaled a shift in stance during the conference call, stating that the company is likely to sell a small portion of its Bitcoin to pay dividends. Following the announcement, MSTR shares fell over 4% in after-hours trading, while Bitcoin briefly dipped below $81,000 before quickly rebounding. On Polymarket, the probability of MicroStrategy selling Bitcoin this year has risen to 48%.

Pressure for rigid repayment surges.

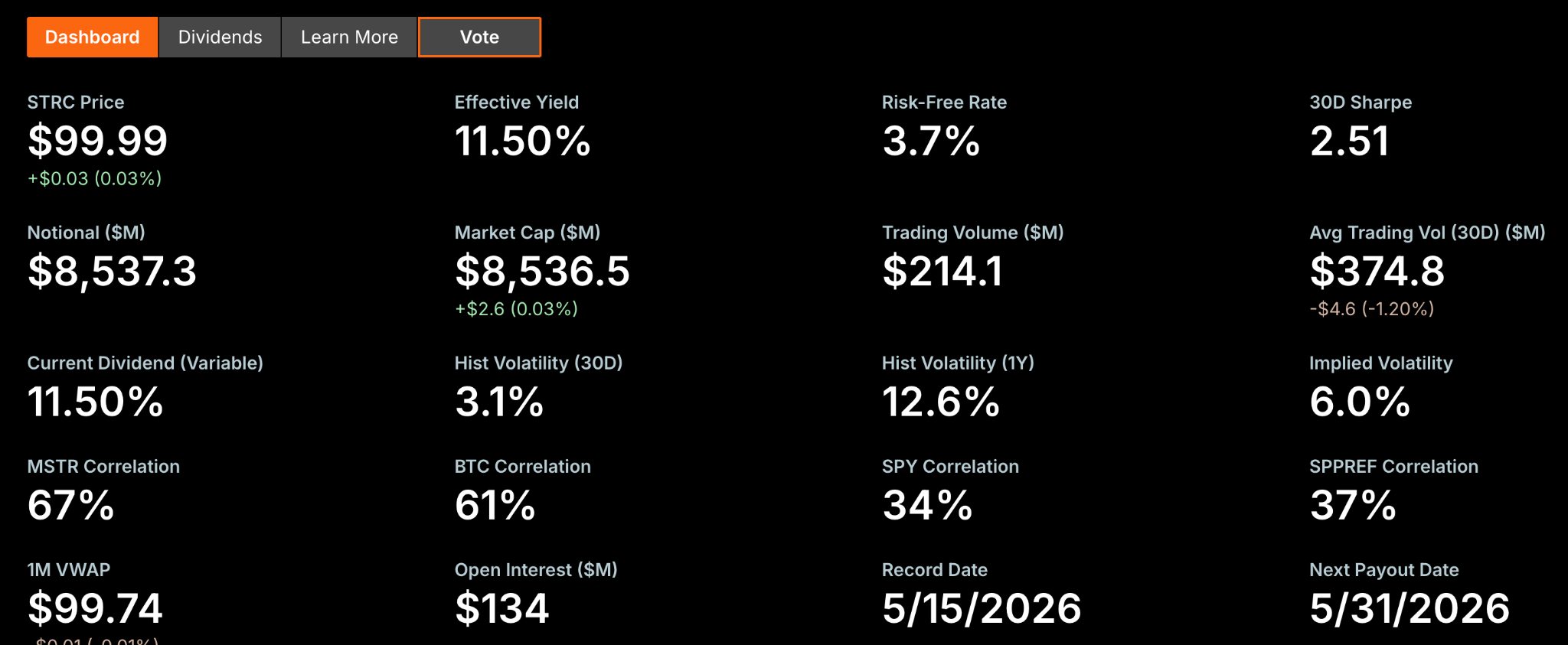

Constrained by the high-yield perpetual preferred stock STRC, which carries an annual yield of 11.5% and has raised approximately $8.5 billion since its launch, this software-rooted company has joined the ranks of the largest preferred stock issuers in the United States.

[Information on Perpetual Preferred Stock STRC, Source: Strategy]

However, this capital comes with a clear repayment mechanism: Strategy must pay preferred shareholders approximately $1.5 billion in dividends annually.

Strategy's management initially planned to continuously raise funds by issuing common stock or STRC to purchase Bitcoin, relying on Bitcoin's appreciation to maintain solvency. This approach remained sustainable as long as the MSTR share price traded at a premium to its Bitcoin Net Asset Value (NAV). However, the sharp Bitcoin price drawdown in 2026 challenged this logic, and MSTR shares also plummeted during the same period. At that time, Strategy resorted to a desperate "severing limbs to survive" tactic by selling Bitcoin, which alleviated its massive cash flow pressure in the short term.

Saylor revealed during the conference call that current annual dividend payments require selling approximately 18,500 to 19,000 Bitcoins, accounting for only about 2.2% of its total holdings of approximately 820,000 coins.

He also estimated that if Bitcoin achieves an annualized growth of just 2.3%, it could perpetually cover the dividends without the need for additional equity issuance. However, in a bear market cycle, if BTC falls back to the company's average cost basis of $75,537, this ratio would be multiplied, and the actual impact could exceed control thresholds.

Bitcoin Accumulation No Longer the Priority as Strategy Shifts

CEO Phong Le stated clearly during the conference call: "When selling Bitcoin is beneficial to the company, we will sell. We will not sit around and say that we will never sell Bitcoin." He also noted that the company's objective has shifted from growth in total Bitcoin holdings to growth in Bitcoin per share.

Shareholder dilution is a hidden debt that has been significantly underestimated over the past few years. MicroStrategy's Class A common shares have ballooned from 76 million at the end of 2020 to over 330 million, a 313% increase. Issuing additional shares to raise capital for Bitcoin purchases is essentially an equivalent exchange of equity dilution for incremental Bitcoin.

Now, the new CEO has shifted the company's strategic goal from total holdings to holdings per share, making a structural adjustment from quantity toward quality. When the premium falls below a critical threshold, selling small amounts of Bitcoin to fund dividends or even share buybacks may actually be a more efficient way to increase the value of Bitcoin per share.

Saylor also provided a vivid explanation during the conference call: We would sell some Bitcoin to pay dividends just to prime the market and signal our success.

1.22x mNAV watershed

During the earnings call, management also introduced a core quantitative metric: a 1.22x mNAV. mNAV measures the ratio between the company's market capitalization and the value of its Bitcoin holdings.

When the premium exceeds 1.22x, the company continues to issue shares and raise capital to purchase Bitcoin. If the premium falls below 1.22x, further share issuance is no longer accretive; management would instead pivot to selling BTC to use the proceeds for debt repayment or share buybacks.

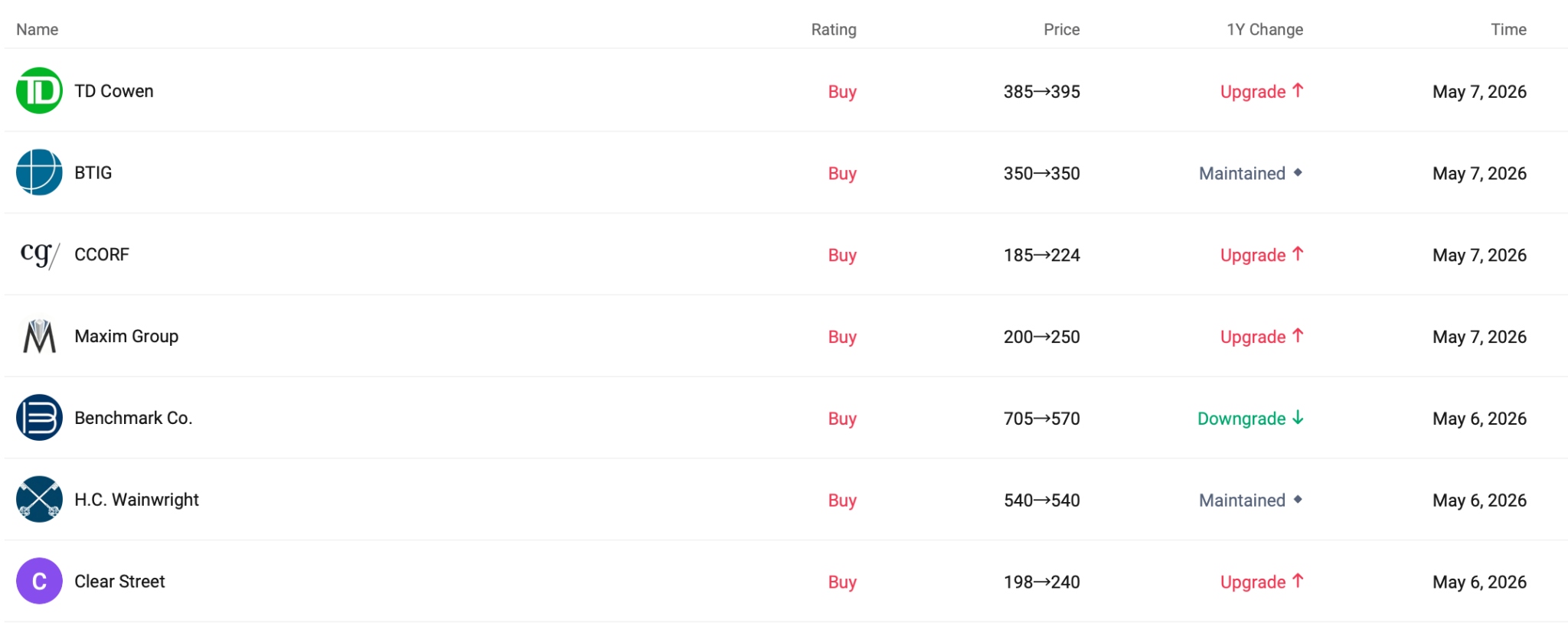

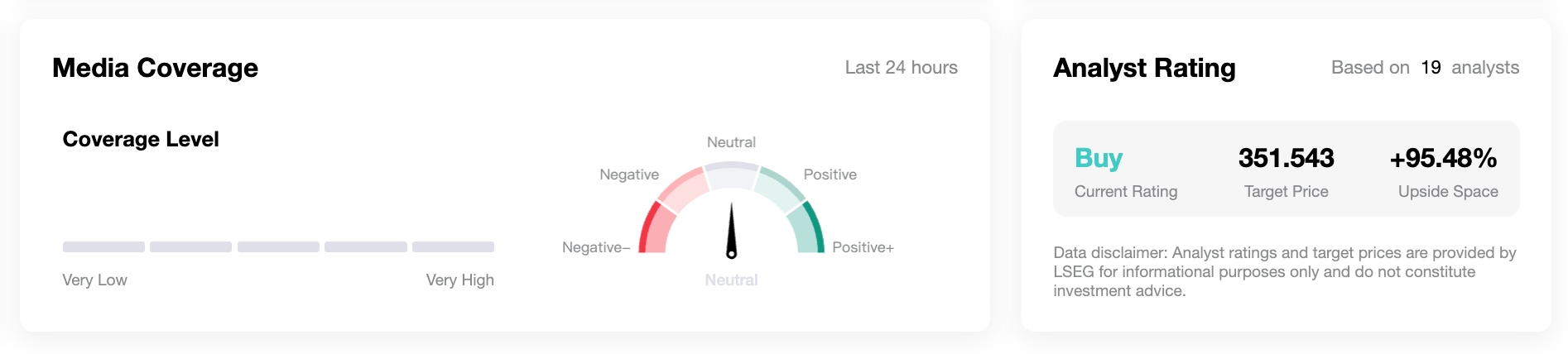

Looking across Wall Street price targets, TD Cowen has set a target of $395, while Citi maintains a Buy rating at $260. CCORF raised its price target to $224. This extremely wide range of targets reflects significant market divergence regarding the valuation logic under MicroStrategy’s new model.

According to TradingKey data, the average price target is approximately $351, implying more than 95% upside from the current share price. However, it should be noted that the extent of this upside remains dependent on the future trajectory of Bitcoin.

The signal released by Saylor is essentially a proactive flexibility adjustment of the public balance sheet. STRC brings the world's largest preferred stock issuance pool and matching institutional absorption capacity, but rigid repayment pressures persist. When financing costs begin to erode the margin of safety, establishing robust risk safety valves in advance is a better way to ensure the continuity of this flywheel model.

Recommended Articles