Strait of Hormuz Reopening in Sight? Don’t Be Optimistic Too Early: Energy Executives Bet on November, Oil Prices Could Hit $200.

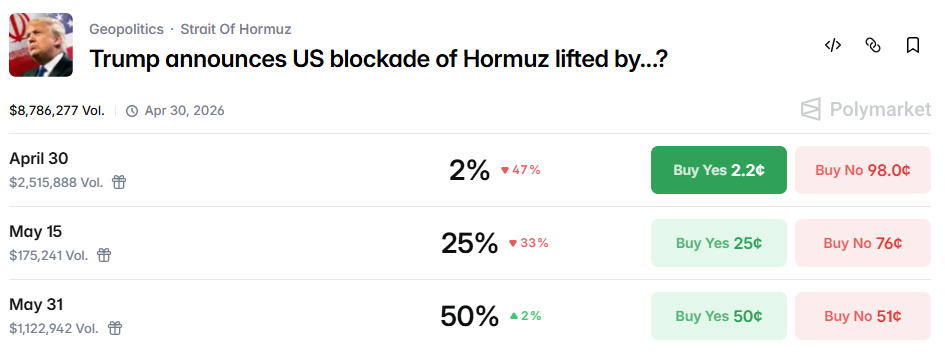

TradingKey - Despite the persistent lack of an agreement between the U.S. and Iran, the ceasefire remains intact. Against this backdrop, market expectations for the reopening of the Strait of Hormuz have turned optimistic. Prediction market Polymarket shows a 50% probability that normal navigation will resume by the end of June.

However, from a professional perspective, the reality may be less sanguine. According to the Dallas Fed’s latest Energy Survey, 40% of its respondents—oil and gas executives—believe that this day may not arrive until November or later this year.

Image courtesy of Polymarket

Retail Investors Bet on June Approval; Energy Executives Cast “No” Votes

Dallas Fed survey data shows that only 20% of surveyed energy executives believe navigation through the Strait of Hormuz could return to normal by May, while 39% believe it will take until August, and 26% extend the timeline to November; another 14% believe normalization will not occur until after November. This data stands in sharp contrast to the views of public prediction markets: as many as 80% of energy executives believe normal transit may not be possible until at least August, and nearly 40% believe the probability of a resolution within the year is quite limited.

The survey report noted that there are discrepancies in short-term judgments between these two groups, and that industry insiders are also more sensitive to tail risks and long-term risks.

Latest reports indicate that Iran will launch military retaliation against the U.S. naval blockade, while the U.S. stated that Trump has prepared plans to sustain the blockade measures against Iran for several months.

BNP Paribas pointed out in its latest quarterly outlook that the current dual blockade of the Strait of Hormuz by both Iran and the United States will make a future where crude oil reaches $200 per barrel no longer out of reach.

Crude Oil May Enter an Era of Sustained High Premiums

While as many as 86% of surveyed executives believe normal passage through the strait will resume by November, 48% believe it remains highly likely that another geopolitical event will disrupt Hormuz passage within the next five years. This indicates an industry-wide realization that while current hostilities may subside, the Strait of Hormuz remains extremely fragile as a global energy artery. Given this consensus, a repricing of the geopolitical risk premium for energy assets may be only a matter of time.

Furthermore, transportation costs will remain an issue even after passage through the strait is restored. 79% of surveyed executives expect transportation costs for Persian Gulf exports to rise by at least $2 per barrel after the conflict ends, with 43 percentage points of that group believing the increase will be no less than $4. These transportation costs include insurance, freight, and transit fees.

In other words, the rise in transportation costs will no longer be driven solely by the state of conflict but will instead become a long-term fixture. This remains tied to the market consensus regarding long-term geopolitical risks in the strait.

The impact varies across segments of the crude oil value chain: for refiners, shipping companies, and downstream consumers reliant on Persian Gulf crude, cost structures have shifted toward a trending upward trajectory; for upstream E&P (Exploration and Production) companies, despite rising transportation costs, they remain relatively resilient as they can pass costs to other segments through higher pricing; meanwhile, midstream and downstream segments highly sensitive to logistics costs will face sustained pressure from margin erosion.

US Shale Oil Struggles to Fill Global Gap

During the current cycle of rising crude oil prices, the market has pinned some of its hopes on the U.S. shale industry, expecting that rapid production growth would fill the supply gap caused by transportation disruptions in the Persian Gulf. However, evidence suggests this may be unrealistic.

Survey data indicates that 90% of executives polled expect that, as a result of the conflict, U.S. oil production growth will not exceed 500,000 barrels per day in 2026, with little change in that outlook for 2027. This implies that relying on U.S. output increases to bridge the global crude shortfall is like a drop in the bucket.

The reason lies in the fact that the U.S. shale industry has weathered years of prolonged stagnation. When oil prices collapsed in 2014 and 2020, hundreds of shale firms declared bankruptcy, demonstrating that the commercial logic of continuous capacity expansion was no longer viable.

In addition, while spot oil prices remain high, oil and gas executives have observed a divergent trend: forward crude contracts have not seen a corresponding surge. Shale development typically takes months or longer from drilling to production; if the current window of high prices is missed and prices retreat once the conflict concludes, the heavy costs incurred today will be impossible to recover.

Recommended Articles